PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038772

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038772

Automotive Ethernet PHY Chip Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

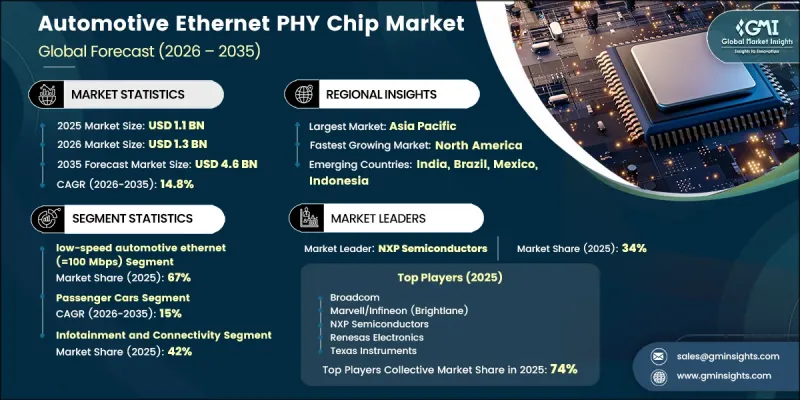

The Global Automotive Ethernet PHY Chip Market was valued at USD 1.1 billion in 2025 and is estimated to grow at a CAGR of 14.8% to reach USD 4.6 billion by 2035.

Market growth is driven by the rapid evolution of in-vehicle electronic architectures that require faster, more reliable, and higher-bandwidth communication systems. Automotive Ethernet PHY chips play a critical role in enabling stable data transmission across complex vehicle networks using single unshielded twisted pair cables. Increasing integration of advanced digital systems in vehicles is accelerating demand for robust communication interfaces that can support real-time data exchange. The expansion of connected mobility, electrification trends, and software-defined vehicle platforms is further strengthening the need for scalable networking solutions. At the same time, rising adoption of advanced driver assistance systems and autonomous driving technologies is pushing automotive manufacturers to deploy high-speed communication infrastructure, reinforcing the importance of Ethernet PHY chips in next-generation vehicle design.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.1 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 14.8% |

The automotive Ethernet PHY chip market is also shaped by growing requirements for safety, reliability, and energy-efficient communication systems in modern vehicles. These chips are designed to withstand harsh automotive environments, including extreme temperature variations, electromagnetic interference, and continuous mechanical vibration, ensuring long-term operational stability. Compliance with stringent automotive quality and functional safety standards further enhances their adoption across global vehicle platforms.

The low-speed automotive Ethernet segment (<=100 Mbps) segment held 67% share in 2025. This segment continues to lead due to its widespread integration in existing vehicle communication architectures. It supports efficient full-duplex data transmission over single unshielded twisted pair cables, making it suitable for infotainment systems, gateway functions, and basic in-vehicle connectivity applications.

The passenger cars segment is expected to grow at a CAGR of 15% from 2026 to 2035. This category includes multiple vehicle types and remains the primary adopter of automotive Ethernet PHY chips due to increasing electronic content and connectivity demand. Passenger vehicles integrate multiple PHY chips across infotainment systems, camera-based safety systems, gateways, and body electronics, driven by rising consumer expectations for advanced safety and digital features.

China Automotive Ethernet PHY Chip Market reached USD 330.5 million in 2025 supported by strong policy initiatives promoting intelligent and connected vehicles. Expanding adoption of digital cockpit systems, autonomous driving technologies, and telematics solutions is encouraging local manufacturers to incorporate high-speed networking architectures into new vehicle platforms.

Key players operating in the Global Automotive Ethernet PHY Chip Industry include Texas Instruments, Broadcom, Analog Devices, Qualcomm Technologies, NXP Semiconductors, Microchip Technology, Intel, MaxLinear, Marvell / Infineon, and Cadence Design Systems (PHY IP). Companies in the Automotive Ethernet PHY Chip Market focus on advanced product innovation, energy-efficient design, and compliance with stringent automotive safety standards to strengthen their market position. Manufacturers are investing heavily in next-generation high-speed PHY solutions that support increasing data traffic in connected and autonomous vehicles. Strategic partnerships with automotive OEMs and Tier-1 suppliers are helping accelerate integration of Ethernet technologies into new vehicle platforms. Companies are also expanding R&D capabilities to enhance signal integrity, reduce power consumption, and improve system reliability under harsh operating conditions. In addition, firms are scaling production capacity and strengthening supply chain resilience to meet rising global demand.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast Model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of EVs and ADAS

- 3.2.1.2 Shift to software-defined vehicles (SDV)

- 3.2.1.3 Rising vehicle production in emerging markets

- 3.2.1.4 Demand for low-latency, secure data transmission

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development costs for automotive-grade chips

- 3.2.2.2 Cybersecurity vulnerabilities in connected systems

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in autonomous driving and V2X ecosystems

- 3.2.3.2 Expansion of EV battery management and telematics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration safety regulations

- 3.4.1.2 ISO 26262 functional safety standards

- 3.4.1.3 Automotive cybersecurity requirements

- 3.4.1.4 Personal Information Protection and Electronic Documents Act (PIPEDA)

- 3.4.2 Europe

- 3.4.2.1 EU General Safety Regulation

- 3.4.2.2 General Data Protection Regulation (GDPR)

- 3.4.2.3 UNECE R155, R156

- 3.4.2.4 ISO 26262, IEC 61508

- 3.4.3 Asia Pacific

- 3.4.3.1 China (PIPL, CSL, DSL, automotive data laws)

- 3.4.3.2 India (AIS, Bharat NCAP)

- 3.4.3.3 Japan mobility regulations

- 3.4.3.4 South Korea cybersecurity laws

- 3.4.4 Latin America

- 3.4.4.1 Brazil (LGPD, safety standards)

- 3.4.4.2 Mexico automotive regulations

- 3.4.4.3 Argentina frameworks

- 3.4.4.4 Regional certifications

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE mobility regulations

- 3.4.5.2 Saudi Arabia safety & cybersecurity

- 3.4.5.3 South Africa safety & data laws

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing Analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-Driven Disruption of Existing Business Models

- 3.9.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Sustainability & environmental aspects

- 3.10.1 Carbon Footprint Assessment

- 3.10.2 Circular Economy Integration

- 3.10.3 E-Waste Management Requirements

- 3.10.4 Green Manufacturing Initiatives

- 3.11 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.11.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.11.2 Optimistic Scenarios - Favourable macro and industry tailwinds

- 3.11.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Company tier benchmarking

- 4.7.1 Tier classification criteria & qualifying thresholds

- 4.7.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, units)

- 5.1 Key trends

- 5.2 Low-Speed Automotive Ethernet (=100 Mbps)

- 5.2.1 10BASE-T1S

- 5.2.2 100BASE-T1

- 5.3 Gigabit Automotive Ethernet (1000BASE-T1)

- 5.4 Multi-Gigabit Automotive Ethernet (>1 Gbps)

- 5.4.1 2.5/5/10GBASE-T1

- 5.4.2 Future Standards (25G+)

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger Cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial Vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 ADAS and Autonomous Driving

- 7.2.1 Radar Systems

- 7.2.2 LiDAR Sensors

- 7.2.3 Cameras

- 7.2.4 Sensor Fusion

- 7.2.5 Domain Controllers

- 7.3 Infotainment and Connectivity

- 7.3.1 Display Systems

- 7.3.2 Audio Systems

- 7.3.3 Telematics

- 7.3.4 Over-the-Air Updates

- 7.3.5 Connectivity Gateways

- 7.4 Powertrain and Vehicle Dynamics

- 7.4.1 Engine Control

- 7.4.2 Transmission Control

- 7.4.3 Battery Management

- 7.4.4 Chassis Control

- 7.4.5 Thermal Management

- 7.5 Body Electronics and Comfort

- 7.5.1 Door Modules

- 7.5.2 Lighting Systems

- 7.5.3 Climate Control

- 7.5.4 Seat Control

- 7.5.5 Access Control

- 7.6 Gateway and Backbone

- 7.6.1 Central Gateways

- 7.6.2 Zone Controllers

- 7.6.3 Ethernet Switches

- 7.6.4 Diagnostic Systems

- 7.6.5 Security Gateways

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Nordics

- 8.3.7 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Players

- 9.1.1 Analog Devices

- 9.1.2 Broadcom

- 9.1.3 Marvell / Infineon

- 9.1.4 Intel

- 9.1.5 Marvell Technology

- 9.1.6 NXP Semiconductors

- 9.1.7 Qualcomm Technologies

- 9.1.8 Texas Instruments

- 9.2 Regional Players

- 9.2.1 Cadence Design Systems (PHY IP)

- 9.2.2 MaxLinear

- 9.2.3 MediaTek

- 9.2.4 onsemi

- 9.2.5 Realtek Semiconductor

- 9.2.6 Renesas Electronics

- 9.2.7 Rohm Semiconductor

- 9.2.8 STMicroelectronics

- 9.3 Emerging Players/Disruptors

- 9.3.1 Alphawave IP

- 9.3.2 Aquantia

- 9.3.3 Canova Tech

- 9.3.4 Ethernovia

- 9.3.5 Kandou Bus

- 9.3.6 Valens Semiconductor