PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038472

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038472

Vertiports Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

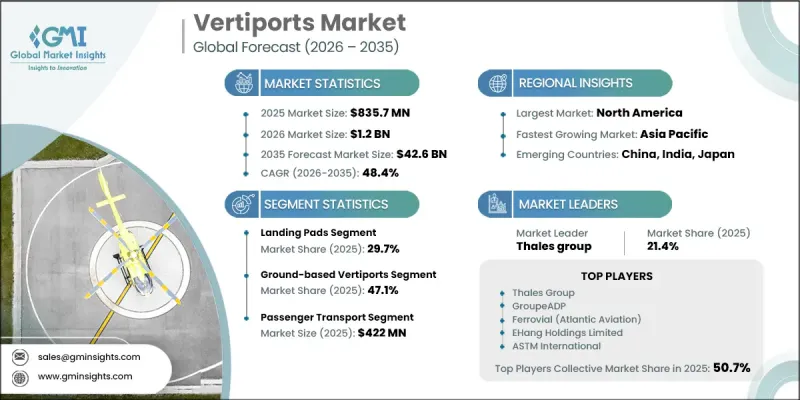

The Global Vertiports Market was valued at USD 835.7 million in 2025 and is estimated to grow at a CAGR of 48.4% to reach USD 42.6 billion by 2035.

Market expansion is driven by rising investments in advanced air mobility infrastructure and the increasing deployment of electric vertical takeoff and landing aircraft, which are reshaping urban transportation frameworks. The integration of vertiports into broader mobility ecosystems is accelerating development, as stakeholders focus on building interconnected transit networks that support seamless passenger and cargo movement. Continuous advancements in infrastructure planning, combined with growing demand for efficient and time-saving transport solutions, are strengthening the market outlook. Additionally, increasing emphasis on reducing congestion and enhancing urban mobility efficiency is encouraging the adoption of next-generation air transport systems. As a result, vertiports are emerging as a critical component of future transportation ecosystems, enabling scalable, efficient, and technologically advanced mobility solutions across rapidly evolving urban landscapes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $835.7 Million |

| Forecast Value | $42.6 Billion |

| CAGR | 48.4% |

Market growth is further supported by rising collaboration across the value chain, where infrastructure developers, aircraft manufacturers, and urban planning authorities are aligning their capabilities to identify high-growth opportunities and accelerate deployment. Strategic partnerships enabling faster project execution and facilitating the development of advanced facilities equipped with enhanced safety systems and efficient traffic management solutions. Increasing investments in passenger-focused infrastructure designs are improving operational efficiency and user experience. At the same time, regulatory frameworks are evolving to support safe and standardized operations, which is strengthening investor confidence and enabling long-term market development. The combination of technological innovation, collaborative ecosystems, and supportive policy environments is creating a strong foundation for sustained market expansion.

The landing pads segment accounted for a share of 29.7% in 2025, maintaining its leadership position due to its fundamental role in supporting aircraft operations. These components are essential for ensuring efficient turnaround times and maintaining operational safety standards. Their integration within the vertiport infrastructure contributes to improved connectivity and streamlined operations, supporting both passenger and cargo movement. The increasing deployment of advanced air mobility systems is driving the demand for well-designed landing infrastructure, reinforcing the segment's importance in overall market growth. Continuous enhancements in design and operational efficiency are further strengthening the segment's position within the industry.

The ground-based vertiports segment held a share of 47.1% in 2025, driven by its operational flexibility and ease of deployment. This category benefits from relatively lower construction complexity and the ability to integrate efficiently with existing infrastructure networks. Its scalability and capability to accommodate increasing traffic volumes make it a preferred choice for early-stage deployment of advanced mobility systems. Ground-based facilities play a crucial role in supporting both passenger and logistics operations, ensuring reliable and efficient service delivery. As demand for urban air mobility continues to rise, this segment is expected to maintain strong growth momentum.

North America Vertiports Market accounted for 38.5% share in 2025, reflecting strong regional adoption supported by regulatory developments and substantial investments. The region is witnessing accelerated progress in infrastructure planning and implementation, driven by increasing focus on advanced mobility solutions. Government initiatives aimed at establishing operational standards and safety guidelines are creating a favorable environment for market growth. Significant capital inflows from both public and private sectors are enabling the development of advanced facilities equipped with modern technologies. These factors collectively contribute to the region's leading position and continued expansion within the global market.

Prominent players operating in the Global Vertiports Industry include Aeroauto LLC, Airnova, airsight, Archer Aviation (Infrastructure Division), ASTM International, Bayards Vertiports Solutions, EHang Holdings Limited, eVertiSKY Corp., Ferrovial (Atlantic Aviation), Jaunt Air Mobility (Vertiport Tech), Joby Aviation, Inc., Skyports Infrastructure Limited, SKYSCAPE Co., Ltd., Tavistock (Lilium GmbH), Urban-Air Port, UrbanV S.p.A, Varon Vehicles Corporation, Vports, Altaport Inc., BETA Technologies, Groupe ADP, Skyway Technologies Corp., and Thales Group. Companies operating in the Global Vertiports Market are focusing on strategic initiatives to enhance their competitive positioning and expand their global footprint. Key strategies include forming long-term partnerships with technology providers, infrastructure developers, and mobility solution companies to accelerate deployment capabilities. Organizations are investing heavily in research and development to improve design efficiency, scalability, and operational safety of vertiport infrastructure. Additionally, companies are emphasizing digital integration, including advanced traffic management systems and smart infrastructure solutions, to optimize performance. Expansion into emerging markets, along with the development of standardized and modular infrastructure models, is enabling faster adoption. Firms are also prioritizing sustainability by incorporating energy-efficient systems and environmentally friendly designs, aligning their offerings with evolving regulatory requirements and future mobility trends.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Solution trends

- 2.2.2 Location trends

- 2.2.3 Type trends

- 2.2.4 Landscape trends

- 2.2.5 Application trends

- 2.2.6 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urbanization and congestion creating demand for vertiports

- 3.2.1.2 Technological advancements in e-VTOL aircraft framing the rise in vertiports

- 3.2.1.3 Governmental support and regulatory frameworks

- 3.2.1.4 Sustainability and environmental concerns

- 3.2.1.5 Investment and infrastructure development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory hurdles

- 3.2.2.2 Concerns for safety and air traffic management

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of vertiports with multimodal transport hubs

- 3.2.3.2 Deployment of sustainable and energy-efficient vertiports

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Solution, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Landing pads

- 5.3 Terminal gates

- 5.4 Ground support equipment

- 5.5 Charging stations

- 5.6 Ground control stations

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Location, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Ground-based Vertiports

- 6.3 Rooftop/Elevated Vertiports

- 6.4 Floating Vertiports

Chapter 7 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Vertihubs

- 7.3 Vertibases

- 7.4 Vertipads

Chapter 8 Market Estimates and Forecast, By Landscape, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Urban vertiports

- 8.3 Regional vertiports

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Passenger Transport

- 9.3 Cargo & Logistics

- 9.4 Emergency & Medical Services

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Thales Group

- 11.1.2 ASTM International

- 11.1.3 EHang Holdings Limited

- 11.1.4 Ferrovial (Atlantic Aviation)

- 11.1.5 Groupe ADP

- 11.1.6 Skyports Infrastructure Limited

- 11.1.7 Joby Aviation, Inc.

- 11.1.8 Archer Aviation (Infrastructure Division)

- 11.1.9 BETA Technologies

- 11.2 Regional key players

- 11.2.1 Tavistock (Lilium GmbH)

- 11.2.2 Urban-Air Port

- 11.2.3 UrbanV S.p.A

- 11.2.4 SKYSCAPE Co., Ltd.

- 11.2.5 Vports

- 11.2.6 Altaport Inc.

- 11.2.7 Skyway Technologies, Corp.

- 11.2.8 Bayards Vertiports Solutions

- 11.2.9 Jaunt Air Mobility (Vertiport Tech)

- 11.3 Niche Players/Disruptors

- 11.3.1 Aeroauto LLC

- 11.3.2 Airnova

- 11.3.3 airsight

- 11.3.4 eVertiSKY Corp.

- 11.3.5 Varon Vehicles Corporation