PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038804

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038804

In-Car Wellness Monitoring System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

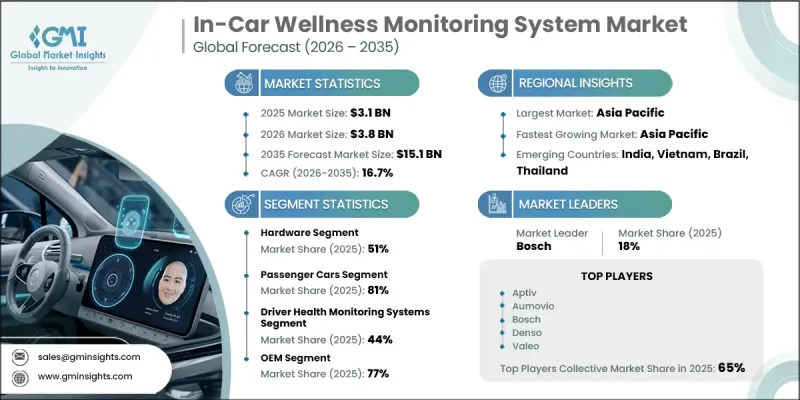

The Global In-Car Wellness Monitoring System Market was valued at USD 3.1 billion in 2025 and is estimated to grow at a CAGR of 16.7% to reach USD 15.1 billion by 2035.

Market expansion is driven by the rapid integration of biometric sensing technologies and intelligent cabin monitoring systems across modern vehicles. Automakers are increasingly embedding sensors, cameras, and radar-based solutions to track driver and passenger health indicators such as fatigue levels, heart activity, and stress conditions. Rising consumer expectations for enhanced in-vehicle safety, comfort, and personalized driving experiences are further accelerating adoption. The growing penetration of connected vehicles, luxury automobiles, and electric mobility platforms is also strengthening demand for advanced wellness monitoring solutions. In addition, ongoing advancements in artificial intelligence, sensor fusion, and real-time data analytics are enabling more accurate and predictive in-cabin health monitoring capabilities, supporting broader integration across mainstream automotive platforms.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Billion |

| Forecast Value | $15.1 Billion |

| CAGR | 16.7% |

The in-car wellness monitoring systems industry is also influenced by evolving automotive safety regulations and increasing emphasis on occupant well-being. Regional markets reflect differing adoption patterns, with Europe maintaining a leading position due to stringent safety frameworks and high acceptance of premium vehicles. Asia Pacific is experiencing rapid expansion driven by rising electric vehicle penetration and connected car adoption, while North America is progressing steadily with increasing regulatory support and growing demand for advanced automotive features.

The hardware segment held a 51% share and is expected to grow at a CAGR of 14.9% from 2026 to 2035. Demand is primarily driven by advanced imaging and sensing components, including high-resolution cabin cameras, infrared-enabled systems, and radar-based monitoring solutions. These technologies enable non-intrusive tracking of vital signs such as respiration patterns and micro-movements. Radar-enabled solutions are gaining traction due to their ability to provide contactless monitoring, while AI-based signal processing is enhancing system accuracy and reliability.

The OEM segment accounted for a 77% share in 2025, supported by widespread integration of wellness and safety monitoring features in new vehicle models. Automakers are embedding fatigue detection, biometric tracking, and cabin monitoring systems within advanced automotive platforms to enhance safety and user experience. These systems are increasingly combined with other in-vehicle technologies, including infotainment and driver assistance systems, to deliver a connected and intelligent driving environment.

China In-Car Wellness Monitoring System Market held a 60% share, generating USD 648.8 million in 2025. Growth in the country is supported by the rapid expansion of electric vehicle adoption and increasing consumer focus on health-oriented mobility solutions. Domestic automakers are incorporating artificial intelligence-driven wellness and safety features into vehicle designs, supported by broader initiatives promoting intelligent and secure transportation systems.

Key companies operating in the Global In-Car Wellness Monitoring System Market include Bosch, Aptiv, Valeo, Denso, Magna, Hyundai Mobis, Gentex, Seeing Machines, Visteon, and Aumovio. Companies in the In-Car Wellness Monitoring System Market are strengthening their competitive position through continuous innovation in sensor technologies, artificial intelligence integration, and real-time data processing capabilities. Manufacturers are focusing on developing highly accurate, non-intrusive monitoring solutions that enhance driver and passenger safety. Strategic partnerships with automotive OEMs are enabling deeper integration of wellness systems into next-generation vehicles. Firms are also investing in advanced radar, camera, and biometric technologies to improve system reliability and performance. Expansion of production capabilities and collaboration with software developers are further supporting scalable deployment. In addition, companies are emphasizing compliance with evolving safety regulations while differentiating through premium in-cabin experience solutions and advanced predictive health monitoring features.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 System

- 2.2.5 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising focus on driver safety and health

- 3.2.1.2 Integration of AI, IoT, and advanced sensors

- 3.2.1.3 Government safety regulations and mandates

- 3.2.1.4 Increasing adoption in luxury and premium vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system cost and integration complexity

- 3.2.2.2 Data privacy and security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into commercial and fleet vehicles

- 3.2.3.2 Growth in autonomous and semi-autonomous vehicles

- 3.2.3.3 Integration with wearable devices and mobile health platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 United States driver monitoring and vehicle safety regulations (NHTSA)

- 3.6.1.2 U.S. data privacy and biometric data laws

- 3.6.1.3 Automotive cybersecurity and software compliance standards

- 3.6.1.4 Canada vehicle safety and data protection regulations (PIPEDA)

- 3.6.2 Europe

- 3.6.2.1 EU General Safety Regulation (driver monitoring mandate)

- 3.6.2.2 GDPR data privacy and biometric compliance

- 3.6.2.3 UNECE cybersecurity and software update regulations (R155, R156)

- 3.6.2.4 National vehicle homologation requirements

- 3.6.3 Asia Pacific

- 3.6.3.1 China data protection laws (PIPL, CSL, DSL)

- 3.6.3.2 China automotive data security regulations

- 3.6.3.3 India automotive safety and driver monitoring guidelines

- 3.6.3.4 Japan intelligent mobility and vehicle safety regulations

- 3.6.3.5 South Korea data protection and connected vehicle rules

- 3.6.4 Latin America

- 3.6.4.1 Brazil data protection law (LGPD) and vehicle safety standards

- 3.6.4.2 Mexico automotive safety and data privacy regulations

- 3.6.4.3 Argentina vehicle safety and data protection frameworks

- 3.6.4.4 Regional automotive certification standards

- 3.6.5 Middle East & Africa

- 3.6.5.1 UAE vehicle safety and smart mobility regulations

- 3.6.5.2 Saudi Arabia automotive safety and data governance

- 3.6.5.3 South Africa vehicle safety and data protection standards

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Trade Data Analysis (Driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Cost breakdown analysis

- 3.12 Impact of AI and Generative AI on the Market

- 3.12.1 AI Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.12.3 Risks Limitations and Regulatory Considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.15.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.2 Cameras

- 5.2.3 Steering wheel and seat sensors

- 5.2.4 Control units and processors

- 5.3 Software

- 5.3.1 AI-based health analytics

- 5.3.2 Driver monitoring algorithms

- 5.3.3 Data integration and alert systems

- 5.4 Services

- 5.4.1 Cloud connectivity and data management

- 5.4.2 Emergency assistance and telehealth integration

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By System, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Driver health monitoring systems

- 7.3 Passenger wellness monitoring systems

- 7.4 In-cabin environment and comfort monitoring systems

- 7.5 Integrated vehicle wellness systems

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Norway

- 9.3.8 Netherlands

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Aptiv

- 10.1.2 Aumovio

- 10.1.3 Bosch

- 10.1.4 Denso

- 10.1.5 Gentex

- 10.1.6 Hyundai Mobis

- 10.1.7 Magna

- 10.1.8 Seeing Machines

- 10.1.9 Valeo

- 10.2 Regional Players

- 10.2.1 Baidu

- 10.2.2 Desay SV Automotive

- 10.2.3 HiRain Technologies

- 10.2.4 Horizon Robotics

- 10.2.5 Huawei Technologies

- 10.2.6 Joyson Electronics

- 10.2.7 NavInfo

- 10.2.8 Neusoft

- 10.2.9 ThunderSoft

- 10.2.10 Visteon

- 10.3 Emerging Players / Disruptors

- 10.3.1 Affectiva

- 10.3.2 Cipia

- 10.3.3 Eyesight Technologies

- 10.3.4 Jungo Connectivity

- 10.3.5 Lightmetrics

- 10.3.6 SenseTime

- 10.3.7 Smart Eye

- 10.3.8 Xperi