PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045681

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045681

Asia Pacific Conveyor Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

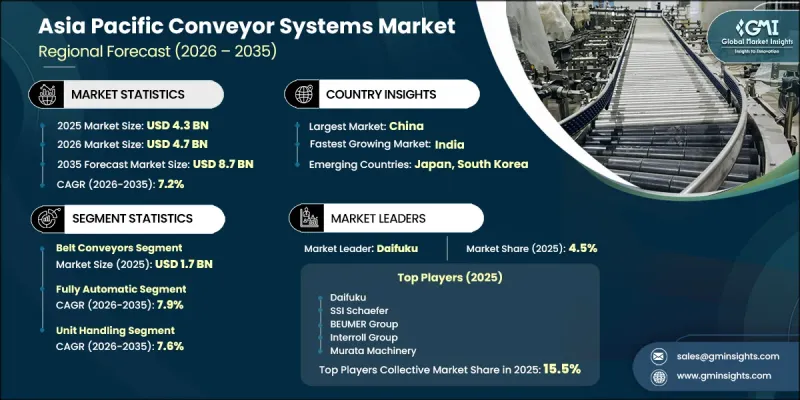

Asia Pacific Conveyor Systems Market was valued at USD 4.3 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 8.7 billion by 2035.

Growth across the Asia Pacific conveyor systems industry continues to accelerate as manufacturers and industrial operators increasingly focus on automation to improve productivity and minimize operational costs. Rising technological integration across production facilities and distribution centers has significantly increased the deployment of conveyor technologies throughout the region. Expanding online retail activities have also created a strong demand for advanced material handling infrastructure capable of supporting high-volume goods movement. In addition, rapid investment in modern warehousing facilities has accelerated the adoption of conveyor systems across logistics networks. The integration of smart technologies, including IoT and AI-enabled systems, continues to reshape the industry by enabling predictive maintenance, real-time equipment tracking, and improved operational performance. Sustainability trends are further encouraging the development of energy-efficient conveyor solutions. Strong industrial expansion in emerging economies, combined with the fast-growing retail and manufacturing sectors, is expected to create substantial growth opportunities for the Asia Pacific conveyor systems market over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.3 Billion |

| Forecast Value | $8.7 Billion |

| CAGR | 7.2% |

The belt conveyors segment accounted for USD 1.7 billion in 2025. The segment is anticipated to expand at a CAGR of 7.7% throughout the forecast timeline. Demand for belt conveyor systems continues to rise due to their extensive application across manufacturing, logistics, and processing industries. Their ability to efficiently transport both bulk materials and packaged products has made them a preferred solution across multiple industrial operations. Increasing emphasis on automated material handling and continuous advancements in conveyor technologies are further supporting segment growth across regional markets.

The fully automatic segment held a 48% share and is forecast to witness a CAGR of 7.9% between 2026 and 2035. Fully automated conveyor systems are gaining strong traction because they deliver greater precision, higher efficiency, and reduced dependency on manual labor. The integration of robotics, IoT-enabled monitoring systems, and AI-driven automation features is significantly increasing adoption rates across industrial facilities. In addition, the growing shift toward smart manufacturing and Industry 4.0 frameworks is expected to further strengthen demand for fully automatic conveyor solutions throughout the Asia-Pacific region.

China Conveyor Systems Industry held a 34% share, generating USD 1.5 billion in 2025. Market growth in China is driven by rapid industrial development and continuous modernization of manufacturing infrastructure. Key provinces contributing to market expansion include Guangdong, Jiangsu, and Zhejiang, where large-scale industrial production and advanced manufacturing activities continue to expand. The increasing adoption of conveyor systems across industrial facilities in these provinces is supporting regional market growth and accelerating investments in advanced automation technologies.

Key companies operating in the Asia Pacific conveyor systems market include Bastian Solutions, BEUMER Group, Daifuku, Dorner Manufacturing, Interroll Group, Murata Machinery, and SSI Schaefer. Regional participants active in the market include Australian Conveyor Engineering, Doosan Logistics Solutions, Fenner Conveyors, Godrej-Korber, IHI Logistics & Machinery, Shanghai YiFan, and Shanxi Dongjie. Emerging and niche companies participating in the Asia Pacific conveyor systems market include Delta Electronics, Elecon Engineering, Kawasaki Heavy Industries, MF India (Material First), Ryson International, Siemens Logistics, and Toshiba Infrastructure. Companies participating in the Asia Pacific conveyor systems market are focusing on several strategic initiatives to strengthen their market position and expand regional presence. Major players are increasing investments in automation technologies, smart conveyor solutions, and AI-enabled monitoring systems to improve operational efficiency and product performance. Many companies are also prioritizing research and development activities to introduce energy-efficient and sustainable conveyor technologies that align with evolving industrial requirements. Strategic partnerships, mergers, and collaborations with logistics providers and manufacturing companies are becoming increasingly common to enhance distribution capabilities and customer reach. In addition, manufacturers are expanding production facilities across emerging Asia Pacific economies to support rising demand and improve supply chain responsiveness.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by country

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 System Type

- 2.2.3 Load Type

- 2.2.4 Operation Mode

- 2.2.5 System Configuration

- 2.2.6 End Use Industry

- 2.2.7 Distribution Channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Manufacturers

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 E-Commerce Boom & Warehouse Automation Expansion

- 3.2.1.2 Manufacturing FDI & China+1 Strategy (India, Vietnam, Indonesia, Thailand)

- 3.2.1.3 Industry 4.0 / Smart Factory Adoption (IoT, AI-integrated conveyors)

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial Capital Expenditure & Long Payback Periods

- 3.2.2.2 Supply Chain Disruptions & Component Shortages (semiconductors, motors, sensors)

- 3.2.2.3 Skilled Labor Shortage for System Integration & Maintenance

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing analysis, 2025 (driven by primary research)

- 3.4.1 Historical price trend analysis

- 3.4.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.4.3 Price variation by product type & technology generation

- 3.4.4 Consumer price sensitivity analysis

- 3.5 Regulatory landscape

- 3.5.1 China GB Standards & Compliance

- 3.5.2 ASEAN Harmonized Standards & Fragmentation

- 3.5.3 India BIS Standards & Quality Mark Requirements

- 3.5.4 Japan/Korea Safety Standards (JIS, KS)

- 3.5.5 Australia/New Zealand AS/NZS Standards

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technological and innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Future market trends

- 3.10 Trade data analysis (driven by paid database) (HS Code: 8428)

- 3.10.1 Intra-APAC Import/Export Volume & Value Trends

- 3.10.2 China-ASEAN Trade Corridors & RCEP Impact

- 3.10.3 India-ASEAN Trade Dynamics

- 3.11 Impact of AI & generative ai on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By System Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Belt conveyors

- 5.3 Roller conveyors

- 5.4 Pallet conveyors

- 5.5 Overhead conveyors

- 5.6 Bucket conveyors

- 5.7 Others (floor conveyors, chain conveyors etc.)

Chapter 6 Market Estimates & Forecast, By Load Type, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Unit handling

- 6.3 Bulk handling

Chapter 7 Market Estimates & Forecast, By Operation Mode, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Semi-automatic

- 7.4 Fully automatic

Chapter 8 Market Estimates & Forecast, By System Configuration, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Fixed/linear systems

- 8.3 Modular/flexible systems

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Mining & quarrying

- 9.4 Pharmaceuticals

- 9.5 Retail & E-commerce

- 9.6 Food & Beverages

- 9.7 Others (airport etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 11.1 Key trends

- 11.2 China

- 11.3 India

- 11.4 Japan

- 11.5 South Korea

- 11.6 Australia

- 11.7 Indonesia

- 11.8 Malaysia

- 11.9 Rest of Asia Pacific

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Bastian Solutions (Toyota AL)

- 12.1.2 BEUMER Group

- 12.1.3 Daifuku

- 12.1.4 Dorner Manufacturing

- 12.1.5 Interroll Group

- 12.1.6 Murata Machinery

- 12.1.7 SSI Schaefer

- 12.2 Regional Players

- 12.2.1 Australian Conveyor Engineering

- 12.2.2 Doosan Logistics Solutions

- 12.2.3 Fenner Conveyors

- 12.2.4 Godrej-Korber

- 12.2.5 IHI Logistics & Machinery

- 12.2.6 Shanghai YiFan

- 12.2.7 Shanxi Dongjie

- 12.3 Emerging/Niche Specialists

- 12.3.1 Delta Electronics

- 12.3.2 Elecon Engineering

- 12.3.3 Kawasaki Heavy Industries

- 12.3.4 MF India (Material First)

- 12.3.5 Ryson International

- 12.3.6 Siemens Logistics

- 12.3.7 Toshiba Infrastructure