PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038742

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038742

Connected Motorcycle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

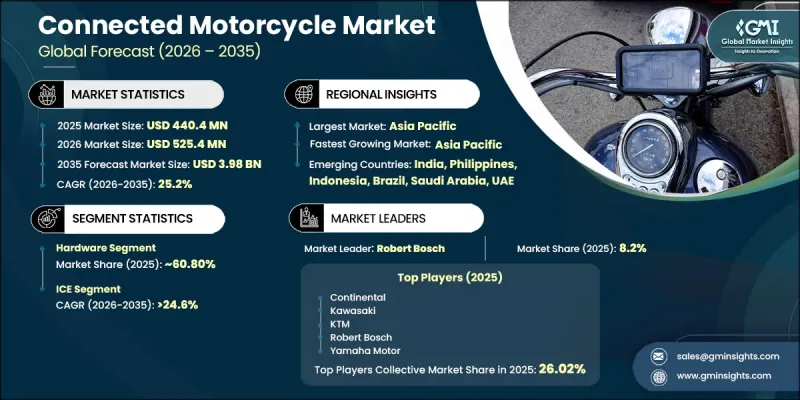

The Global Connected Motorcycle Market was valued at USD 440.4 million in 2025 and is estimated to grow at a CAGR of 25.2% to reach USD 3.98 billion by 2035.

The growing adoption of connected motorcycles is driven by safety features, such as collision warnings, blind-spot monitoring, and real-time traffic updates. These advancements reduce accidents, increase rider adoption, and create demand for embedded connectivity solutions across both consumer and fleet markets. The expansion of electric motorcycles and scooters further fuels the demand for connectivity, allowing for better battery management, performance monitoring, and over-the-air updates. Connected motorcycles also support urban delivery services, ride-hailing companies, and logistics fleets by enabling route optimization, predictive maintenance, and real-time tracking. The subscription-based telematics services have opened avenues for recurring revenue, promoting the use of tethered or embedded connectivity, which is accelerating the commercial market for these vehicles. Motorcycle manufacturers are focusing on integrating sensors, cameras, and Vehicle-to-Everything (V2X) communication to improve rider safety, enhance operational efficiency, and increase the adoption of advanced connectivity features. These systems are increasingly being designed to work seamlessly with smart infrastructure, such as smart cities, to offer always-connected capabilities globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $ 440.4 Million |

| Forecast Value | $3.98 Billion |

| CAGR | 25.2% |

The hardware segment held a 60.80% share in 2025 and is anticipated to grow at a CAGR of 24.1% through 2035. The integration of sensors like GNSS/GPS, accelerometers, and components of Advanced Rider Assistance Systems (ARAS) is transforming motorcycles into highly connected vehicles. These sensors not only provide safety features but also enable predictive maintenance and real-time diagnostics, offering a more sophisticated experience for riders. Manufacturers are now focusing on developing compact, low-power telematics control units (TCUs), displays, and communication modules to ensure connectivity while minimizing the impact on battery life and vehicle performance, especially in the electric motorcycle sector.

The cellular segment accounted for the largest share of the market in 2025, driven by its capability to support real-time, long-distance communication across vehicles, cloud systems, and external networks. In contrast to short-range options like Bluetooth, cellular connectivity enables uninterrupted data flow for functions such as navigation, system monitoring, security tracking, and emergency support, making it a critical component for advanced connected features and a smooth user experience. In addition, the ongoing rollout of 4G and the emergence of 5G technologies are significantly improving network speed, stability, and data handling capacity.

China Connected Motorcycle Market held a 64.9% share, generating USD 124 million in 2025. The market in China is expanding rapidly due to accelerating urban development, increasing consumer spending power, and growing adoption of smart mobility technologies. Widespread smartphone usage and robust high-speed internet infrastructure are enabling seamless integration of features such as navigation, real-time monitoring, and app-based controls, which is influencing consumer demand for technologically advanced motorcycles. Furthermore, the country's strong focus on electric mobility and intelligent transportation development is supporting the growth of connected motorcycles, while ongoing investments by domestic and global manufacturers are further strengthening the ecosystem for IoT-enabled two-wheelers.

Prominent players in the Connected Motorcycle Market include companies like BMW Motorrad, Ducati, Yamaha, Kawasaki, Honda, Harley-Davidson, KTM, Piaggio, Robert Bosch, and Continental. These companies are driving innovation in connected motorcycle technologies, focusing on safety and performance features that enhance the riding experience. To strengthen their market position, companies in the connected motorcycle industry are investing heavily in research and development to integrate cutting-edge technologies such as telematics, V2X communication, and ARAS into their motorcycles. By embedding advanced safety systems and connectivity solutions, they are offering a higher value proposition to consumers. In addition, many companies are focusing on creating seamless integration with mobile apps and telematics platforms, allowing riders to monitor and optimize their motorcycles' performance.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast Model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Connectivity

- 2.2.4 Propulsion

- 2.2.5 Network

- 2.2.6 End use

- 2.2.7 Motorcycle Type

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing Demand for Rider Safety and Assistance Systems

- 3.2.1.2 Rising Adoption of IoT and Telematics

- 3.2.1.3 Growth in Urban Mobility and Smart Transportation

- 3.2.1.4 Expansion of Electric Connected Motorcycles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Cost of Connected Systems

- 3.2.2.2 Data Security and Privacy Concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI, 5G, and V2X Technologies

- 3.2.3.2 Growth in Emerging Markets

- 3.2.3.3 Subscription-Based and Mobility Services

- 3.2.3.4 Predictive Maintenance and OTA Updates

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and Innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory guideline

- 3.6.1 North America

- 3.6.1.1 U.S.: NHTSA Vehicle Safety Standards, FCC V2X Regulations

- 3.6.1.2 Canada: Motor Vehicle Safety Regulations (MVSR), Transport Canada Cybersecurity Guidelines

- 3.6.2 Europe

- 3.6.2.1 Germany: EU General Safety Regulation (GSR), eCall Regulation

- 3.6.2.2 UK: UK Vehicle Type Approval Regulations, Connected Vehicle Cybersecurity Standards

- 3.6.2.3 France: French Road Safety Code, Intelligent Transport Systems (ITS) Framework

- 3.6.2.4 Italy: Italian Highway Code, EU Vehicle Connectivity Compliance Standards

- 3.6.3 Asia Pacific

- 3.6.3.1 China: MIIT Intelligent Connected Vehicle (ICV) Policy, V2X Standards

- 3.6.3.2 India: AIS Standards, Bharat NCAP Framework

- 3.6.3.3 Japan: MLIT ITS Regulations, Road Transport Vehicle Safety Standards

- 3.6.3.4 Australia: Australian Design Rules (ADR), Vehicle Cybersecurity Guidelines

- 3.6.4 Latin America

- 3.6.4.1 Brazil: CONTRAN Vehicle Safety Regulations, ABS Mandate Standards

- 3.6.4.2 Mexico: NOM Vehicle Standards, Road Transport Safety Regulations

- 3.6.4.3 Argentina: ANSV Road Safety Regulations, National Vehicle Compliance Standards

- 3.6.5 MEA

- 3.6.5.1 UAE: ESMA Vehicle Standards, Smart Mobility Regulations

- 3.6.5.2 Saudi Arabia: SASO Vehicle Standards, Vision 2030 Mobility Framework

- 3.6.5.3 3.7.5.3 South Africa: National Road Traffic Act, SABS Vehicle Standards

- 3.6.1 North America

- 3.7 PESTEL analysis

- 3.8 Patent Landscape (Driven by Primary Research)

- 3.9 Trade Data Analysis (Based on Paid Database)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, Limitations & Regulatory Considerations

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Production Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipelines

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.13.2 Optimistic Scenarios - Favourable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 TCU

- 5.2.2 Display

- 5.2.3 Sensors

- 5.2.4 Others

- 5.3 Software

- 5.4 Services

- 5.4.1 Professional service

- 5.4.2 Managed services

Chapter 6 Market Estimates & Forecast, By Connectivity, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Embedded

- 6.3 Tethered

- 6.4 Aftermarket

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

- 7.3.1 PHEV

- 7.3.2 HEV

- 7.3.3 FCEV

- 7.3.4 BEV

Chapter 8 Market Estimates & Forecast, By Network, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Cellular

- 8.3 Short range

- 8.4 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Private

- 9.3 Commercial

Chapter 10 Market Estimates & Forecast, By Motorcycle Type, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 Sport Motorcycles

- 10.3 Touring Motorcycles

- 10.4 Roadster / Naked Bikes

- 10.5 Heritage / Cruiser Bikes

- 10.6 Adventure Motorcycles

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Belgium

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Philippines

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Leaders

- 12.1.1 BMW Motorrad

- 12.1.2 Continental

- 12.1.3 Ducati

- 12.1.4 Harley-Davidson

- 12.1.5 Honda

- 12.1.6 Kawasaki Heavy Industries

- 12.1.7 KTM

- 12.1.8 Piaggio

- 12.1.9 Robert Bosch

- 12.1.10 Suzuki Motor.

- 12.1.11 Triumph Motorcycles

- 12.1.12 Yamaha Motor

- 12.2 Regional Champions

- 12.2.1 Ather Energy

- 12.2.2 Bajaj Auto

- 12.2.3 CFMoto

- 12.2.4 Gogoro

- 12.2.5 Hero MotoCorp

- 12.2.6 Indian Motorcycle

- 12.2.7 NIU Technologies

- 12.2.8 Ola Electric

- 12.2.9 Royal Enfield

- 12.2.10 TVS Motor Company

- 12.3 Emerging Players

- 12.3.1 LiveWire

- 12.3.2 Revolt Motors

- 12.3.3 Zero Motorcycles