PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045656

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045656

Aseptic Bottle Filling Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

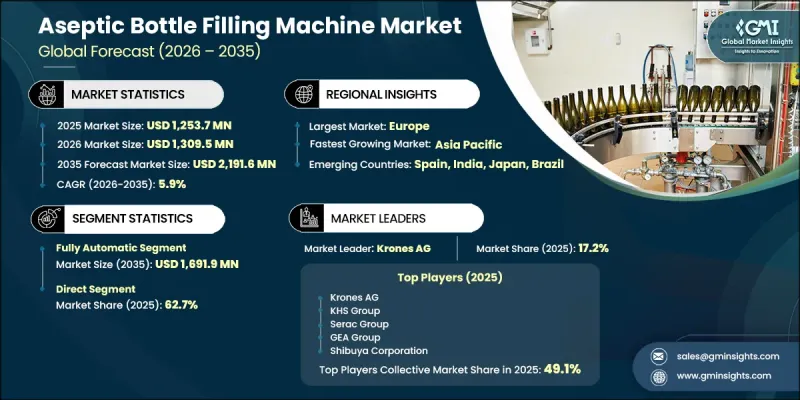

The Global Aseptic Bottle Filling Machine Market was valued at USD 1,253.7 million in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 2,191.6 million by 2035.

Rising demand for biologics, vaccines, and sterile pharmaceutical products continues to accelerate the adoption of advanced aseptic filling technologies across the healthcare sector. Manufacturers are significantly increasing investments in modern filling systems and contamination control technologies to ensure safe and sterile product handling throughout the production cycle. The evolving food and beverage sector is also contributing to market growth as consumers increasingly prefer preservative-free products with extended shelf life and high product integrity. Aseptic filling systems help manufacturers maintain product quality while meeting strict hygiene and packaging standards. Regulatory authorities have strengthened sterilization and containment requirements, encouraging companies to replace outdated machinery with advanced, compliant systems. Growing emphasis on operational efficiency, automation, product safety, and regulatory adherence continues to create favorable opportunities for the aseptic bottle filling machine industry worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1,253.7 Million |

| Forecast Value | $2,191.6 Million |

| CAGR | 5.9% |

The fully automatic segment generated USD 959.2 million in 2025 and is expected to reach USD 1,691.9 million by 2035. Fully automated aseptic bottle filling machines continue to dominate the industry due to their ability to maintain high levels of sterility and process precision. These systems significantly reduce direct human interaction during the filling process, minimizing contamination risks and improving production reliability. Automated technologies also deliver greater operational consistency by ensuring uniform filling speed, accurate sealing, and stable product handling throughout production cycles. Such consistency is essential for manufacturers aiming to comply with strict international quality and safety standards. Increasing adoption of automation across pharmaceutical and food processing facilities is further strengthening demand for fully automatic aseptic filling equipment.

The direct sales segment accounted for 62.7% share in 2025. Direct purchasing channels remain the preferred sales approach because aseptic filling systems involve highly specialized engineering and technical integration requirements. Customers typically require extensive consultation and customized system configuration before investing in advanced filling equipment. Manufacturers often work directly with end users to ensure machinery specifications align with operational requirements, facility structures, and production capacities. Customized system design also plays an important role in large-scale production environments where equipment must accommodate specific processing characteristics and packaging requirements. The technical complexity associated with aseptic machinery limits the role of third-party distributors, as buyers generally prefer direct engagement with original equipment manufacturers for better technical guidance and long-term support services.

United States Aseptic Bottle Filling Machine Market accounted for 81.6% share in 2025. Strong market growth across the country is primarily supported by rising consumption of packaged nutritional products, dairy-based beverages, and ready-to-consume products requiring sterile packaging solutions. Food and beverage manufacturers are increasingly prioritizing contamination-free production environments to comply with strict food safety and validation standards established by regulatory authorities. Additionally, the rapid integration of automation technologies and Industry 4.0 solutions is encouraging investments in advanced aseptic filling equipment capable of improving traceability, operational efficiency, and regulatory compliance. Replacement of aging packaging infrastructure across production facilities in the United States and Canada is also contributing to continued market expansion throughout the region.

Major companies operating in the Global Aseptic Bottle Filling Machine Market include Aseptic Systems Co., Ltd., Cozzoli Machine Company, Dara Pharma, GEA Group, Groninger Holding GmbH & Co. KG, KHS Group, Krones AG, Newamstar Packaging Machinery, NJM Packaging, Plumat, Romaco Group, Serac Group, Shibuya Corporation, SMI Group, Syntegon, Tech-Long Packaging Machinery, Tetra Pak, Trepko, Watson-Marlow / Flexicon, Weiler Engineering, Inc., and Zhangjiagang King Machine. Companies operating in the aseptic bottle filling machine industry are adopting several strategic initiatives to strengthen their market presence and improve competitive positioning. Leading manufacturers are investing heavily in automation technologies, robotic integration, and smart monitoring systems to enhance production efficiency and reduce contamination risks. Product innovation remains a major focus area, with companies developing advanced filling systems capable of supporting higher throughput and improved sterilization performance. Strategic partnerships, mergers, and regional expansion initiatives are also helping market participants increase customer reach and strengthen distribution capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.9 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By Technology

- 2.2.3 By Mode Of Operation

- 2.2.4 By Output Capacity

- 2.2.5 By Integration Type

- 2.2.6 By Sterilization Technology

- 2.2.7 By Application

- 2.2.8 By End Use Industry

- 2.2.9 By Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging demand for increasing demand for sterile contamination free packaging

- 3.2.1.2 Rising consumption of shelf-stable and preservative-free products

- 3.2.1.3 Stricter regulatory requirements for hygiene, traceability, and process validation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Stringent regulatory requirements and compliance standards

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of dairy alternatives, functional beverages, and nutraceuticals

- 3.2.3.2 Adoption of automation, digital monitoring, and industry 4.0 solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.5 Major market trends and disruptions

- 3.6 Technology/innovation landscape

- 3.7 Pricing Analysis (driven by primary research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.8 Future market trends

- 3.9 Trade data analysis (driven by paid database) (HS code- 8422.30)

- 3.9.1 Import/export volume & value trends (driven by primary research)

- 3.9.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 Gen-AI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Aseptic Bottle Filling Capacity by Region & Key Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035 (USD Million, Thousand Units)

- 5.1 Key trends

- 5.2 Rotary aseptic filling systems

- 5.3 Linear aseptic filling systems

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Mode of Operation, 2022 - 2035 (USD Million, Thousand Units)

- 6.1 Key trends

- 6.2 Fully automatic

- 6.3 Semi-automatic

Chapter 7 Market Estimates & Forecast, By Output Capacity, 2022 - 2035 (USD Million, Thousand Units)

- 7.1 Key trends

- 7.2 Up to 10,000 Bottles/Hr

- 7.3 10,000 to 25,000 Bottles/Hr

- 7.4 25,000 to 50,000 Bottles/Hr

- 7.5 Above 50,000 Bottles/Hr

Chapter 8 Market Estimates & Forecast, By Integration Type, 2022 - 2035 (USD Million, Thousand Units)

- 8.1 Key trends

- 8.2 Standalone filling systems

- 8.3 Integrated monobloc systems

Chapter 9 Market Estimates & Forecast, By Sterilization Technology, 2022 - 2035 (USD Million, Thousand Units)

- 9.1 Key trends

- 9.2 Chemical sterilization

- 9.3 Energy-based sterilization

- 9.4 Combination/multi-method systems

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Million, Thousand Units)

- 10.1 Key trends

- 10.2 Plastic bottle

- 10.2.1 PET bottle filling

- 10.2.2 HDPE bottle filling

- 10.2.3 PP bottle filling

- 10.3 Glass bottle

- 10.4 Others (metallic, multilayer & specialty bottle)

Chapter 11 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Million, Thousand Units)

- 11.1 Key trends

- 11.2 Pharmaceutical

- 11.3 Cosmetic industries

- 11.4 Food and beverages

- 11.5 Biotechnology

- 11.6 Others (chemical etc.)

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Million, Thousand Units)

- 12.1 Key trends

- 12.2 Direct sales

- 12.3 Indirect sales

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Million, Thousand Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Spain

- 13.3.5 Italy

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 Japan

- 13.4.3 India

- 13.4.4 Australia

- 13.4.5 South Korea

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global Companies

- 14.1.1 GEA Group

- 14.1.2 KHS Group

- 14.1.3 Krones AG

- 14.1.4 Serac Group

- 14.1.5 Shibuya Corporation

- 14.1.6 Syntegon

- 14.1.7 Tetra Pak

- 14.2 Regional Companies

- 14.2.1 Aseptic Systems Co., Ltd.

- 14.2.2 Dara Pharma

- 14.2.3 Groninger Holding GmbH & Co. KG

- 14.2.4 Plumat

- 14.2.5 Romaco Group

- 14.2.6 SMI Group

- 14.2.7 Watson-Marlow / Flexicon

- 14.3 Emerging Companies

- 14.3.1 Cozzoli Machine Company

- 14.3.2 NJM Packaging

- 14.3.3 Newamstar Packaging Machinery

- 14.3.4 Tech-Long Packaging Machinery

- 14.3.5 Trepko

- 14.3.6 Weiler Engineering, Inc.

- 14.3.7 Zhangjiagang King Machine