PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045676

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045676

U.S. Industrial Energy Storage System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

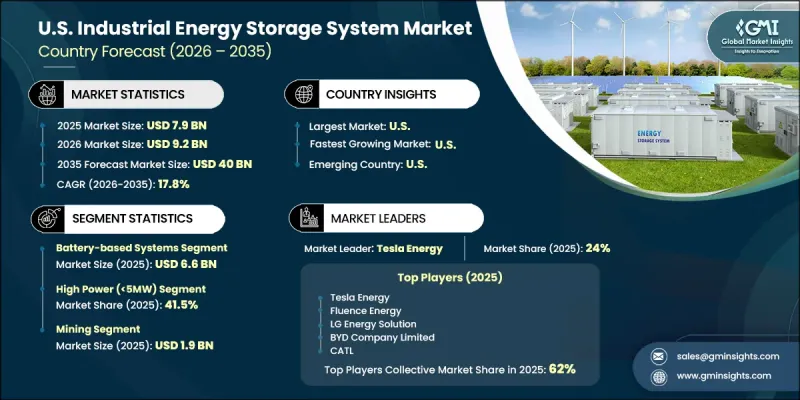

U.S. Industrial Energy Storage System Market was valued at USD 7.9 billion in 2025 and is estimated to grow at a CAGR of 17.8% to reach USD 40 billion by 2035.

The industrial energy storage system industry in the United States is advancing rapidly as energy optimization, cost control, and operational resilience become critical priorities for industrial operators. Energy storage solutions are increasingly viewed as transformative technologies that enable businesses to better manage electricity usage, enhance grid stability, and improve sustainability outcomes. Widespread adoption across industries reflects the growing need for reliable and efficient energy infrastructure. These systems are widely implemented to support load balancing, ensure continuity of operations, and facilitate the integration of renewable energy sources into industrial power systems. The market continues to lead globally, supported by strong technological advancements, increasing awareness of energy efficiency, and favorable regulatory frameworks. Continuous innovation, combined with growing investments in infrastructure modernization, is further strengthening the adoption of industrial energy storage systems across the country.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.9 Billion |

| Forecast Value | $40 Billion |

| CAGR | 17.8% |

Technological advancements in the industrial energy storage system market have significantly improved system performance and operational flexibility. Modern solutions are being designed with enhanced reliability, scalability, and efficiency, allowing industrial users to adapt to evolving energy demands. Ongoing research and development efforts are driving improvements in system capabilities, resulting in more advanced and cost-effective energy storage technologies. Manufacturers are increasingly focusing on refining system architecture and optimizing performance to meet the diverse needs of industrial applications.

The battery-based systems segment held an 84% share in 2025 with a value of USD 6.6 billion. This segment leads due to its adaptability, efficiency, and cost-effectiveness, making it suitable for a wide range of industrial applications. Continuous reductions in battery costs, along with advancements in energy density and lifecycle performance, are supporting broader adoption. The segment is also benefiting from expanded application scope, improved financial accessibility, and growing support through incentive structures.

The high power (5MW) systems segment held a 41.5% share in 2025. These systems are designed to meet the substantial energy demands of large-scale industrial operations, enabling significant cost optimization and improved energy efficiency. The growth of this segment is supported by economies of scale, which enhance cost advantages, and the increasing deployment of large-capacity storage solutions that support advanced energy management strategies.

The mining segment held a 24.3% share in 2025. This segment benefits from the ability of energy storage systems to reduce reliance on conventional fuel sources, improve energy efficiency, and support sustainability initiatives. Increased focus on cost savings, operational efficiency, and environmental performance continues to drive adoption within this segment.

Key players in the U.S. Industrial Energy Storage System Market include Fluence Energy, Inc., Tesla Energy, LG Energy Solution, BYD Company Limited, CATL, Samsung SDI Co., Ltd., Wartsila Energy Storage, Cummins Inc., Generac Industrial Energy, Stryten Energy, Stem, Inc., Atlas Copco AB, Form Energy, Inc., ESS Inc. (ESS Tech), Energy Vault, Inc., and Enphase Energy. Companies operating in the U.S. Industrial Energy Storage System Market are implementing a range of strategies to strengthen their competitive position. Organizations are investing heavily in research and development to enhance system efficiency, durability, and scalability. Strategic collaborations and partnerships are being pursued to expand technological capabilities and accelerate market penetration. Firms are also focusing on expanding their product portfolios to address diverse industrial requirements while improving customization options. Digital integration, including advanced monitoring and control systems, is being leveraged to deliver enhanced performance and user experience.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Storage systems

- 2.2.2 Power range

- 2.2.3 Application

- 2.2.4 End use industry

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising electricity costs and demand charge management

- 3.2.1.2 Grid modernization and renewable energy integration mandates

- 3.2.1.3 Decarbonization commitments and ESG reporting requirements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront capital costs

- 3.2.2.2 Regulatory uncertainty and interconnection challenges

- 3.2.3 Opportunities

- 3.2.3.1 Integration of AI-powered energy management and predictive analytics

- 3.2.3.2 Behind-the-meter microgrid development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Paid data source) (HS code - 8507.60)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Capacity by Region & Key Producer (Modern vs. Traditional Trade) (Driven by Primary Research)

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Storage system, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Mechanical systems

- 5.2.1 Compressed air energy storage

- 5.2.2 Pumped hydro power

- 5.3 Thermal systems

- 5.4 Battery-based systems

Chapter 6 Market Estimates and Forecast, By Power Range, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low power (>200kW)

- 6.3 Medium power (200kW-5MW)

- 6.4 High power (<5 MW)

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Energy arbitrage & time-shifting

- 7.3 Peak shaving & load leveling

- 7.4 Renewable integration & firming

- 7.5 Grid stability & voltage support

- 7.6 Transmission & distribution deferral

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Mining

- 8.3 Oil & gas

- 8.4 Food & beverage

- 8.5 Pharmaceutical

- 8.6 Automotive

- 8.7 Others (data center etc.)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Company Profiles

- 10.1 Top Global Players

- 10.1.1 Tesla Energy

- 10.1.2 Fluence Energy, Inc.

- 10.1.3 LG Energy Solution

- 10.1.4 BYD Company Limited

- 10.1.5 CATL

- 10.1.6 Samsung SDI Co., Ltd.

- 10.1.7 Wartsila Energy Storage

- 10.2 Regional Champions

- 10.2.1 Cummins Inc.

- 10.2.2 Generac Industrial Energy

- 10.2.3 Stryten Energy

- 10.2.4 Stem, Inc.

- 10.2.5 Atlas Copco AB

- 10.3 Emerging & Specialized Players

- 10.3.1 Form Energy, Inc.

- 10.3.2 ESS Inc. (ESS Tech)

- 10.3.3 Energy Vault, Inc.

- 10.3.4 Enphase Energy