PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038778

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038778

Continuous Glucose Monitoring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

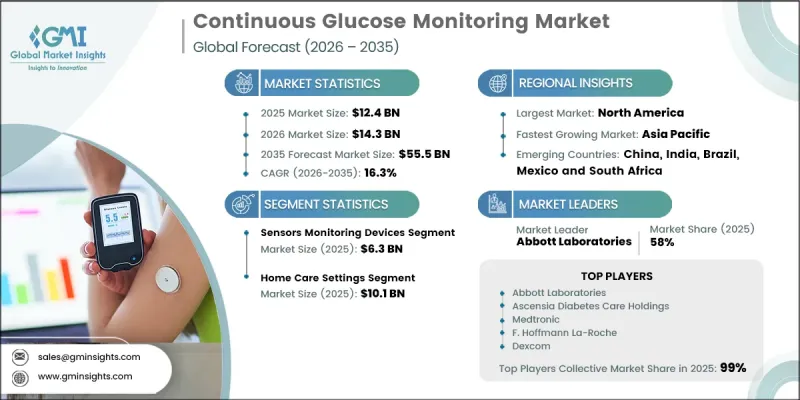

The Global Continuous Glucose Monitoring Market was valued at USD 12.4 billion in 2025 and is estimated to grow at a CAGR of 16.3% to reach USD 55.5 billion by 2035.

Market expansion is influenced by the escalating global burden of diabetes, rising preference for real-time glucose tracking solutions, continuous improvements in wearable medical technologies, and increasing public health initiatives aimed at diabetes awareness and management. Growing demand for accurate and continuous monitoring tools is reshaping diabetes care, as patients and healthcare providers shift toward data-driven treatment approaches. Technological progress in sensor miniaturization, wireless connectivity, and mobile integration is further enhancing device usability and clinical efficiency. Continuous glucose monitoring systems are gaining traction as they provide real-time insights into glucose fluctuations, helping reduce complications associated with delayed detection. Increasing adoption of remote and home-based care models is also supporting market penetration. Additionally, expanding healthcare access, improved reimbursement frameworks, and rising patient education levels are encouraging wider utilization of CGM systems across both developed and emerging healthcare markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.4 Billion |

| Forecast Value | $55.5 Billion |

| CAGR | 16.3% |

The sensor-based monitoring devices segment accounted for USD 6.3 billion in 2025. This segment continues to expand due to ongoing improvements in sensor precision, durability, and overall performance. Modern sensor technologies have significantly enhanced measurement accuracy, with advanced systems achieving a mean absolute relative difference below 10%. Enhanced miniaturization has also improved patient comfort, making long-term usage more practical and widely accepted. These advancements are strengthening the role of sensor-based devices in continuous and reliable glucose tracking.

The home care settings segment reached USD 10.1 billion in 2025. Adoption in this segment is increasing as continuous glucose monitoring systems enable patients to track glucose levels in real time outside clinical environments. These devices support proactive diabetes management by allowing early identification of abnormal glucose fluctuations and reducing dependence on hospital visits. The growing shift toward decentralized healthcare delivery is accelerating the use of CGM solutions for long-term diabetes management, post-treatment monitoring, and elderly care, where continuous observation is essential for preventing complications.

U.S. Continuous Glucose Monitoring Market reached USD 5.7 billion in 2025. Market growth in the country is supported by high healthcare expenditure, strong availability of advanced medical technologies, and a rising diabetes population. Increasing adoption of digital health solutions and continuous monitoring devices is further contributing to market expansion. Favorable reimbursement frameworks have also improved access to CGM systems, enabling broader patient adoption and strengthening the overall market outlook.

Leading players such as Abbott Laboratories, Dexcom, Medtronic, Senseonics, F. Hoffmann-La Roche, A. Menarini Diagnostics, i-SENS, Medtrum Technologies, Med Trust, Sinocare, and Zhejiang POCTech continue to focus on product innovation and global expansion strategies to reinforce their competitive position. Companies in the Continuous Glucose Monitoring Market are focusing on continuous innovation in sensor accuracy, device miniaturization, and longer sensor lifespan to improve patient compliance and clinical reliability. They are expanding integration with smartphones and digital health platforms to enhance real-time data access and remote monitoring capabilities. Strategic collaborations with healthcare providers and insurers are helping improve reimbursement coverage and market accessibility. Manufacturers are also investing heavily in research and development to enhance algorithm-driven glucose prediction and improve user experience. Additionally, companies are strengthening global distribution networks and increasing investments in emerging markets to expand patient reach and accelerate adoption of advanced diabetes management solutions.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.1.1 Key market trends

- 2.1.2 Component trends

- 2.1.3 End use trends

- 2.1.4 Regional trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of diabetes, globally

- 3.2.1.2 Rising demand for continuous monitoring devices

- 3.2.1.3 Technological advancements in devices

- 3.2.1.4 Increasing government initiatives to generate awareness regarding diabetes

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost related to devices

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunity

- 3.2.3.1 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.1.1 Real time continuous glucose monitoring systems

- 3.5.1.2 Bluetooth enabled CGM sensors and transmitters

- 3.5.1.3 Mobile apps and cloud based CGM data platforms

- 3.5.2 Emerging technologies

- 3.5.2.1 AI driven glucose prediction and decision-support algorithms

- 3.5.2.2 Non invasive and minimally invasive glucose sensing technologies

- 3.5.2.3 Extended wear and multi-day CGM sensors

- 3.5.2.4 Fully integrated digital diabetes management ecosystems

- 3.5.1 Current technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Patent analysis (Driven by Primary Research)

- 3.8 Pricing analysis, 2025 (Driven by Primary Research)

- 3.9 Impact of AI and Generative AI on the market (Driven by Primary Research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Transmitters

- 5.3 Sensors

- 5.4 Receivers

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Home care settings

- 6.4 Diagnostic centres and clinics

- 6.5 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 A. Menarini Diagnostics

- 8.3 Dexcom

- 8.4 i-SENS

- 8.5 F. Hoffmann-La Roche

- 8.6 Med Trust

- 8.7 Medtronic

- 8.8 Medtrum Technologies

- 8.9 Senseonics

- 8.10 Sinocare

- 8.11 Zhejiang POCTech