PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038743

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038743

Spain Construction Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

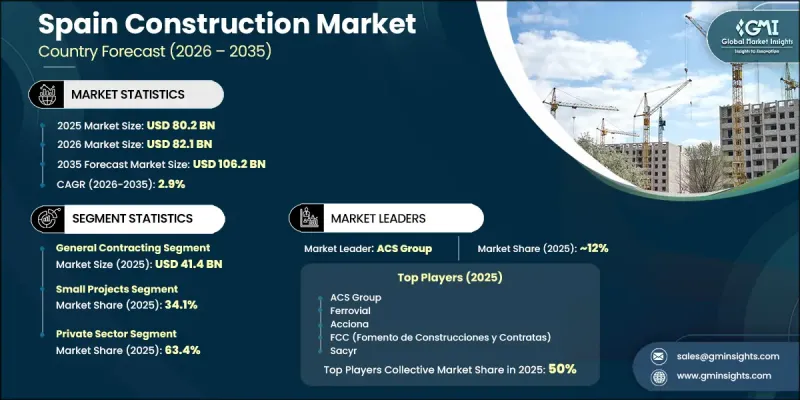

Spain Construction Market was valued at USD 80.2 billion in 2025 and is estimated to grow at a CAGR of 2.9% to reach USD 106.2 billion by 2035.

Market growth in Spain is supported by ongoing public infrastructure development, expansion of renewable energy projects, and sustained government-backed economic recovery initiatives. Construction activity continues to play a vital role in the country's economic structure, contributing significantly to employment generation and regional development. The sector spans residential, commercial, and infrastructure construction, with projects being executed through both public and private investments across the country. Spain remains one of the most prominent construction markets in Europe, supported by a strong presence of established domestic and international contractors. The industry is benefiting from substantial financial backing through European Union funding programs and Spain's Recovery, Transformation, and Resilience Plan, which is accelerating infrastructure modernization and sustainability-focused development. Construction companies are increasingly adopting advanced technologies and modern building techniques to improve efficiency, reduce costs, and meet evolving regulatory requirements. There is also a growing emphasis on sustainable construction practices and renewable energy integration within infrastructure projects. The sector is steadily transitioning from traditional methods toward more innovative and technology-driven construction approaches, supporting long-term market evolution and competitiveness across all major project categories.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $80.2 Billion |

| Forecast Value | $106.2 Billion |

| CAGR | 2.9% |

The general contracting segment accounted for USD 41.4 billion, representing 51.7% of share in 2025. This delivery model continues to dominate due to its structured approach, where contractors execute construction work based on client-provided or independently developed designs. It is particularly widely used in public infrastructure development, where design and construction responsibilities are managed separately. General contractors oversee subcontractors, procurement activities, workforce management, and project execution, while design responsibilities typically remain with external consultants, ensuring clear role separation throughout project delivery.

The small projects segment held a 34.1% share with a value of USD 27.38 billion in 2025. This segment includes many localized construction activities such as residential developments, small-scale commercial buildings, renovation work, minor infrastructure upgrades, and civil engineering projects. Although individually smaller in scale, these projects collectively form a significant share of total construction activity and provide steady demand for regional contractors. They also serve as a key source of employment and business continuity for local construction firms across Spain.

Sacyr, Ferrovial, ACS Group, Acciona, OHLA, FCC (Fomento de Construcciones y Contratas), Dragados, Vinci, Skanska, Eiffage, Bouygues Construction, Elecnor, AZVI (Grupo Azvi), COMSA Corporacion, and Tecnicas Reunidas are among the key companies operating in the Spain Construction Industry. Companies in the Spain Construction Market are focusing on digital transformation, sustainable building practices, and infrastructure diversification to strengthen their market position. They are increasingly adopting advanced construction technologies such as BIM, automation, and smart project management tools to improve efficiency and reduce project timelines. Sustainability is also a major focus, with firms integrating green building materials and renewable energy solutions into infrastructure development. Strategic participation in public-private partnerships helps companies secure large-scale projects while ensuring long-term revenue stability. Firms are also expanding their presence in renewable energy infrastructure and transportation projects to align with national development priorities.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Construction Type

- 2.2.2 Contracting Type

- 2.2.3 Scale

- 2.2.4 End User

Chapter 3 Spain Construction Market Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Economic growth and government investments

- 3.2.1.2 Government programs for smart city development

- 3.2.1.3 Rapid urbanization and population growth

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Regulatory delays and administrative bottlenecks

- 3.2.4 Skilled labor shortages and rising construction costs

- 3.2.1 Growth drivers

- 3.3 Opportunities

- 3.3.1 Affordable housing construction boom

- 3.3.2 Defense and security infrastructure investment

- 3.4 Growth potential analysis

- 3.5 Future market trends

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Pricing Analysis (Driven by Primary Research)

- 3.7.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.7.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.8 Regulatory landscape

- 3.8.1 Spanish Building Code (Codigo Tecnico de la Edificacion)

- 3.8.2 Public Procurement & Contractor Classification System

- 3.8.3 Environmental & Sustainability Regulations

- 3.8.4 Health & Safety Standards

- 3.9 Trade Data Analysis (Driven by Paid Data Source)

- 3.9.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.9.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.12.3 Risks, Limitations & Regulatory Considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Spain Construction Market Estimates & Forecast, By Construction Type (USD Billion)

- 5.1 Key trends

- 5.2 Residential Construction

- 5.2.1 Single-Family Homes

- 5.2.2 Multi-Family Apartment Complexes

- 5.2.3 Social Housing & Affordable Housing

- 5.2.4 Luxury Residential Developments

- 5.3 Non-Residential Building Construction

- 5.3.1 Commercial Buildings

- 5.3.1.1 Office Buildings

- 5.3.1.2 Retail Centers & Shopping Malls

- 5.3.1.3 Hotels & Hospitality Facilities

- 5.3.2 Institutional Buildings (Healthcare, Educational, Government)

- 5.3.2.1 Healthcare Facilities (Hospitals, Clinics)

- 5.3.2.2 Educational Facilities (Schools, Universities)

- 5.3.2.3 Government & Public Buildings

- 5.3.3 Industrial Buildings

- 5.3.3.1 Manufacturing Facilities

- 5.3.3.2 Warehouses & Logistics Centers

- 5.3.3.3 Data Centers

- 5.3.1 Commercial Buildings

- 5.4 Infrastructure & Civil Engineering Construction

- 5.4.1 Transportation Infrastructure

- 5.4.1.1 Roads & Highways

- 5.4.1.2 Railways & Metro Systems

- 5.4.1.3 Airports

- 5.4.1.4 Ports & Maritime Infrastructure

- 5.4.2 Utilities Infrastructure

- 5.4.2.1 Water Supply & Wastewater Treatment

- 5.4.2.2 Energy Generation & Transmission

- 5.4.2.3 Telecommunications Networks

- 5.4.1 Transportation Infrastructure

- 5.5 Specialized Construction

- 5.5.1 Renovation/Remodelling Construction

- 5.5.2 Sustainable & Environmental Construction

- 5.5.3 Sports & Recreation Facilities

- 5.5.4 Mixed-Use Developments

Chapter 6 Spain Construction Market Estimates & Forecast, By End-User (USD Billion)

- 6.1 Key trends

- 6.2 Private sector

- 6.3 Public sector

Chapter 7 Spain Construction Market Estimates & Forecast, By Contracting Type (USD Billion)

- 7.1 Key trends, by contracting type

- 7.2 General contracting

- 7.3 Design-build contracting

- 7.4 Construction management

Chapter 8 Spain Construction Market Estimates & Forecast, By Scale (USD Billion)

- 8.1 Key trends, by scale

- 8.2 Mega project

- 8.3 Major project

- 8.4 Medium project

- 8.5 Small project

Chapter 9 Company Profiles

- 9.1 Acciona

- 9.2 ACS

- 9.3 AZVI

- 9.4 Bouygues Construction

- 9.5 COMSA Corporacion

- 9.6 Dragados

- 9.7 Eiffage

- 9.8 Elecnor

- 9.9 FCC

- 9.10 Ferrovial

- 9.11 OHLA

- 9.12 Sacyr

- 9.13 Skanska

- 9.14 Tecnicas Reunidas

- 9.15 Vinci