PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038439

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038439

Residential Air Insulated Transformer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

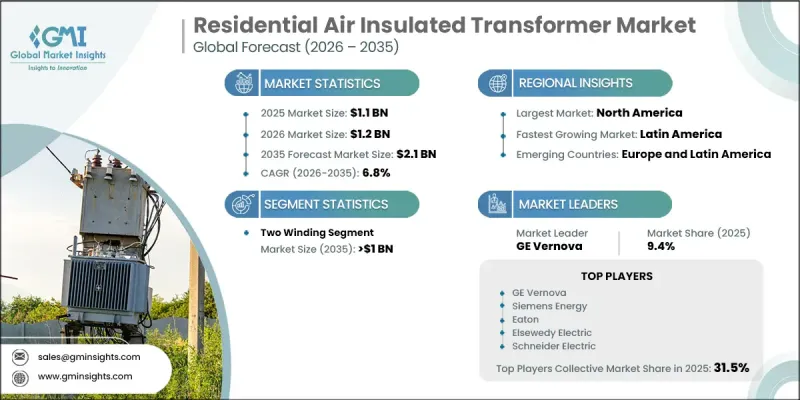

The Global Residential Air Insulated Transformer Market was valued at USD 1.1 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 2.1 billion by 2035.

Market expansion is supported by rising urban development and increasing demand for safer and more cost-effective electrical distribution solutions. Air insulated transformers are gaining preference in residential environments due to their enhanced safety profile and reduced risk compared to conventional alternatives. Their design eliminates concerns related to leakage and contamination, aligning with the growing focus on secure and sustainable living infrastructure. Improvements in product efficiency and declining costs are further encouraging widespread adoption across residential settings. Additionally, evolving energy consumption patterns and the need for dependable power distribution systems are strengthening market demand. The push toward environmentally responsible technologies, coupled with the transition to modern electrical frameworks, continues to position air insulated transformers as a reliable solution for residential applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.1 Billion |

| Forecast Value | $2.1 Billion |

| CAGR | 6.8% |

Growing adoption of air insulated transformers across households and low-capacity buildings is largely driven by their affordability and low maintenance requirements. These systems offer a safer alternative by minimizing risks associated with environmental damage and operational hazards. Increasing urbanization has created a strong need for efficient and reliable power distribution networks, accelerating product penetration. At the same time, the demand for energy-efficient electrical equipment is rising, prompting greater focus on advanced transformer technologies that support optimized energy usage and improved performance.

The two winding segment is expected to reach USD 1 billion in 2035. These transformers play a critical role in regulating electricity flow between power grids and residential consumption points, ensuring stable and efficient energy distribution. Their importance is increasing alongside the expansion of renewable energy adoption, which requires effective systems for integrating power into existing grids. These transformers support seamless energy transfer across networks, enabling consistent electricity supply and improved grid reliability.

U.S. Residential Air Insulated Transformer Market is anticipated to reach USD 500 million by 2035. Growth is being driven by the integration of advanced energy technologies supported by federal initiatives aimed at improving power management and efficiency. At the same time, substantial investments in modernizing aging electrical infrastructure across developed regions are contributing to increased adoption. Air insulated transformers are becoming essential components in upgraded power distribution systems designed to meet evolving residential energy demands.

Key companies operating in the Global Residential Air Insulated Transformer Market include Siemens Energy, Schneider Electric, General Electric, Mitsubishi Electric, Toshiba, Eaton, CG Power, Kirloskar Electric, Hyosung, Elsewedy Electric, Arteche, Daihen, Ormazabal, Pfiffner, Imefy, Celme, and Trench. Companies in the Residential Air Insulated Transformer Market are enhancing their competitive position through continuous innovation, strategic collaborations, and expansion into high-growth regions. Many players are investing in research and development to improve transformer efficiency, safety, and environmental performance. Partnerships with utility providers and infrastructure developers are helping companies secure long-term projects and strengthen distribution networks. Businesses are also focusing on upgrading manufacturing capabilities to meet increasing demand and comply with evolving regulatory standards. Expanding product portfolios with energy-efficient and smart-enabled solutions is another key approach. Additionally, companies are leveraging competitive pricing, strong branding, and improved after-sales services to boost customer retention and expand their global footprint.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Winding trends

- 2.1.3 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.8 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Winding, 2022 - 2035 ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 Two winding

- 5.3 Auto transformer

Chapter 6 Market Size and Forecast, By Region, 2022 - 2035 ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 France

- 6.3.3 Russia

- 6.3.4 UK

- 6.3.5 Italy

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 South Korea

- 6.4.4 India

- 6.4.5 Australia

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 South Africa

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

Chapter 7 Company Profiles

- 7.1 Arteche

- 7.2 Celme

- 7.3 CG Power

- 7.4 Daihen

- 7.5 Eaton

- 7.6 Elsewedy Electric

- 7.7 General Electric

- 7.8 Hyosung

- 7.9 Imefy

- 7.10 Kirloskar Electric

- 7.11 Mitsubishi Electric

- 7.12 Ormazabal

- 7.13 Pfiffner

- 7.14 Schneider Electric

- 7.15 Siemens Energy

- 7.16 Toshiba

- 7.17 Trench