PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038438

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038438

Metal Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

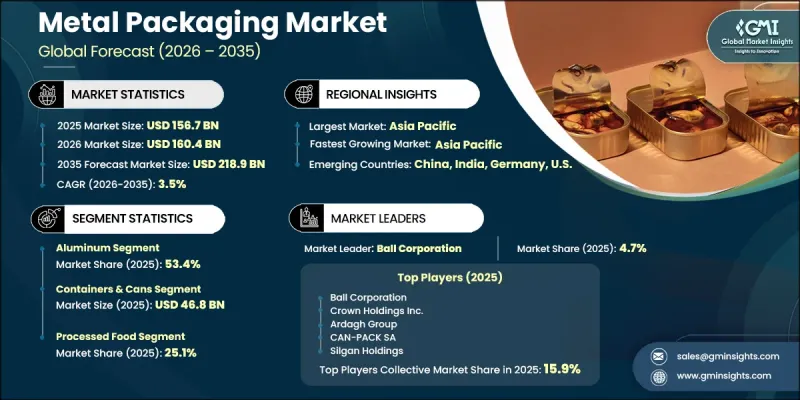

The Global Metal Packaging Market was valued at USD 156.7 billion in 2025 and is estimated to grow at a CAGR of 3.5% to reach USD 218.9 billion by 2035.

Market expansion is driven by tightening sustainability regulations that are encouraging a transition away from plastic toward highly recyclable metal packaging formats. Increasing consumption of packaged food and beverages, supported by fast-paced urban lifestyles, is further strengthening demand. Metal packaging is widely recognized for its ability to extend product shelf life while preserving quality and safety, making it a preferred choice across multiple industries. Growing applications in pharmaceuticals, healthcare, and personal care sectors are also contributing to market growth, as these industries prioritize durable and contamination-resistant packaging solutions. In addition, advancements in lightweight materials and modern manufacturing technologies are improving production efficiency and enhancing product design, allowing brands to achieve stronger visual appeal and differentiation. As sustainability, durability, and performance remain key priorities, metal packaging continues to gain traction across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $156.7 Billion |

| Forecast Value | $218.9 Billion |

| CAGR | 3.5% |

The metal packaging market is also benefiting from increasing global emphasis on environmentally responsible packaging solutions. Regulatory frameworks focused on recycling targets and extended producer responsibility are encouraging the adoption of materials such as aluminum and steel due to their high recyclability and circular economy benefits. The scope of metal packaging has expanded beyond traditional food and beverage applications, with growing utilization across healthcare, personal care, and industrial sectors where performance, protection, and product stability are critical. Continuous technological advancements in production processes are improving efficiency, reducing costs, and enhancing scalability, which is enabling broader adoption across diverse end-use industries. These developments are strengthening the competitiveness of metal packaging compared to alternative materials.

The steel segment is expected to grow at a CAGR of 3.2% through 2035, supported by consistent demand from canned goods, household products, and industrial packaging applications. Steel remains a preferred material due to its strength, durability, and ability to withstand high-pressure and high-volume usage conditions. Its cost-effectiveness further supports its adoption in large-scale packaging operations, particularly in price-sensitive markets. As industries continue to prioritize reliable and robust packaging solutions, steel is expected to maintain steady growth across a wide range of applications.

The bottles and jars segment is projected to grow at a CAGR of 5.4% during 2026-2035. Growth in this segment is driven by rising demand across personal care, cosmetics, pharmaceutical, and specialty food industries. Consumers are increasingly favoring premium packaging formats that offer both functionality and visual appeal, leading to greater adoption of metal bottles and jars. Their reusability, durability, and ability to preserve product integrity are key factors supporting their popularity in value-added and niche applications.

North America Metal Packaging Market accounted for 35.3% share in 2025, supported by strong demand across food, beverage, and household product segments. The region benefits from a well-established retail and foodservice infrastructure, which drives consistent consumption of packaged goods. High demand for convenient and ready-to-consume products, combined with a preference for hygienic and long-lasting packaging, continues to support the widespread use of metal containers. Increasing regulatory focus on recycling and sustainability, along with investments in domestic manufacturing and recycling capabilities, is further strengthening market growth across North America.

Key companies operating in the Global Metal Packaging Market include Ball Corporation, Crown Holdings Inc., Ardagh Group, Amcor Limited, Silgan Holdings, Sonoco Products Company, CAN-PACK SA, Toyo Seikan Group Holdings Inc., Tata Steel, Novelis Inc, Mauser Packaging Solutions, CCL Containers, DS Containers Inc., Greif Incorporated, Tubex GmbH, CPMC Holdings, and Visy Industries. These companies are actively expanding their capabilities and enhancing product offerings to meet evolving industry requirements. Companies in the metal packaging market are focusing on strategic initiatives aimed at strengthening their competitive position and expanding global reach. A major emphasis is placed on developing lightweight and sustainable packaging solutions that reduce material usage while maintaining durability and performance. Firms are investing in advanced manufacturing technologies to improve production efficiency and lower operational costs. Strategic collaborations with consumer brands and supply chain partners are helping companies secure long-term contracts and expand their customer base. Additionally, organizations are enhancing recycling capabilities and promoting circular economy practices to align with environmental regulations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward sustainable and infinitely recyclable packaging

- 3.2.1.2 Rising consumption of packaged food and beverages

- 3.2.1.3 Increasing focus on product safety and shelf-life extension

- 3.2.1.4 Growth of pharmaceutical, personal care, and aerosol applications

- 3.2.1.5 Lightweight and technological advancements in metal packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in raw material prices

- 3.2.2.2 High capital intensity and energy-intensive manufacturing processes

- 3.2.3 Market opportunities

- 3.2.3.1 Substitution of multi-material packaging with mono-material metal solutions

- 3.2.3.2 Emergence of smart and functional metal packaging solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Steel

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Containers & cans

- 6.3 Bottles & jars

- 6.4 Caps & closures

- 6.5 Barrels & drums

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Processed food

- 7.3 Dairy products

- 7.4 Beverages

- 7.5 Personal care & cosmetics

- 7.6 Paints & varnishes

- 7.7 Healthcare

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Ball Corporation

- 9.1.2 Crown Holdings Inc.

- 9.1.3 Ardagh Group

- 9.1.4 CAN-PACK SA

- 9.1.5 Silgan Holdings

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 CPMC Holdings

- 9.2.1.2 DS Containers Inc.

- 9.2.1.3 Greif Incorporated

- 9.2.1.4 Mauser Packaging Solutions

- 9.2.1.5 Sonoco Products Company

- 9.2.2 Asia Pacific

- 9.2.2.1 Toyo Seikan Group Holdings Inc.

- 9.2.2.2 Visy Industries

- 9.2.3 Europe

- 9.2.3.1 Tubex GmbH

- 9.2.3.2 CCL Containers

- 9.2.4 Middle East & Africa

- 9.2.4.1 Tata Steel

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Amcor Limited

- 9.3.2 Novelis Inc.