PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038691

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038691

U.S. Dialysis Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

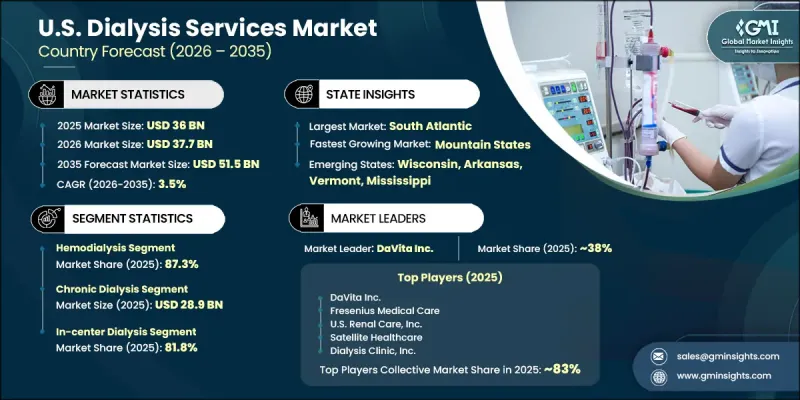

U.S. Dialysis Services Market was valued at USD 36 billion in 2025 and is estimated to grow at a CAGR of 3.5% to reach USD 51.5 billion by 2035.

Market growth is supported by a rising prevalence of chronic conditions that contribute to kidney dysfunction, along with an increasing number of patients diagnosed with end-stage renal disease. The steady expansion of dialysis facilities and favorable reimbursement structures is further strengthening the industry landscape. Growing awareness around kidney health, coupled with an aging population, is contributing to higher demand for treatment services. At the same time, the adoption of digital health technologies and remote monitoring systems is reshaping how care is delivered. Continuous investment in research and development is driving innovation in dialysis techniques and treatment approaches, enabling improved efficiency and patient outcomes. These advancements are focused on enhancing comfort, optimizing treatment effectiveness, and addressing unmet clinical needs. Dialysis services include medical procedures designed to support individuals with reduced kidney function by removing waste, excess fluids, and toxins from the bloodstream through specialized treatment methods.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $36 Billion |

| Forecast Value | $51.5 Billion |

| CAGR | 3.5% |

The hemodialysis segment accounted for a share of 87.3% in 2025. Demand for this segment continues to rise due to the limited availability of organ transplants and the increasing need for long-term renal support. Hemodialysis remains the most widely utilized treatment method, involving the filtration of blood through specialized equipment to remove impurities and excess fluids. Its widespread adoption is supported by its clinical effectiveness and broad availability across multiple healthcare settings, supported by a well-established infrastructure that ensures accessibility and consistent care delivery.

The chronic dialysis segment generated USD 28.9 billion in 2025. Patients with advanced kidney conditions typically depend on ongoing treatment schedules to maintain stable health conditions. This form of dialysis requires routine sessions conducted several times per week to effectively manage fluid balance and toxin removal. These services are delivered through specialized healthcare environments staffed by trained professionals with expertise in renal care, ensuring comprehensive and continuous patient support.

South Atlantic Dialysis Services Market reached USD 8.2 billion in 2025. Strong regional performance is supported by the presence of established service providers, advanced healthcare infrastructure, and consistent investment in research initiatives. High healthcare spending levels and broad insurance coverage also contribute to improved access to dialysis treatments, supporting continued market expansion within the region.

Key players operating in the U.S. Dialysis Services Market include Fresenius Medical Care, DaVita Inc., U.S. Renal Care, Inc., Satellite Healthcare, Dialysis Clinic, Inc., Innovative Renal Care, Sanderling Renal Services, Rogosin Institute, Centers for Dialysis Care, and Vantive. Companies in the U.S. Dialysis Services Market are enhancing their competitive position through strategic expansion of treatment centers and increased investment in advanced care technologies. Emphasis is being placed on integrating digital health solutions and remote monitoring systems to improve patient management and operational efficiency. Organizations are also focusing on research and development to introduce innovative treatment methods that enhance clinical outcomes and patient experience. Partnerships and collaborations are being formed to strengthen service networks and expand geographic reach. Additionally, companies are working to optimize cost structures and improve service quality through staff training and process improvements.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by zone

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Zonal trends

- 2.2.2 Type trends

- 2.2.3 Service trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising number of end stage renal diseases (ESRD) patients

- 3.2.1.2 Favorable reimbursement scenario available for dialysis treatment

- 3.2.1.3 Expansion of dialysis centers across the U.S.

- 3.2.1.4 Increasing incidence of diabetes leading to kidney disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs associated with dialysis

- 3.2.2.2 Complications associated with dialysis treatment

- 3.2.3 Opportunities

- 3.2.3.1 Growth in home-based dialysis adoption

- 3.2.3.2 Development of biocompatible and high-efficiency dialysis membranes

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Impact of AI & generative AI on the market (Driven by Primary Research)

- 3.7.1 AI-driven disruption of existing business models

- 3.7.2 GenAI use cases & adoption roadmap by segment

- 3.8 Number of dialysis centers by key companies, 2025

- 3.9 Reimbursement scenario (Driven by Primary Research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by Primary Research)

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Hemodialysis

- 5.3 Peritoneal dialysis

Chapter 6 Market Estimates and Forecast, By Service, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Acute dialysis

- 6.3 Chronic dialysis

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 In-center dialysis

- 7.3 Home dialysis

Chapter 8 Market Estimates and Forecast, By Zone, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 East North Central

- 8.2.1 Illinois

- 8.2.2 Indiana

- 8.2.3 Michigan

- 8.2.4 Ohio

- 8.2.5 Wisconsin

- 8.3 West South Central

- 8.3.1 Arkansas

- 8.3.2 Louisiana

- 8.3.3 Oklahoma

- 8.3.4 Texas

- 8.4 South Atlantic

- 8.4.1 Delaware

- 8.4.2 Florida

- 8.4.3 Georgia

- 8.4.4 Maryland

- 8.4.5 North Carolina

- 8.4.6 South Carolina

- 8.4.7 Virginia

- 8.4.8 West Virginia

- 8.4.9 Washington, D.C.

- 8.5 North East

- 8.5.1 Connecticut

- 8.5.2 Maine

- 8.5.3 Massachusetts

- 8.5.4 New Hampshire

- 8.5.5 Rhode Island

- 8.5.6 Vermont

- 8.5.7 New Jersey

- 8.5.8 New York

- 8.5.9 Pennsylvania

- 8.6 East South Central

- 8.6.1 Alabama

- 8.6.2 Kentucky

- 8.6.3 Mississippi

- 8.6.4 Tennessee

- 8.7 Pacific Central

- 8.7.1 Alaska

- 8.7.2 California

- 8.7.3 Hawaii

- 8.7.4 Oregon

- 8.7.5 Washington

- 8.8 Mountain States

- 8.8.1 Arizona

- 8.8.2 Colorado

- 8.8.3 Utah

- 8.8.4 Nevada

- 8.8.5 New Mexico

- 8.8.6 Idaho

- 8.8.7 Montana

- 8.8.8 Wyoming

Chapter 9 Company Profiles

- 9.1 Centers for Dialysis Care

- 9.2 DaVita Inc.

- 9.3 Dialysis Clinic, Inc.

- 9.4 Fresenius Medical Care

- 9.5 Innovative Renal Care

- 9.6 Rogosin Institute

- 9.7 Sanderling Renal Services

- 9.8 Satellite Healthcare

- 9.9 U.S. Renal Care, Inc.

- 9.10 Vantive