PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045662

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045662

North America Vertical Farming Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

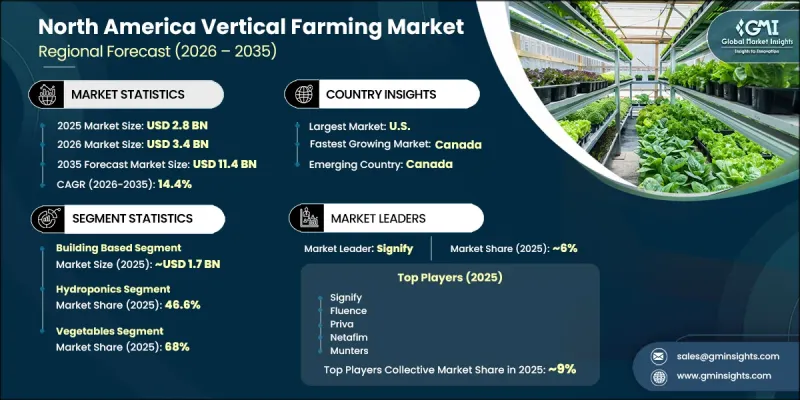

North America Vertical Farming Market was valued at USD 2.8 billion in 2025 and is estimated to grow at a CAGR of 14.4% to reach USD 11.4 billion by 2035.

Rapid urbanization across North America is creating increasing pressure on available agricultural land, encouraging the adoption of innovative farming methods capable of delivering higher crop yields within limited spaces. Vertical farming has emerged as a transformative agricultural approach that utilizes advanced cultivation technologies to improve productivity, resource efficiency, and food quality. The growing preference for fresh, clean, and chemical-free produce among consumers is also accelerating market growth across the region. Controlled indoor farming environments reduce dependency on synthetic chemicals while ensuring consistent crop quality and higher production efficiency throughout the year. In addition, vertical farming systems provide reliable year-round cultivation regardless of seasonal climate changes, helping producers maintain stable food supply chains. Locating production facilities closer to urban populations further improves product freshness, shelf life, and nutritional value, strengthening the long-term growth outlook for the North America vertical farming industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.8 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 14.4% |

The building-based segment generated USD 1.7 billion in 2025 and is anticipated to grow at a CAGR of 14.8% from 2026 to 2035. Building-based vertical farming operations continue to play a leading role in the North America vertical farming market due to their ability to maximize controlled-environment agriculture within urban infrastructure settings. These facilities are commonly developed within purpose-built structures or converted industrial spaces that support precise management of environmental conditions, including humidity, lighting, temperature, and nutrient delivery systems. Such controlled cultivation environments enable uninterrupted crop production throughout the year while maintaining consistent quality and operational efficiency. The growing focus on urban food production and supply chain optimization is further supporting demand for building-based vertical farming solutions across the region.

The hydroponics segment held a 46.6% share in 2025. Hydroponic systems are gaining widespread adoption due to their ability to enhance crop growth while reducing dependency on soil-based farming methods. By utilizing nutrient-rich water solutions, these systems help minimize contamination risks and improve cultivation efficiency. Hydroponics also significantly lowers water consumption compared to conventional agricultural practices, making it a highly sustainable farming solution. The scalability of hydroponic systems and their compatibility with automation technologies continue to attract investments from large commercial farming operators and emerging urban agriculture businesses throughout North America.

United States Vertical Farming Market accounted for USD 1.9 billion in 2025. The United States remains one of the most technologically advanced and innovation-driven vertical farming markets globally, supported by strong investment activity and rapid adoption of indoor agriculture technologies. Favorable support for urban agriculture initiatives and the availability of infrastructure suitable for vertical farming development are contributing to increasing market penetration across the country. In addition, widespread integration of automation technologies, robotics, and renewable energy systems is helping operators improve production efficiency while addressing rising labor and operational costs. The combination of technological advancement, infrastructure availability, and growing consumer demand for locally produced fresh food continues to position the United States as a leading market for vertical farming innovation and commercial expansion.

Major companies operating in the North America Vertical Farming Market include global participants such as Fluence, Signify (Philips), Priva, Netafim, Munters, OSRAM, and Seoul Semiconductor. Regional companies participating in the market include Freight Farms, Desert Aire, Sollum Technologies, Ridder, DryGair, Lumileds, Heliospectra, and Valoya. Companies operating in the North America vertical farming market are implementing several strategic initiatives to strengthen their market position and expand commercial presence. Leading players are heavily investing in automation technologies, artificial intelligence, and data-driven farming systems to improve crop productivity and operational efficiency. Product innovation focused on energy-efficient lighting, climate control systems, and water-saving cultivation technologies remains a major priority across the industry. Companies are also forming strategic partnerships with technology providers, food retailers, and urban agriculture developers to expand distribution networks and strengthen market reach. In addition, market participants are increasing investments in research and development activities to improve crop yield consistency and reduce operating costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Structure

- 2.2.3 Process

- 2.2.4 Component

- 2.2.5 Crop Type

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urban population growth

- 3.2.1.2 Demand for sustainable food

- 3.2.1.3 Technology advancements

- 3.2.2 Pitfalls & challenges

- 3.2.2.1 High energy costs

- 3.2.2.2 Operational complexity

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of controlled-environment agriculture

- 3.2.3.2 Innovation in LED & automation systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.5.3 Automation & robotics integration

- 3.5.4 Sensor & IoT technologies

- 3.6 Price trends, 2025

- 3.6.1 Historical Price Trend Analysis

- 3.6.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6.3 Price Comparison: Vertical Farm vs. Traditional Agriculture

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Food safety standards & compliance

- 3.7.3 Regional regulatory frameworks

- 3.7.4 Certification standards

- 3.8 Trade Data Analysis (Driven by paid database) (HS code - 8436.80.90)

- 3.8.1 Import/export volume & value trends (driven by primary research)

- 3.8.2 Key trade corridors & tariff impact (driven by primary research)

- 3.9 Impact of AI & Generative AI on the Market

- 3.9.1 AI-Driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

- 3.12 Supply chain analysis

- 3.12.1 Equipment supply chain

- 3.12.2 Seed & genetics supply

- 3.12.3 Distribution & logistics networks

- 3.12.4 Supply chain vulnerabilities & resilience

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer (driven by primary research)

- 3.13.2 Capacity utilization rates & expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Country

- 4.2.1.1 U.S.

- 4.2.1.2 Canada

- 4.2.1 By Country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Structure, 2022 - 2035, (USD Billion)

- 5.1 Key trends

- 5.2 Shipping-container based

- 5.3 Building based

Chapter 6 Market Estimates & Forecast, By Process, 2022 - 2035, (USD Billion)

- 6.1 Key trends

- 6.2 Hydroponics

- 6.3 Aeroponics

- 6.4 Aquaponics

Chapter 7 Market Estimates & Forecast, By Component, 2022 - 2035, (USD Billion)

- 7.1 Key trends

- 7.2 Hardware

- 7.2.1 Lighting systems

- 7.2.2 Hydroponic components

- 7.2.3 Climate control systems

- 7.2.4 Sensors & monitoring equipment

- 7.2.5 Building materials & structural components

- 7.3 Software

- 7.4 Services

Chapter 8 Market Estimates & Forecast, By Crop Type, 2022 - 2035, (USD Billion)

- 8.1 Key trends

- 8.2 Fruits

- 8.3 Vegetables

Chapter 9 Market Estimates & Forecast, By Country, 2022 - 2035, (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Fluence

- 10.1.2 Signify (Philips)

- 10.1.3 Priva

- 10.1.4 Netafim

- 10.1.5 Munters

- 10.1.6 OSRAM

- 10.1.7 Seoul Semiconductor

- 10.2 Regional players

- 10.2.1 Freight Farms

- 10.2.2 Desert Aire

- 10.2.3 Sollum Technologies

- 10.2.4 Ridder

- 10.2.5 DryGair

- 10.2.6 Lumileds

- 10.2.7 Heliospectra

- 10.2.8 Valoya

- 10.3 Emerging players

- 10.3.1 AEssenseGrows

- 10.3.2 Gardin Agritech

- 10.3.3 IGS

- 10.3.4 Nova Aeroponics

- 10.3.5 Grow Pod Solutions

- 10.3.6 Autogrow