PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038462

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038462

Plastic Bottles and Containers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

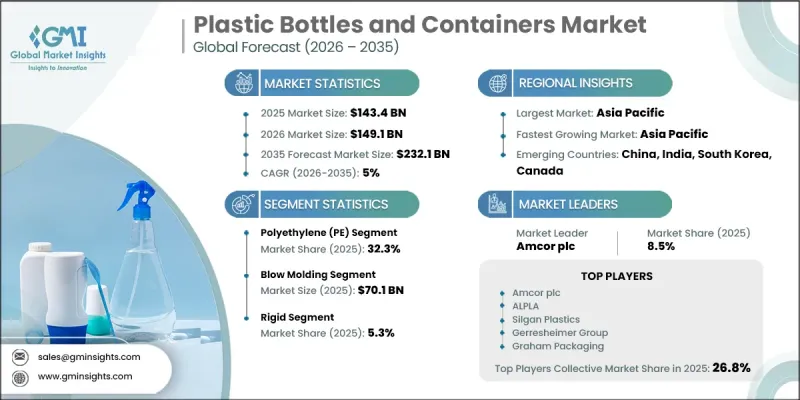

The Global Plastic Bottles and Containers Market was valued at USD 143.4 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 232.1 billion by 2035.

Market growth is driven by increasing consumption of bottled beverages and water, supported by changing lifestyles and rising urban populations. Growing demand for convenient, lightweight, and durable packaging solutions is further strengthening adoption across multiple industries. The personal care and cosmetics sector is contributing significantly, as brands continue to seek visually appealing and functional packaging formats that enhance product differentiation. In addition, the pharmaceutical industry is driving demand for reliable liquid packaging solutions that ensure product safety and compliance. The widespread use of polyethylene terephthalate due to its cost efficiency and versatility is supporting large-scale production. At the same time, increasing focus on sustainability is encouraging the adoption of recycled materials and environmentally responsible packaging solutions. Continuous advancements in packaging technologies, along with shifting consumer preferences toward convenience and hygiene, are reinforcing the steady expansion of the plastic bottles and containers market across global regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $143.4 Billion |

| Forecast Value | $232.1 Billion |

| CAGR | 5% |

The plastic bottles and containers market is further supported by rising global demand for packaged beverages and personal care products. Increasing consumer spending on hygiene, grooming, and wellness products is encouraging manufacturers to develop innovative, lightweight, and aesthetically appealing packaging solutions. The growing influence of fast-moving consumer goods industries and expanding pharmaceutical applications is also contributing to higher demand. In addition, the preference for lightweight materials and the increasing use of advanced polymers are improving production efficiency and reducing transportation costs. Investments in recycling technologies and sustainable packaging solutions are further enhancing market competitiveness while addressing environmental concerns.

The polyethylene segment accounted for a 32.3% share in 2025, driven by its widespread use across various applications. This material is favored for its strong chemical resistance, durability, lightweight properties, and cost-effectiveness, making it suitable for large-scale production. Its compatibility with multiple manufacturing processes enhances its versatility, allowing it to be used across different industries. The ability to produce high volumes efficiently continues to support its dominance in the market.

The blow molding segment reached USD 70.1 billion in 2025, due to its critical role in producing hollow plastic containers. This manufacturing process is widely adopted for its ability to deliver lightweight, durable, and cost-efficient products at high production speeds. Its flexibility in design and compatibility with commonly used materials supports its widespread use across industries. The scalability and efficiency of blow molding technology continue to make it a preferred choice for large-scale production of plastic bottles and containers.

North America Plastic Bottles and Containers Market accounted for 27.6% share in 2025, driven by strong regulatory frameworks and increasing focus on sustainable packaging practices. The region is experiencing growing adoption of advanced packaging technologies aimed at improving recyclability and reducing environmental impact. Investments in recycling infrastructure, including both mechanical and advanced recycling methods, are supporting the availability of recycled materials for packaging production. Additionally, regulatory mandates encouraging the use of recycled content are influencing market dynamics and driving innovation. The presence of established packaging manufacturers and continuous technological advancements are further supporting market growth across the region.

Key companies operating in the Global Plastic Bottles and Containers Market include Amcor, ALPLA, Gerresheimer Group, Graham Packaging, Silgan Plastics, Tekni-Plex, Huhtamaki Oyj, KHS Group, MJS Packaging, Cospak, Cambrian Packaging, Air Sea Containers, Dhanraj Plastics Private Limited, JSK Plastic Industries, Jyoti Chemicals, Kee Pet Containers, and Plastoworld India Private Limited.Companies in the Plastic Bottles and Containers Market are adopting a range of strategies to strengthen their market position and enhance competitiveness. A key focus is on developing sustainable packaging solutions by increasing the use of recycled materials and improving recyclability. Firms are investing in advanced manufacturing technologies to enhance efficiency, reduce material usage, and optimize production processes. Strategic collaborations with consumer goods companies and pharmaceutical manufacturers are helping expand market reach and secure long-term contracts. Companies are also focusing on lightweight packaging designs to lower transportation costs and environmental impact. Geographic expansion into emerging markets, along with capacity enhancements, is supporting revenue growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Product type trends

- 2.2.3 Technology trends

- 2.2.4 Capacity trends

- 2.2.5 End-use industry trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising bottled water and beverage consumption globally

- 3.2.1.2 Growth in personal care packaging demand

- 3.2.1.3 Expanding pharmaceutical liquid packaging requirements

- 3.2.1.4 Increased FMCG demand for lightweight containers

- 3.2.1.5 PET adoption due to cost efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent single-use plastic regulations worldwide

- 3.2.2.2 Volatile resin prices affect production costs

- 3.2.3 Market opportunities

- 3.2.3.1 Smart packaging integration for consumer engagement

- 3.2.3.2 Bio-based plastic container innovation expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Polypropylene (PP)

- 5.3 Polyethylene (PE)

- 5.4 Polystyrene (PS)

- 5.5 Polyethylene terephthalate (PET)

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Rigid

- 6.3 Semi-rigid

- 6.4 Flexible

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Blow molding

- 7.3 Injection molding

- 7.4 Compression molding

Chapter 8 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Small (Less than 250 ml)

- 8.3 Medium (250 ml - 1 liter)

- 8.4 Large (1-5 liters)

Chapter 9 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Food & beverage

- 9.3 Pharmaceuticals & healthcare

- 9.4 Agriculture

- 9.5 Chemicals

- 9.6 Consumer goods

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 ALPLA

- 11.1.2 Amcor

- 11.1.3 Gerresheimer Group

- 11.1.4 Huhtamaki Oyj

- 11.1.5 Silgan Plastics

- 11.1.6 Tekni-Plex

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Air Sea Containers

- 11.2.1.2 Graham Packaging

- 11.2.1.3 MJS Packaging

- 11.2.2 Asia Pacific

- 11.2.2.1 Cospak

- 11.2.2.2 Dhanraj Plastics Private Limited

- 11.2.2.3 Jyoti Chemicals

- 11.2.2.4 Kee Pet Containers

- 11.2.2.5 Plastoworld India Private Limited

- 11.2.3 Europe

- 11.2.3.1 Cambrian Packaging

- 11.2.3.2 KHS Group

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 JSK Plastic Industries