PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038703

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038703

High-Speed Steel Metal Cutting Tools Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

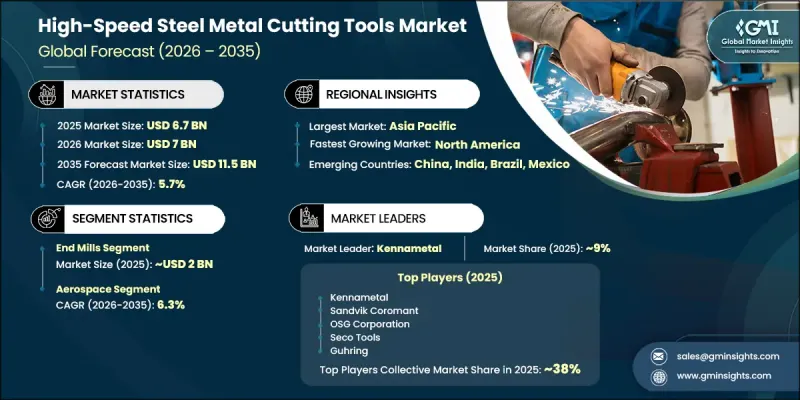

The Global High-Speed Steel Metal Cutting Tools Market was valued at USD 6.7 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 11.5 billion by 2035.

The market is expanding, supported by the growth of global manufacturing activities, industrial automation, and rising demand from major end-use industries such as automotive and aerospace. Rapid industrialization across emerging economies, including India, China, and Southeast Asia is further strengthening market demand as these regions experience increasing production in automotive, aerospace, defense, and construction sectors, all of which rely heavily on high-precision metal cutting solutions. Continuous advancements in high-speed steel compositions, including titanium nitride coating technologies and improved metallurgical processing techniques, have significantly enhanced tool durability, wear resistance, and cutting performance, making these tools more suitable for precision machining applications. In addition, increasing adoption of lightweight materials in automotive manufacturing and advanced high-strength alloys in aerospace production is boosting demand for reliable cutting tools capable of maintaining accuracy under high-stress conditions. High-speed steel tools continue to remain widely used in manufacturing operations due to their cost efficiency, toughness, and versatility across multiple machining processes. These tools include drills, milling cutters, taps, reamers, and various other precision cutting instruments essential for industrial production.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.7 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 5.7% |

The end mills segment accounted for around USD 2 billion in 2025 and is projected to grow at a CAGR of 6.3% between 2026 and 2035. This segment leads the market due to its extensive use in milling applications across diverse manufacturing industries. High-speed steel end mills are widely used for producing slots, cavities, profiles, and complex geometries in metal components. Aerospace manufacturing relies on these tools for machining aluminum alloys, titanium, and other specialized materials requiring high precision. Automotive production facilities utilize end mills for manufacturing engine parts, transmission components, and structural assemblies. Their adaptability for both roughing and finishing operations enhances operational efficiency and reduces tool change requirements.

The aerospace segment held a 28.7% share in 2025 and is expected to grow at a CAGR of 6.3% through 2035. This dominance is attributed to strict precision standards and the complexity of aerospace components. Aircraft structural parts, engine systems, and landing gear assemblies require advanced machining processes supported by durable cutting tools. High-speed steel tools are favored in certain aerospace applications due to their toughness and resistance to edge chipping. The segment is further supported by the production of commercial aircraft, defense aircraft, and spacecraft components, all of which involve machining of difficult materials such as titanium alloys, stainless steels, and high-temperature resistant metals.

U.S. High-Speed Steel Metal Cutting Tools Market reached USD 1.2 billion in 2025 and is forecast to grow at a CAGR of 7% from 2026 to 2035. Market growth in the country is driven by strong aerospace manufacturing activity, automotive production, and advanced industrial machinery development. The defense sector contributes significantly due to its requirement for precision machining in military equipment and systems. The medical device industry also supports demand through specialized manufacturing of surgical instruments and implants. Broad-based industrial manufacturing activities further sustain consistent consumption of cutting tools across multiple applications.

Key players operating in the Global High-Speed Steel Metal Cutting Tools Market include Dormer Pramet, Sandvik Coromant, Kennametal, OSG Corporation, Seco Tools, Guhring, Sumitomo Electric Industries, Emuge-Franken, Vargus, BIG Kaiser (BIG DAISHOWA Americas), Niagara Cutter, Hannibal Carbide Tool, GWS Tool Group, Toolmex Industrial Solutions, and RTS Cutting Tools. Companies in the high-speed steel metal cutting tools market are focusing on continuous product innovation to enhance tool life, cutting precision, and heat resistance through advanced coatings and improved metallurgy. Manufacturers are expanding their production capabilities and investing in automated manufacturing technologies to improve efficiency and reduce production costs. Strategic partnerships with automotive, aerospace, and industrial OEMs are strengthening long-term supply agreements and ensuring stable demand. Firms are also emphasizing research and development to design tools compatible with advanced materials and high-speed machining applications. Geographic expansion into emerging manufacturing hubs is helping companies capture new demand centers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material Grade

- 2.2.4 Application

- 2.2.5 End Use Industry

- 2.2.6 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing aerospace and automotive manufacturing

- 3.2.1.2 Expansion of industrial manufacturing and machinery production

- 3.2.1.3 Rising demand for precision-engineered medical devices

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Competition from carbide and ceramic cutting tools

- 3.2.2.2 Fluctuating raw material costs and supply chain issues

- 3.2.3 Opportunities

- 3.2.3.1 Growing online retail and e-commerce platforms

- 3.2.3.2 Expansion in emerging markets and youth participation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Value/Cost-plus) (Driven by Primary Research)

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.10.3 HS Code Classification & Trade Flow Analysis

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Modern vs. Traditional Trade) (Driven by Primary Research)

- 3.12.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 End mills

- 5.3 Drills

- 5.4 Taps

- 5.5 Reamers

- 5.6 Broaches

- 5.7 Others (countersinking etc.)

Chapter 6 Market Estimates & Forecast, By Material Grade, 2022 - 2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 T series

- 6.3 M series

- 6.4 Others (cobalt steel etc.)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Turning

- 7.3 Milling

- 7.4 Drilling

- 7.5 Tapping

- 7.6 Others (threading etc.)

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Aerospace

- 8.3 Medical

- 8.4 Automotive

- 8.5 Industrial manufacturing

- 8.6 Construction

- 8.7 Others (electronics & electrical etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Top Global Player

- 11.1.1 Sandvik Coromant

- 11.1.2 Kennametal

- 11.1.3 Sumitomo Electric Industries

- 11.1.4 Seco Tools

- 11.1.5 OSG Corporation

- 11.1.6 Dormer Pramet

- 11.2 Regional Player

- 11.2.1 Emuge-Franken

- 11.2.2 Niagara Cutter

- 11.2.3 BIG Kaiser (BIG DAISHOWA Americas)

- 11.2.4 Guhring

- 11.2.5 Vargus

- 11.3 Emerging Players

- 11.3.1 RTS Cutting Tools

- 11.3.2 Hannibal Carbide Tool

- 11.3.3 Toolmex Industrial Solutions

- 11.3.4 GWS Tool Group