PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038713

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038713

Orthopedic Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

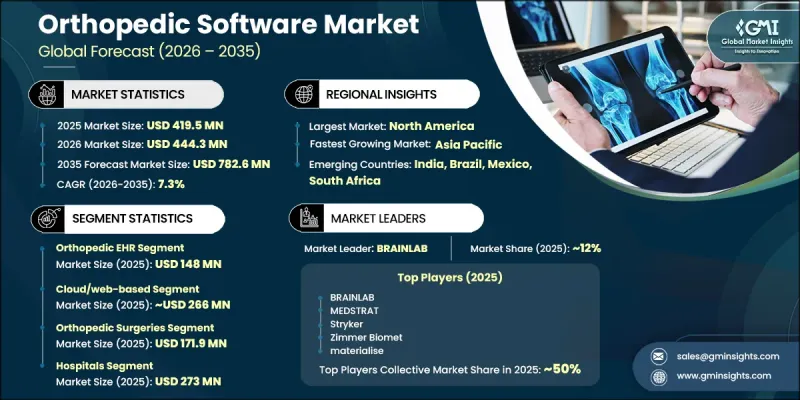

The Global Orthopedic Software Market was valued at USD 419.5 million in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 782.6 million by 2035.

Growth is supported by the rising incidence of orthopedic disorders and the increasing preference for minimally invasive surgical procedures. Orthopedic software is designed to support clinicians in diagnosing, planning, and managing musculoskeletal conditions through advanced digital tools. These platforms enhance accuracy in clinical decision-making by enabling detailed analysis of diagnostic imaging, surgical simulation, and efficient patient data management. Increasing demand for improved surgical precision, better patient outcomes, and reduced revision procedures is further driving adoption. The rising burden of musculoskeletal conditions, fueled by aging populations and higher participation in sports and physical activities, is significantly contributing to market expansion. Growing emphasis on healthcare digitization and workflow efficiency is encouraging providers to adopt integrated software solutions that streamline orthopedic care delivery and improve overall operational performance across healthcare facilities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $419.5 Million |

| Forecast Value | $782.6 Million |

| CAGR | 7.3% |

The orthopedic software market is also advancing due to the growing integration of digital healthcare systems and the increasing need for interoperable platforms. Healthcare providers are focusing on improving coordination between clinical, administrative, and diagnostic workflows through advanced software solutions. Continuous technological improvements are enabling better data accessibility, improved imaging integration, and enhanced treatment planning capabilities. Rising awareness of value-based care models is further encouraging the adoption of digital orthopedic solutions that improve efficiency and reduce treatment variability. Expanding healthcare infrastructure and increasing investment in digital health technologies are also contributing to sustained market growth across global regions.

The orthopedic EHR segment accounted for USD 148 million in 2025. Its dominance is driven by its ability to streamline clinical documentation and improve workflow efficiency across orthopedic practices. These systems are widely adopted due to their customization for musculoskeletal care, supporting functions such as injury tracking, implant documentation, and treatment outcome monitoring. Increasing demand for integrated patient records and seamless connectivity with imaging and billing systems is further strengthening segment growth. The shift toward data-driven healthcare delivery continues to reinforce its importance in orthopedic care environments.

The cloud/web-based segment reached USD 266 million in 2025. This segment is gaining strong traction due to its scalability, cost efficiency, and ease of implementation across healthcare facilities of varying sizes. It enables real-time data access, remote collaboration, and smooth integration with other healthcare systems. Growing preference for subscription-based models and reduced infrastructure requirements is further accelerating adoption. Enhanced data security measures and continuous software updates are also supporting widespread use of cloud-based orthopedic solutions.

North America Orthopedic Software Market generated USD 164.6 million in 2025. The region benefits from advanced healthcare infrastructure, strong digital adoption, and increasing demand for integrated clinical systems. Healthcare providers across the region are rapidly adopting digital orthopedic solutions to enhance operational efficiency and improve patient outcomes. The growing shift toward cloud-based platforms, combined with regulatory support for electronic health record adoption and data interoperability, is further strengthening market growth across hospitals, clinics, and surgical centers.

Key companies operating in the Orthopedic Software Market include Siemens Healthineers, Stryker, GE HealthCare, Philips, McKESSON, Zimmer Biomet, BRAINLAB, Carestream, Esaote, Intellijoint Surgical, Materialise, MEDSTRAT and Surgimap. Companies in the orthopedic software market are focusing on innovation, integration, and strategic expansion to strengthen their market position. They are investing in advanced technologies such as artificial intelligence and data analytics to improve diagnostic accuracy and surgical planning capabilities. Strategic partnerships with hospitals and healthcare networks are helping companies expand product adoption and enhance workflow integration. Many firms are prioritizing cloud-based solutions to improve scalability, accessibility, and cost efficiency. Continuous upgrades in interoperability and system integration are enabling seamless connectivity across healthcare platforms.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Delivery mode trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.2.5 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of orthopedic disorders

- 3.2.1.2 Technological advancements in orthopedic software

- 3.2.1.3 Growing demand for minimally invasive surgeries

- 3.2.1.4 Surging demand for improved surgical outcomes, efficiency, and reduced revision rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Potential risks of software malfunction

- 3.2.2.2 High implementation and maintenance costs

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for AI-enabled surgical planning and decision-support software

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends (Driven by primary research)

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by primary research)

- 3.7 Patent landscape (Driven by Primary Research)

- 3.8 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Orthopedic EHR

- 5.3 Orthopedic PACS

- 5.4 Orthopedic RCM

- 5.5 Orthopedic practice management

- 5.6 Digital templating/Preoperative planning software

Chapter 6 Market Estimates and Forecast, By Delivery Mode, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Cloud/web-based

- 6.3 On premises

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Orthopedic surgeries

- 7.3 Fracture management

- 7.4 Joint replacement

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 BRAINLAB

- 10.2 Carestream

- 10.3 Esaote

- 10.4 GE HealthCare

- 10.5 intellijoint surgical

- 10.6 materialise

- 10.7 McKESSON

- 10.8 MEDSTRAT

- 10.9 merative

- 10.10 Philips

- 10.11 Siemens Healthineers

- 10.12 Stryker

- 10.13 Surgimap

- 10.14 Zimmer Biomet