PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061301

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061301

Asia-Pacific High-Speed Steel Metal Cutting Tools Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

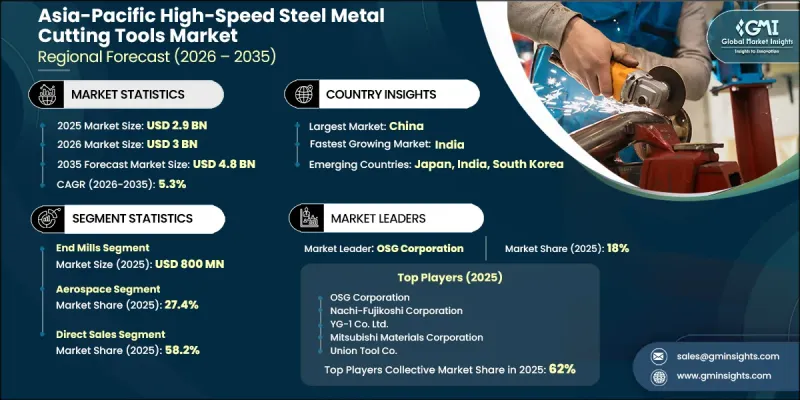

Asia-Pacific High-Speed Steel Metal Cutting Tools Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 4.8 billion by 2035.

The market across Asia-Pacific is witnessing expansion due to rapid industrial development, increasing automation across manufacturing facilities, and rising demand for advanced machining solutions. Growth in industrial production and ongoing investments in precision engineering continue to create favorable opportunities for high-speed steel metal cutting tools throughout the region. Expanding manufacturing capabilities and increasing focus on operational efficiency are encouraging companies to adopt durable and high-performance cutting solutions. Rising demand from major industrial sectors is also supporting broader market growth as manufacturers seek improved accuracy, productivity, and machine consistency. In addition, the shift toward advanced production technologies and precision-based manufacturing processes is accelerating the adoption of innovative cutting tools developed using premium-grade materials. Digital distribution channels are further strengthening market accessibility by allowing manufacturers and buyers to access technical specifications, product information, and advanced tooling solutions more efficiently. The growing emphasis on long-lasting performance, tool reliability, and machining precision continues to drive demand for high-speed steel metal cutting tools across the Asia-Pacific region.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 5.3% |

The end mills segment accounted for 27.5% share, generating USD 800 million in 2025. Demand for end mills continues to increase due to their versatility and ability to support complex milling applications and precision machining operations. Manufacturers are increasingly adopting these tools to improve machining flexibility and achieve higher levels of cutting accuracy across a wide range of industrial applications. Product advancements, including improved tool geometries, enhanced coatings, and optimized cutting performance, are further supporting segment growth. The ability of end mills to deliver reliable results in demanding machining environments continues to strengthen their market position throughout the region.

The aerospace segment held a share of 27.4% in 2025 and generated USD 800 million in revenue. Strong demand from aerospace manufacturing continues to support market growth due to the industry's strict quality standards and increasing requirement for precision-machined components. Manufacturers operating in the aerospace sector are investing in advanced cutting tools capable of handling complex materials and maintaining consistent performance under challenging production conditions. The need for highly specialized tooling solutions that support precision engineering and efficient machining processes remains a key growth driver for this segment. Continuous innovation in cutting tool design and material performance is also contributing to increased adoption across aerospace manufacturing operations.

China High-Speed Steel Metal Cutting Tools Market held a 32.1% share, generating USD 900 million in 2025. China's leadership position is supported by its extensive manufacturing infrastructure, rapid industrial development, and growing demand for precision machining technologies. Expanding industrial capabilities and rising investments in advanced manufacturing processes continue to strengthen demand for premium-quality metal cutting tools across the country. Chinese manufacturers are increasingly prioritizing machining accuracy, production efficiency, and high-performance tooling solutions to meet evolving industrial standards and maintain competitiveness in global manufacturing operations.

Major companies operating in the Asia-Pacific High-Speed Steel Metal Cutting Tools Market include Addison & Co. Ltd., BIG DAISHOWA SEIKI CO., LTD., DHF Precision Tool Co., Ltd., Fuji Tool Co., Ltd., Korloy Inc., Kyocera Corporation, Mitsubishi Materials Corporation, Nachi-Fujikoshi Corporation, OSG Corporation, Sutton Tools, Taegutec Ltd., Tiangong International Company Limited, Tungaloy Corporation, Union Tool Co., Ltd., and YG-1 Co., Ltd. Companies operating in the Asia-Pacific high-speed steel metal cutting tools market are implementing multiple strategies to strengthen their market position and expand regional presence. Leading manufacturers are investing heavily in research and development to improve cutting efficiency, tool durability, and machining precision. Businesses are also focusing on advanced coatings, innovative tool geometries, and premium-grade steel materials to enhance product performance and operational lifespan. Strategic partnerships with distributors, industrial suppliers, and manufacturing companies are helping brands improve market reach and customer engagement. In addition, companies are expanding digital sales channels and technical support platforms to provide easier access to product specifications and application guidance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Material Grade

- 2.2.3 Application

- 2.2.4 End Use Industry

- 2.2.5 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing aerospace and automotive manufacturing activities

- 3.2.1.2 Rising demand for precision machining and high-performance tools

- 3.2.1.3 Innovation in tool coatings and material technology

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Competition from carbide and ceramic cutting tools

- 3.2.2.2 Rising raw material costs and supply chain complexities

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of medical device and aerospace manufacturing

- 3.2.3.2 Integration of advanced coatings and sustainable manufacturing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Value/Cost-plus) (Driven by Primary Research)

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.10.3 HS Code Classification & Trade Flow Analysis

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Modern vs. Traditional Trade) (Driven by Primary Research)

- 3.12.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 End mills

- 5.3 Drills

- 5.4 Taps

- 5.5 Reamers

- 5.6 Broaches

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Material Grade, 2022 - 2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 T series

- 6.3 M series

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Turning

- 7.3 Milling

- 7.4 Drilling

- 7.5 Tapping

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Aerospace

- 8.3 Medical

- 8.4 Automotive

- 8.5 Industrial manufacturing

- 8.6 Construction

- 8.7 Others (electronics & electrical etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 China

- 10.3 Japan

- 10.4 India

- 10.5 Australia

- 10.6 South Korea

- 10.7 Indonesia

- 10.8 Malaysia

- 10.9 Singapore

Chapter 11 Company Profiles

- 11.1 Top Global Player

- 11.1.1 OSG Corporation

- 11.1.2 Nachi-Fujikoshi Corporation

- 11.1.3 YG-1 Co., Ltd.

- 11.1.4 Mitsubishi Materials Corporation

- 11.1.5 Union Tool Co., Ltd.

- 11.1.6 Tungaloy Corporation

- 11.2 Regional Player

- 11.2.1 Kyocera Corporation

- 11.2.2 Korloy Inc.

- 11.2.3 Sutton Tools

- 11.2.4 Taegutec Ltd.

- 11.2.5 Tiangong International Company Limited

- 11.3 Emerging Players

- 11.3.1 BIG DAISHOWA SEIKI CO., LTD.

- 11.3.2 DHF Precision Tool Co., Ltd.

- 11.3.3 Addison & Co. Ltd.

- 11.3.4 Fuji Tool Co., Ltd.