PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038675

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038675

Industrial Heat Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

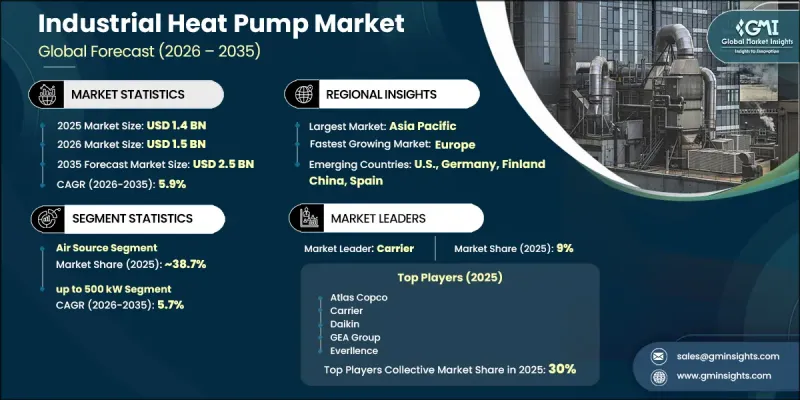

The Global Industrial Heat Pump Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 2.5 billion in 2035.

The market is gaining momentum as industries increasingly focus on decarbonizing operations and improving energy efficiency across heating and cooling systems. Rising efforts to capture and reuse industrial waste heat are further strengthening adoption, as heat pumps provide an effective way to convert low-grade heat into usable thermal energy while reducing dependence on fossil fuels. Growing emphasis on sustainability targets, coupled with stricter environmental regulations and carbon reduction mandates, is accelerating deployment across industrial facilities. The replacement of conventional heating technologies with energy-efficient alternatives is further supporting demand. Additionally, expanding industrial infrastructure in emerging economies and rising energy consumption across manufacturing processes are contributing to long-term market growth. Continuous regulatory pressure and corporate sustainability commitments are expected to further enhance adoption rates over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 5.9% |

The ground source heat pump segment generated USD 50.7 million in 2025 and is projected to grow steadily as industries increase adoption for heating and cooling applications while focusing on carbon emission reduction. These systems are recognized for their efficiency and sustainability, using low-temperature geothermal energy to support thermal transfer processes across industrial environments.

The 500 kW to 2 MW capacity segment is expected to register a CAGR of 5.9% from 2026 to 2035. Rising environmental concerns and decarbonization initiatives are driving demand for high-capacity systems capable of supporting large-scale industrial operations. Manufacturers are increasingly investing in research, partnerships, and product innovation to develop advanced high-output systems that reduce reliance on fossil fuel-based heating.

United States Industrial Heat Pump Market held an 85.3% share in 2025, generating USD 274.6 million. Growth in the country is supported by strong industrial demand for efficient thermal systems and strict regulatory frameworks aimed at reducing emissions. The transition toward high-capacity industrial heat pumps is also reinforcing the shift toward low-carbon manufacturing and reduced fossil fuel consumption.

Major players operating in the Global Industrial Heat Pump Industry include Armstrong International, Atlas Copco, Carrier, Daikin Applied Europe, Johnson Controls, Mitsubishi Electric, Siemens Energy, Trane Technologies, GEA Group, and Thermax. Companies in the Industrial Heat Pump Market are prioritizing the development of high-efficiency systems that enable waste heat recovery and support large-scale industrial decarbonization goals. They are investing heavily in advanced R&D to improve system performance, capacity, and integration with existing industrial infrastructure. Strategic collaborations with industrial operators and engineering firms are being used to accelerate deployment and improve customization for sector-specific requirements. Manufacturers are also focusing on expanding product portfolios to include scalable heat pump systems suitable for diverse industrial load demands. Strengthening global supply chains and enhancing after-sales service capabilities are further helping companies improve customer retention. In addition, firms are leveraging regulatory incentives and sustainability programs to promote adoption and position their solutions as viable alternatives to conventional fossil-fuel-based heating systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid Sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Capacity trends

- 2.5 Temperature trends

- 2.6 Application trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Positive outlook toward renewable sector

- 3.2.1.2 Influx of new investments across heavy duty industrial applications

- 3.2.1.3 Encouraging regulatory framework by respective authorities to curb carbon emissions

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Significant initial deployment cost

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of industrial heat pumps

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035, (USD Million, Units)

- 5.1 Key trends

- 5.2 Air source

- 5.3 Ground source

- 5.4 Water source

- 5.5 Closed cycle mechanical heat pump

- 5.6 Open cycle mechanical vapor compression heat pump

- 5.7 Open cycle mechanical thermocompression heat pump

- 5.8 Closed cycle absorption heat pump

Chapter 6 Market Size and Forecast, By Capacity, 2022 - 2035, (USD Million, Units)

- 6.1 Key trends

- 6.2 Up to 500 kW

- 6.3 > 500 kW to 2 MW

- 6.4 2 MW - 5 MW

- 6.5 > 5 MW

Chapter 7 Market Size and Forecast, By Temperature, 2022 - 2035, (USD Million, Units)

- 7.1 Key trends

- 7.2 80 - 100 °C

- 7.3 100 - 150 °C

- 7.4 150 - 200 °C

- 7.5 > 200 °C

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035, (USD Million, Units)

- 8.1 Key trends

- 8.2 Industrial

- 8.2.1 Paper

- 8.2.2 Food & beverages

- 8.2.3 Chemical

- 8.2.4 Iron & Steel

- 8.2.5 Machinery

- 8.2.6 Non-Metallic minerals

- 8.2.7 Other industries

- 8.3 District heating

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035, (USD Million, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Norway

- 9.3.3 Denmark

- 9.3.4 Finland

- 9.3.5 Sweden

- 9.3.6 Germany

- 9.3.7 Poland

- 9.3.8 Spain

- 9.3.9 Austria

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 Australia

- 9.4.4 South Korea

- 9.5 Middle East and Africa

- 9.5.1 Saudi Arabia

- 9.5.2 Turkey

- 9.5.3 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Mexico

Chapter 10 Company Profiles

- 10.1 AGO Energie + Anlagen

- 10.2 Armstrong International

- 10.3 Atlas Copco

- 10.4 Baker Hughes

- 10.5 Carrier

- 10.6 Daikin Applied Europe

- 10.7 Dalrada Technology Group

- 10.8 Ecop

- 10.9 Enerin

- 10.10 Everllence

- 10.11 GEA Group

- 10.12 Hien New Energy Equipment

- 10.13 Johnson Controls

- 10.14 Mitsubishi Electric

- 10.15 Ochsner

- 10.16 Oilon Group

- 10.17 Siemens Energy

- 10.18 Thermax

- 10.19 Trane Technologies

- 10.20 Turboden