PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2059968

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2059968

Conveyor System Market by Industry (Retail & Distribution, Food & Beverage, Automotive, Electronic, Mining, & Airport), Type (Belt, Roller, Overhead, Floor, Pallet, Crescent, Cable, Bucket), Component, Operation, & Region - Global Forecast to 2033

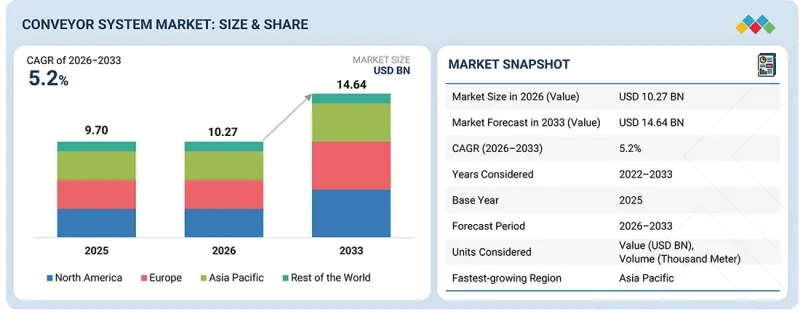

The conveyor system market size is projected to grow from USD 10.27 billion in 2026 to USD 14.64 billion by 2033, at a CAGR of 5.2%. The conveyor system market demand is being shaped by the shift toward continuous, automated operations, in which material flow is tightly integrated into production and distribution processes rather than handled in batches. In automotive manufacturing, conveyors support flexible assembly-line architectures and multi-model production, enabling higher output with reduced manual intervention.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | Industry, Type, Component, Operation, & Region |

| Regions covered | Asia Pacific, Europe, North America, and Rest of the World |

In warehousing and ecommerce logistics, conveyor-based sortation and cross-docking systems have become essential to manage rising parcel volumes, tighter delivery timelines, and ongoing labor constraints. The food, beverage, and pharmaceutical industries rely on hygienic, washdown-capable conveyors to meet safety, traceability, and regulatory requirements while scaling production. Industrial manufacturing, mining, and airports are increasingly adopting sensor-integrated and software-enabled conveyor systems to reduce downtime, optimize energy use, and improve operational reliability. Across sectors, companies are also moving toward modular conveyor layouts that can be expanded or reconfigured as demand patterns change, supported by greater use of automation, condition monitoring, and intelligent control systems that improve flow efficiency and system responsiveness.

Pallet conveyor segment is expected to witness high growth opportunities during the forecast period.

Pallet conveyors are expected to see the fastest growth in the retail and distribution conveyor system market, driven by rising palletized throughput in large-scale e-commerce and omnichannel fulfillment networks. Modern distribution centers handling high SKU complexity now process thousands of pallet moves per day, with large facilities often exceeding 200,000-500,000 square feet, in which pallet-based flows are a core part of inbound replenishment and outbound dispatch cycles. This scale of movement is making manual handling inefficient, driving the adoption of automated pallet conveying to ensure continuous, controlled flow across receiving, storage, and shipping zones. The growth is also supported by the increasing integration of pallet conveyors with automated storage and retrieval systems and warehouse control platforms, with automation penetration in large distribution centers at approximately 50% in developed markets. This integration is critical for synchronizing pallet movement with high-density storage systems and high-speed order-fulfillment operations, particularly in e-commerce-driven facilities, where inventory turnover rates are significantly higher than in traditional retail distribution models. Investment momentum in warehouse automation continues to drive adoption, with large logistics operators expanding high-throughput distribution infrastructure to manage rising parcel and pallet volumes while meeting compressed delivery timelines. For instance, in February 2026, Dematic announced advanced AS RS solutions targeting high-volume ecommerce and multichannel distribution networks, reflecting the continued expansion of fully automated pallet handling systems in large-scale retail and logistics facilities.

Meat and poultry industry will see the fastest growth in the food subindustry.

Meat and poultry are expected to grow at the fastest rate in the food and beverage conveyor system market during the forecast period, supported by higher demand for hygienic, automated, and high-speed handling across processing and packaging lines. Producers are shifting toward conveyor systems that can handle raw meat, poultry cuts, trays, cartons, and packaged products with improved sanitation control and reduced manual contact. This segment is also gaining importance as processors need to meet strict food safety standards, reduce the risk of contamination, and maintain consistent product flow across the washing, cutting, inspection, freezing, and packaging areas. For instance, in March 2026, Key Technology introduced its SmartConveyor System for poultry processing applications, designed to improve automated product handling, inspection flow, and packaging line efficiency in meat and poultry facilities.

Meat and poultry conveyor systems are becoming a key part of hygienic food-processing layouts, where product safety, line efficiency, and controlled handling remain central requirements.

Belt-type conveyor systems will account for the largest market share in the airport industry.

Belt conveyor systems are expected to hold the largest share in the airport conveyor system market due to their role in handling continuous baggage flow across high-volume airport operations. Global passenger traffic has recovered to pre-pandemic levels, exceeding 4 billion passengers annually, increasing pressure on airport baggage systems to process higher volumes within fixed turnaround windows. Large hub airports now handle peak loads exceeding 10,000 bags per hour, making continuous belt-based transport essential for stable, uninterrupted movement through check-in, screening, transfer, and arrival zones. Airport baggage handling systems are increasingly designed as fully integrated automation networks, in which belt conveyors serve as the primary transport layer linking screening equipment, RFID tracking, and automated sortation systems. This is particularly important in transfer-heavy hubs, where connecting baggage can account for around 40% of the total baggage flow, requiring tightly synchronized movement to avoid delays. Ongoing airport expansion across Asia Pacific, Europe, and the Middle East is reinforcing adoption, with new terminals and upgrades moving toward fully automated baggage handling rather than semi-manual systems. Projects such as Heathrow expansion and Centralny Port Komunikacyjny are designed around high-capacity conveyor-based systems to support long-term traffic growth and operational efficiency.

Europe is expected to account for a significant share of the conveyor system market during the forecast period.

Europe is expected to hold the largest share of the conveyor system market, supported by its established industrial base in automotive, food and beverage, airports, retail, and advanced manufacturing. The region has one of the highest automation penetration levels globally, with a large share of new warehouses and distribution centers in Western Europe already operating with automated material handling systems, including conveyor-based sortation and intra-facility transport. Germany, France, the UK, Italy, and the Netherlands continue to drive demand due to dense manufacturing networks and highly developed logistics infrastructure, particularly around automotive production clusters and cross-border fulfillment hubs. A major structural driver is the cost and compliance environment, in which higher labor costs and strict workplace safety standards are pushing companies to reduce manual handling and adopt automated material-handling solutions. This has made conveyors a preferred option for improving productivity, reducing operational risk, and maintaining consistent throughput across factories, warehouses, and airports. The region is also seeing ongoing investment in upgrading existing infrastructure rather than building new capacity, particularly in logistics and airport operations, where automation upgrades focus on improving speed, reliability, and space efficiency. For instance, in May 2026, Interroll Holding AG acquired Royal Apollo Group to strengthen its portfolio of vertical conveying and logistics systems, reflecting ongoing consolidation and capability expansion within the European automation ecosystem. Overall, Europe's leadership is driven by its high automation penetration, strong regulatory environment, and steady modernization of existing industrial and logistics infrastructure.

In-depth interviews were conducted with CXOs, marketing directors, other innovation and technology managers, and executives from various key organizations operating in the conveyor system market. The break-up of the primaries is as follows:

- By Company Type: OEMs - 25%, Tier 1 - 70%, and Tier 2 & 3 - 5%,

- By Designation: CXO - 25%, Managers - 60%, and Executives - 15%

- By Region: North America - 15%, Europe - 50%, Asia Pacific - 15%, and RoW - 20%

The conveyor system market comprises major manufacturers such as Daifuku Co., Ltd. (Japan), Continental AG (Germany), Dematic (US), Vanderlande Industries B.V. (Netherlands), and Interroll Holding AG (Switzerland).

Research Coverage:

The study covers the conveyor system market across various segments. It aims at estimating the market size and future growth potential of this market across different segments. The study also includes an in-depth competitive analysis of key market players, including their company profiles, key observations on product and business offerings, recent developments, and acquisitions.

This research report categorizes the conveyor system market by industry (retail & distribution, food & beverage, automotive, electronic, mining, & airport), type (belt, roller, overhead, floor, pallet, crescent, cable, bucket, & others) component, operation (automated, semi-automatic & manual), and region (North America, Europe, Asia Pacific, and Rest of the World)

The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the conveyor system market. A detailed analysis of the key industry players provides insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, product & service launches, mergers and acquisitions, and recent developments associated with the conveyor system market. Competitive analysis of SMEs/startups in the conveyor system market ecosystem is covered in this report.

Key reasons to buy this report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall conveyor system market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

- The report also helps stakeholders understand the current and future pricing trends of the conveyor system market.

The report provides insights into the following pointers:

- Analysis of key drivers (growing adoption of automation, extensive use of conveyor systems for mass production, surge in mining of rare earth metals, high demand for conveyor systems from e-commerce industry), restraints (high installation and maintenance costs, non-feasibility of automation in niche warehousing, automotive, and electronics applications), opportunities (integration of lean logistics principles, innovations in conveyor systems, rapid deployment of green conveyors to reduce emissions), and challenges (significant presence of local players in emerging markets, rising safety concerns due to system failures) influencing the growth of the conveyor system market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the conveyor system market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the conveyor system market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the conveyor system market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Daifuku Co., Ltd. (Japan), Continental AG (Germany), Dematic (US), Vanderlande Industries B.V. (Netherlands), and Interroll Holding AG (Switzerland), among others, in the conveyor system market.

- Strategies: The report also helps stakeholders understand the pulse of the conveyor system market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING CONVEYOR SYSTEM MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CONVEYOR SYSTEM MARKET

- 3.2 CONVEYOR SYSTEM MARKET, BY TYPE

- 3.3 CONVEYOR SYSTEM MARKET, BY OPERATION

- 3.4 CONVEYOR SYSTEM MARKET, BY COMPONENT

- 3.5 CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY TYPE

- 3.6 CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY TYPE

- 3.7 CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY SUB-INDUSTRY

- 3.8 CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY TYPE

- 3.9 CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY TYPE

- 3.10 CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY TYPE

- 3.11 MINING CONVEYOR SYSTEM MARKET, BY APPLICATION

- 3.12 MINING CONVEYOR SYSTEM MARKET, BY TECHNOLOGY

- 3.13 CONVEYOR SYSTEM MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing adoption of automation across industries

- 4.2.1.2 Rising need for fulfillment, throughput stability, and flow orchestration

- 4.2.1.3 Brownfield distribution center retrofitting and network reconfiguration

- 4.2.2 RESTRAINTS

- 4.2.2.1 High installation and system integration costs

- 4.2.2.2 Operational inflexibility in dynamic fulfillment environments

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of smart conveyor controls and connected sortation systems

- 4.2.3.2 Conveyor software convergence

- 4.2.3.3 Rapid deployment of energy-efficient belt conveyor systems

- 4.2.4 CHALLENGES

- 4.2.4.1 Conveyor performance issues caused by belt wear and component failures

- 4.2.4.2 Integration complexity across heterogeneous automation ecosystems

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 LIMITED INTEROPERABILITY ACROSS AUTOMATION ENVIRONMENTS

- 4.3.2 LACK OF FLEXIBLE CONVEYOR ARCHITECTURES FOR RAPIDLY CHANGING FULFILLMENT OPERATIONS

- 4.3.3 LIMITED REAL-TIME FLOW ORCHESTRATION AND PREDICTIVE THROUGHPUT MANAGEMENT

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL CONVEYOR SYSTEM INDUSTRY

- 5.2 ECOSYSTEM ANALYSIS

- 5.2.1 COMPONENT & TECHNOLOGY PROVIDERS

- 5.2.2 CONVEYOR SYSTEM MANUFACTURERS

- 5.2.3 WAREHOUSE & AUTOMATION SOLUTION PROVIDERS

- 5.2.4 SOFTWARE & SMART CONTROL PROVIDERS

- 5.2.5 END USERS

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL SUPPLIERS

- 5.3.2 COMPONENT AND SUBSYSTEM MANUFACTURERS

- 5.3.3 CONVEYOR SYSTEM MANUFACTURERS/OEMS

- 5.3.4 SYSTEM INTEGRATORS, DISTRIBUTION, AND SERVICE PROVIDERS

- 5.3.5 END USERS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE, BY TYPE, 2023-2025

- 5.4.2 AVERAGE SELLING PRICE, BY REGION

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT DATA FOR HS CODE 842820

- 5.5.2 EXPORT DATA FOR HS CODE 842820

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 BATTERY CELL INSPECTION LINE BY MK NORTH AMERICA

- 5.9.2 SPEED RAIL FRICTION SYSTEM BY MTC & TSUBAKIMOTO MATERIAL HANDLING DIVISION

- 5.9.3 AUTOMATED MATERIAL HANDLING IMPLEMENTATION BY DAIFUKU

- 5.9.4 DORNER SERIES BY DORNER MFG. CORP.

- 5.9.5 ENERGY EFFICIENT CONVEYOR DEPLOYMENT BY BEUMER GROUP

- 5.9.6 SMART CONVEYOR DEPLOYMENT BY INTERROLL

- 5.9.7 AUTOMATED WAREHOUSE AND CONVEYOR INTEGRATION BY DEMATIC

- 5.10 IMPACT OF 2026 IRAN CONFLICT ON CONVEYOR SYSTEM MARKET

- 5.10.1 RAW MATERIAL AND COMPONENT PRICE VOLATILITY

- 5.10.2 SHIPPING AND INDUSTRIAL LOGISTICS DISRUPTIONS

- 5.10.3 PROJECT EXECUTION AND INDUSTRIAL INVESTMENT SLOWDOWN

- 5.10.4 REGIONAL EFFECTS

- 5.11 EUROPE-INDIA TRADE DEALS IMPACT ANALYSIS

- 5.11.1 EU TARIFFS

- 5.11.2 IMPORTS TO INDIA

- 5.11.3 EXPORTS FROM INDIA

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 AUTOMATION & SORTATION SYSTEMS

- 6.1.2 RFID & BARCODE TRACKING

- 6.1.3 PREDICTIVE MAINTENANCE SENSORS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ENERGY-EFFICIENT DRIVES

- 6.2.2 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING

- 6.2.3 AUGMENTED REALITY

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 INTERNET OF THINGS

- 6.3.2 ROBOTICS AND AUTOMATION

- 6.4 PATENT ANALYSIS

- 6.5 IMPACT OF AI ON CONVEYOR SYSTEM MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN CONVEYOR SYSTEM MARKET

- 6.5.3 CASE STUDIES RELATED TO IMPLEMENTATION OF AI IN CONVEYOR SYSTEM MARKET

- 6.5.4 CLIENTS' READINESS TO ADOPT AI IN CONVEYOR SYSTEM MARKET

- 6.6 EMERGING BUSINESS MODELS IN CONVEYOR SYSTEM MARKET

- 6.6.1 CONVEYOR-AS-A-SERVICE MODEL (CAAS): ENABLING SERVICE-DRIVEN MATERIAL HANDLING INFRASTRUCTURE

- 6.6.2 PREDICTIVE MAINTENANCE AND REMOTE MONITORING SERVICES: SHIFTING TOWARD CONTINUOUS CONVEYOR PERFORMANCE MANAGEMENT

- 6.6.3 PERFORMANCE-BASED SERVICE CONTRACTS: LINKING CONVEYOR SERVICE VALUE WITH OPERATIONAL OUTCOMES

- 6.7 FUTURE APPLICATIONS

- 6.7.1 DARK WAREHOUSES ACROSS END-USE INDUSTRIES

- 6.8 ROI BENCHMARKING OF CONVEYOR SYSTEMS AGAINST ADVANCED AUTOMATION TECHNOLOGIES

- 6.8.1 CONVEYOR SYSTEMS VS. AUTONOMOUS MOBILE ROBOTS

- 6.8.2 CONVEYOR SYSTEM VS. ROBOT PICKING TECHNOLOGIES

- 6.8.3 CONVEYOR SYSTEM VS. DRONE-BASED INVENTORY MONITORING

- 6.9 FUTURE MONETIZATION OUTLOOK IN CONVEYOR SYSTEMS

- 6.9.1 SOFTWARE-DRIVEN REVENUE MODELS

- 6.9.2 PREDICTIVE MAINTENANCE AND REMOTE MONITORING SERVICES

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATIONS PERTAINING TO CONVEYOR SYSTEMS, BY INDUSTRY

- 7.1.2 REGULATIONS PERTAINING TO CONVEYOR SYSTEMS, BY REGION

- 7.1.3 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 INDIA: PERFORM, ACHIEVE AND TRADE (PAT) SCHEME

- 7.2.2 CHINA: GREEN MANUFACTURING SYSTEM INITIATIVE

- 7.2.3 JAPAN: GREEN GROWTH STRATEGY

- 7.2.4 SOUTH KOREA: KOREAN GREEN NEW DEAL

- 7.2.5 GERMANY: INDUSTRY 4.0 INITIATIVE

- 7.2.6 UK: INDUSTRIAL ENERGY TRANSFORMATION FUND

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

9 CONVEYOR SYSTEM MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 BELT

- 9.2.1 EXTENSIVE USE IN DIVERSE INDUSTRIES TO DRIVE MARKET

- 9.3 ROLLER

- 9.3.1 SURGE IN E-COMMERCE AND WAREHOUSE MATERIAL HANDLING TO DRIVE MARKET

- 9.4 TRI-PLANAR

- 9.4.1 RAPID DEVELOPMENT OF AIRPORTS IN NORTH AMERICA TO DRIVE MARKET

- 9.5 CRESCENT

- 9.5.1 INCREASING AIRPORT BAGGAGE HANDLING AUTOMATION TO SUPPORT MARKET GROWTH

- 9.6 PALLET

- 9.6.1 BOOMING E-COMMERCE INDUSTRY IN ASIA PACIFIC TO DRIVE MARKET

- 9.7 OVERHEAD

- 9.7.1 IMPROVED PERFORMANCE WITH DEVELOPMENT OF LIGHTWEIGHT MATERIALS TO DRIVE MARKET

- 9.8 FLOOR

- 9.8.1 RISING AUTOMATION IN AUTOMOTIVE MANUFACTURING TO ACCELERATE ADOPTION

- 9.9 BUCKET

- 9.9.1 ADVANCEMENTS IN BUCKET DESIGNS AND MATERIALS TO DRIVE MARKET

- 9.10 CABLE

- 9.10.1 LARGE-SCALE INFRASTRUCTURE AND MINING PROJECTS TO DRIVE MARKET

- 9.11 OTHER TYPES

- 9.12 KEY PRIMARY INSIGHTS

10 CONVEYOR SYSTEM MARKET, BY COMPONENT

- 10.1 INTRODUCTION

- 10.2 ALUMINUM PROFILE

- 10.2.1 RISING SETUP OF EV MANUFACTURING FACTORIES IN EUROPE TO DRIVE THE MARKET

- 10.3 DRIVING UNIT

- 10.3.1 INNOVATIONS IN MODULAR DESIGN AND SMART FEATURES TO DRIVE MARKET

- 10.4 EXTREMITY UNIT

- 10.4.1 NEED FOR ADVANCED CONVEYOR SYSTEMS IN WAREHOUSES AND DISTRIBUTION CENTERS TO DRIVE MARKET

- 10.5 OTHER COMPONENTS

- 10.6 KEY PRIMARY INSIGHTS

11 CONVEYOR SYSTEM MARKET, BY OPERATION

- 11.1 INTRODUCTION

- 11.2 MANUAL

- 11.2.1 EMERGING TREND OF AUTOMATION TO IMPEDE MARKET

- 11.3 SEMI-AUTOMATIC

- 11.3.1 HIGHER ADOPTION IN PRICE-SENSITIVE ASIA PACIFIC COUNTRIES TO DRIVE MARKET

- 11.4 AUTOMATIC

- 11.4.1 FOCUS ON INCREASING PRODUCTIVITY AND EFFICIENCY IN INDUSTRIES TO DRIVE MARKET

- 11.5 KEY PRIMARY INSIGHTS

12 CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY TYPE

- 12.1 INTRODUCTION

- 12.2 BELT

- 12.2.1 RISING AIRPORT MODERNIZATION TO DRIVE BELT CONVEYOR ADOPTION

- 12.3 CRESCENT

- 12.3.1 INCREASING NEED FOR CURVED BAGGAGE ROUTING TO SUPPORT ADOPTION

- 12.4 TRI-PLANAR

- 12.4.1 HIGH DEMAND FROM NORTH AMERICAN REGION TO DRIVE MARKET

- 12.5 OTHER TYPES

- 12.6 KEY PRIMARY INSIGHTS

13 CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY TYPE

- 13.1 INTRODUCTION

- 13.2 BELT

- 13.2.1 GLOBAL EXPANSION OF DISTRIBUTION CENTERS TO DRIVE MARKET

- 13.3 ROLLER

- 13.3.1 INCREASING SCOPE OF E-COMMERCE OPERATIONS TO DRIVE MARKET

- 13.4 PALLET

- 13.4.1 RISING IMPLEMENTATION OF ROBOTICS IN WAREHOUSES TO DRIVE MARKET

- 13.5 OTHER TYPES

- 13.6 KEY PRIMARY INSIGHTS

14 CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY TYPE

- 14.1 INTRODUCTION

- 14.2 BELT

- 14.2.1 INCREASING DEMAND FOR HIGH-CAPACITY BULK MATERIAL TRANSPORTATION TO SUPPORT GROWTH

- 14.3 CABLE

- 14.3.1 DEVELOPMENT OF NEW CABLE MATERIALS AND DESIGNS TO DRIVE MARKET

- 14.4 BUCKET

- 14.4.1 GROWTH IN MINING ACTIVITY TO DRIVE MARKET

- 14.5 OTHER TYPES

- 14.6 KEY PRIMARY INSIGHTS

15 MINING CONVEYOR SYSTEM MARKET, BY APPLICATION

- 15.1 INTRODUCTION

- 15.2 OPEN-PIT MINING

- 15.2.1 PROCESS AUTOMATION WITH CONVEYOR SYSTEMS TO DRIVE MARKET

- 15.3 UNDERGROUND MINING

- 15.3.1 STRINGENT FIRE SAFETY REGULATIONS TO DRIVE THE MARKET

- 15.4 KEY PRIMARY INSIGHTS

16 MINING CONVEYOR SYSTEM MARKET, BY TECHNOLOGY

- 16.1 INTRODUCTION

- 16.2 DRIVE

- 16.2.1 RISING DEPLOYMENT IN NEW MINES TO DRIVE MARKET

- 16.3 GEARLESS

- 16.3.1 FOCUS ON REDUCING ENERGY CONSUMPTION AND OPERATIONAL COSTS TO DRIVE MARKET

- 16.4 AUTOMATED

- 16.4.1 INCREASING DEMAND FOR AUTOMATION FROM MINING COMPANIES TO DRIVE MARKET

- 16.5 KEY PRIMARY INSIGHTS

17 CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY TYPE

- 17.1 INTRODUCTION

- 17.2 FLOOR

- 17.2.1 INCREASING AUTOMATION IN AUTOMOTIVE PRODUCTION LINES TO SUPPORT DEMAND

- 17.3 OVERHEAD

- 17.3.1 NEED FOR SPACE-EFFICIENT VEHICLE BODY HANDLING TO DRIVE ADOPTION

- 17.4 ROLLER

- 17.4.1 RISING AUTOMATION IN AUTOMOTIVE MATERIAL HANDLING TO DRIVE DEMAND

- 17.5 OTHER TYPES

- 17.6 KEY PRIMARY INSIGHTS

18 CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY TYPE

- 18.1 INTRODUCTION

- 18.2 BELT

- 18.2.1 RISE OF ELECTRONICS MANUFACTURING FACTORIES IN ASIA PACIFIC TO DRIVE MARKET

- 18.3 ROLLER

- 18.3.1 SURGE IN MANUFACTURING ACTIVITIES TO DRIVE MARKET

- 18.4 OTHER TYPES

- 18.5 KEY PRIMARY INSIGHTS

19 CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY SUB-INDUSTRY

- 19.1 INTRODUCTION

- 19.2 MEAT & POULTRY

- 19.2.1 INCREASING DEMAND FOR HYGIENIC AND AUTOMATED FOOD PROCESSING TO SUPPORT GROWTH

- 19.3 DAIRY

- 19.3.1 REGULATORY NORMS FOR FOOD PROCESSING TO DRIVE MARKET

- 19.4 OTHER SUB-INDUSTRIES

- 19.5 KEY PRIMARY INSIGHTS

20 CONVEYOR SYSTEM MARKET, BY REGION

- 20.1 INTRODUCTION

- 20.2 ASIA PACIFIC

- 20.2.1 CHINA

- 20.2.1.1 Need for efficient material handling systems to support increasing manufacturing activities to drive market

- 20.2.2 INDIA

- 20.2.2.1 Emphasis on increasing industrial production capacity to drive market

- 20.2.3 JAPAN

- 20.2.3.1 Shift toward automation to replenish aging workforce to drive market

- 20.2.4 SOUTH KOREA

- 20.2.4.1 Strategic investments in advanced manufacturing and automation to drive market

- 20.2.5 REST OF ASIA PACIFIC

- 20.2.1 CHINA

- 20.3 EUROPE

- 20.3.1 GERMANY

- 20.3.1.1 Focus on Industry 4.0 and smart manufacturing systems to drive market

- 20.3.2 FRANCE

- 20.3.2.1 Ongoing modernization of industrial infrastructure to drive market

- 20.3.3 UK

- 20.3.3.1 Government efforts to upgrade existing airports to drive market

- 20.3.4 SPAIN

- 20.3.4.1 Prevalence of multinational and domestic automotive manufacturing plants to drive the market

- 20.3.5 ITALY

- 20.3.5.1 Domestic demands and exports to drive market

- 20.3.6 RUSSIA

- 20.3.6.1 Rising adoption of material handling systems in mining operations to drive market

- 20.3.7 REST OF EUROPE

- 20.3.1 GERMANY

- 20.4 NORTH AMERICA

- 20.4.1 US

- 20.4.1.1 Significant presence of retail companies to drive market

- 20.4.2 CANADA

- 20.4.2.1 Increasing scope of conveyor system applications to drive market

- 20.4.3 MEXICO

- 20.4.3.1 Expansion of electronic manufacturing plants to drive market

- 20.4.1 US

- 20.5 REST OF THE WORLD

- 20.5.1 BRAZIL

- 20.5.1.1 Industrial and infrastructure activity supporting conveyor demand in Brazil

- 20.5.2 SOUTH AFRICA

- 20.5.2.1 Predominance of retail & distribution industry to drive market

- 20.5.3 TURKEY

- 20.5.4 OTHERS

- 20.5.1 BRAZIL

21 COMPETITIVE LANDSCAPE

- 21.1 INTRODUCTION

- 21.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2022-MAY 2026

- 21.3 MARKET SHARE ANALYSIS, 2025

- 21.4 REVENUE ANALYSIS, 2021-2025

- 21.5 COMPANY VALUATION AND FINANCIAL METRICS

- 21.6 BRAND/PRODUCT COMPARISON

- 21.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2026

- 21.7.1 STARS

- 21.7.2 EMERGING LEADERS

- 21.7.3 PERVASIVE PLAYERS

- 21.7.4 PARTICIPANTS

- 21.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2026

- 21.7.5.1 Company footprint

- 21.7.5.2 Region footprint

- 21.7.5.3 Type footprint

- 21.7.5.4 Component footprint

- 21.7.5.5 Industry footprint

- 21.7.5.6 Operation footprint

- 21.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2026

- 21.8.1 PROGRESSIVE COMPANIES

- 21.8.2 RESPONSIVE COMPANIES

- 21.8.3 DYNAMIC COMPANIES

- 21.8.4 STARTING BLOCKS

- 21.8.5 COMPETITIVE BENCHMARKING OF START-UPS/SMES

- 21.8.5.1 Detailed list of key start-ups/SMEs

- 21.8.5.2 Competitive benchmarking of start-ups/SMEs

- 21.9 COMPETITIVE SCENARIO

- 21.9.1 PRODUCT LAUNCHES/ENHANCEMENTS

- 21.9.2 DEALS

- 21.9.3 EXPANSIONS

- 21.9.4 OTHERS

22 COMPANY PROFILES

- 22.1 KEY PLAYERS

- 22.1.1 DAIFUKU CO., LTD.

- 22.1.1.1 Business overview

- 22.1.1.2 Products/Solutions offered

- 22.1.1.3 Recent developments

- 22.1.1.3.1 Product launches/developments

- 22.1.1.3.2 Deals

- 22.1.1.3.3 Expansions

- 22.1.1.3.4 Others

- 22.1.1.4 MnM view

- 22.1.1.4.1 Key strengths

- 22.1.1.4.2 Strategic choices

- 22.1.1.4.3 Weaknesses and competitive threats

- 22.1.2 CONTINENTAL AG

- 22.1.2.1 Business overview

- 22.1.2.2 Products/Solutions offered

- 22.1.2.3 Recent developments

- 22.1.2.3.1 Product launches

- 22.1.2.3.2 Deals

- 22.1.2.3.3 Expansions

- 22.1.2.3.4 Others

- 22.1.2.4 MnM view

- 22.1.2.4.1 Key strengths

- 22.1.2.4.2 Strategic choices

- 22.1.2.4.3 Weaknesses and competitive threats

- 22.1.3 DEMATIC

- 22.1.3.1 Business overview

- 22.1.3.2 Products/Solutions offered

- 22.1.3.3 Recent developments

- 22.1.3.3.1 Product launches

- 22.1.3.3.2 Deals

- 22.1.3.3.3 Others

- 22.1.3.4 MnM view

- 22.1.3.4.1 Key strengths

- 22.1.3.4.2 Strategic choices

- 22.1.3.4.3 Weaknesses and competitive threats

- 22.1.4 VANDERLANDE INDUSTRIES B.V.

- 22.1.4.1 Business overview

- 22.1.4.2 Products/Solutions offered

- 22.1.4.3 Recent developments

- 22.1.4.3.1 Expansions

- 22.1.4.3.2 Others

- 22.1.4.4 MnM view

- 22.1.4.4.1 Key strengths

- 22.1.4.4.2 Strategic choices

- 22.1.4.4.3 Weaknesses and competitive threats

- 22.1.5 INTERROLL GROUP

- 22.1.5.1 Business overview

- 22.1.5.2 Products/Solutions offered

- 22.1.5.3 Recent developments

- 22.1.5.3.1 Product launches

- 22.1.5.3.2 Deals

- 22.1.5.3.3 Expansions

- 22.1.5.3.4 Others

- 22.1.5.4 MnM view

- 22.1.5.4.1 Key strengths

- 22.1.5.4.2 Strategic choices

- 22.1.5.4.3 Weaknesses and competitive threats

- 22.1.6 FIVES GROUP

- 22.1.6.1 Business overview

- 22.1.6.2 Products/Solutions offered

- 22.1.6.3 Recent developments

- 22.1.6.3.1 Product launches/enhancements

- 22.1.6.3.2 Deals

- 22.1.6.3.3 Expansions

- 22.1.6.3.4 Others

- 22.1.7 SIEMENS AG

- 22.1.7.1 Business overview

- 22.1.7.2 Products/Solutions offered

- 22.1.7.3 Recent developments

- 22.1.7.3.1 Product launches

- 22.1.7.3.2 Deals

- 22.1.7.3.3 Expansions

- 22.1.7.3.4 Others

- 22.1.8 BOSCH REXROTH KFT.

- 22.1.8.1 Business overview

- 22.1.8.2 Products/Solutions offered

- 22.1.8.3 Recent developments

- 22.1.8.3.1 Product launches/enhancements

- 22.1.8.3.2 Deals

- 22.1.8.3.3 Expansions

- 22.1.8.3.4 Others

- 22.1.9 DURR GROUP

- 22.1.9.1 Business overview

- 22.1.9.2 Products/Solutions offered

- 22.1.9.3 Recent developments

- 22.1.9.3.1 Product launches/enhancements

- 22.1.9.3.2 Deals

- 22.1.9.3.3 Expansions

- 22.1.9.3.4 Others

- 22.1.10 HONEYWELL INTERNATIONAL, INC.

- 22.1.10.1 Business overview

- 22.1.10.2 Products/Solutions offered

- 22.1.10.3 Recent developments

- 22.1.10.3.1 Product launches

- 22.1.10.3.2 Deals

- 22.1.10.3.3 Expansions

- 22.1.10.3.4 Others

- 22.1.11 MURATA MACHINERY, LTD.

- 22.1.11.1 Business overview

- 22.1.11.2 Products/Solutions offered

- 22.1.11.3 Recent developments

- 22.1.11.3.1 Product launches/enhancements

- 22.1.11.3.2 Deals

- 22.1.11.3.3 Others

- 22.1.12 SWISSLOG HOLDING AG

- 22.1.12.1 Business overview

- 22.1.12.2 Products/Solutions offered

- 22.1.12.3 Recent developments

- 22.1.12.3.1 Product launches/enhancements

- 22.1.12.3.2 Deals

- 22.1.12.3.3 Expansions

- 22.1.12.3.4 Others

- 22.1.13 METSO

- 22.1.13.1 Business overview

- 22.1.13.2 Products/Solutions offered

- 22.1.13.3 Recent developments

- 22.1.13.3.1 Product launches

- 22.1.13.3.2 Deals

- 22.1.13.3.3 Expansions

- 22.1.13.3.4 Others

- 22.1.14 TAIKISHA LTD

- 22.1.14.1 Business overview

- 22.1.14.2 Products/Solutions offered

- 22.1.14.3 Recent developments

- 22.1.14.3.1 Expansions

- 22.1.14.3.2 Others

- 22.1.1 DAIFUKU CO., LTD.

- 22.2 OTHER PLAYERS

- 22.2.1 KNAPP AG

- 22.2.2 TGW LOGISTICS GROUP

- 22.2.3 SEMPERIT AG HOLDING

- 22.2.4 BEUMER GROUP

- 22.2.5 KARDEX

- 22.2.6 HYTROL CONVEYOR COMPANY, INC.

- 22.2.7 SSI SCHAEFER

- 22.2.8 WESTFALIA TECHNOLOGIES, INC.

- 22.2.9 DMW&H

- 22.2.10 OMNIA DELLA TOFFOLA S.P.A.

- 22.2.11 FLEXLINK

- 22.2.12 FLEXICON CORPORATION

- 22.2.13 MECALUX, S.A.

23 RESEARCH METHODOLOGY

- 23.1 RESEARCH DATA

- 23.1.1 SECONDARY DATA

- 23.1.1.1 Secondary sources

- 23.1.1.2 Key data from secondary sources

- 23.1.2 PRIMARY DATA

- 23.1.2.1 Primary interviewees

- 23.1.2.2 Sampling techniques and data collection methods

- 23.1.1 SECONDARY DATA

- 23.2 MARKET SIZE ESTIMATION

- 23.2.1 BOTTOM-UP APPROACH

- 23.2.2 TOP-DOWN APPROACH

- 23.3 DATA TRIANGULATION

- 23.4 FACTOR ANALYSIS

- 23.5 RESEARCH ASSUMPTIONS

- 23.5.1 GLOBAL ASSUMPTIONS

- 23.5.2 INDUSTRY ASSUMPTIONS

- 23.6 RESEARCH LIMITATIONS

- 23.7 RISK ASSESSMENT

24 APPENDIX

- 24.1 DISCUSSION GUIDE

- 24.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 24.3 CUSTOMIZATION OPTIONS

- 24.3.1 RETAIL INDUSTRY CONVEYOR SYSTEM MARKET, BY TYPE (AT COUNTRY LEVEL)

- 24.3.1.1 Belt

- 24.3.1.2 Roller

- 24.3.1.3 Pallet

- 24.3.2 COMPANY PROFILES

- 24.3.2.1 Additional company profiles (up to five)

- 24.3.1 RETAIL INDUSTRY CONVEYOR SYSTEM MARKET, BY TYPE (AT COUNTRY LEVEL)

- 24.4 RELATED REPORTS

- 24.5 AUTHOR DETAILS

List of Tables

- TABLE 1 CONVEYOR SYSTEM MARKET DEFINITION, BY TYPE

- TABLE 2 CONVEYOR SYSTEM MARKET DEFINITION, BY COMPONENT

- TABLE 3 MINING CONVEYOR SYSTEM MARKET DEFINITION, BY APPLICATION

- TABLE 4 MINING CONVEYOR SYSTEM MARKET DEFINITION, BY TECHNOLOGY

- TABLE 5 INCLUSIONS AND EXCLUSIONS

- TABLE 6 CURRENCY EXCHANGE RATES, 2020-2025

- TABLE 7 CONVEYOR SYSTEM APPLICATIONS ACROSS LARGE SCALE FULFILLMENT NETWORKS

- TABLE 8 COST DISTRIBUTION IN CONVEYOR SYSTEM IMPLEMENTATION PROJECTS

- TABLE 9 INDUSTRIES MOST EXPOSED TO CONVEYOR INFLEXIBILITY RISKS

- TABLE 10 USE OF ENERGY-EFFICIENT CONVEYOR SYSTEMS, BY MANUFACTURERS

- TABLE 11 TRADITIONAL CONVEYOR SYSTEMS V/S SOFTWARE DRIVEN CONVEYOR SYSTEM

- TABLE 12 USE OF ENERGY-EFFICIENT CONVEYOR SYSTEMS, BY END INDUSTRY

- TABLE 13 IMPACT ANALYSIS OF MARKET DYNAMICS

- TABLE 14 STRATEGIC MOVES BY KEY PLAYERS IN CONVEYOR SYSTEM MARKET

- TABLE 15 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2030

- TABLE 16 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 17 AVERAGE SELLING PRICE OF CONVEYOR SYSTEMS, BY TYPE, 2023-2025 (USD)

- TABLE 18 AVERAGE SELLING PRICE OF CONVEYOR SYSTEMS, BY REGION, 2023-2025 (USD)

- TABLE 19 CONFERENCES AND EVENTS, 2026-2027

- TABLE 20 DETAILS ON FUNDING ACTIVITIES, 2022-2024

- TABLE 21 KEY COUNTRY LEVEL IMPACT OF THE 2026 IRAN CONFLICT ON CONVEYOR SYSTEM MARKET

- TABLE 22 IMPORT TARIFFS ON CONVEYOR SYSTEM MARKET AND KEY COMPONENTS IN INDIA

- TABLE 23 IMPACT OF TRADE LIBERALIZATION ON CONVEYOR SYSTEM IMPORTS INTO INDIA

- TABLE 24 IMPACT OF TRADE LIBERALIZATION ON CONVEYOR SYSTEM EXPORTS FROM INDIA

- TABLE 25 BUSINESS IMPACT OF AI AND MACHINE LEARNING IN CONVEYOR SYSTEMS

- TABLE 26 PATENT ANALYSIS

- TABLE 27 OVERVIEW OF KEY PRACTICES OPTED BY MANUFACTURERS/OEMS

- TABLE 28 VANDERLANDE AI-BASED PREDICTIVE MAINTENANCE IMPLEMENTATION IN CONVEYOR SYSTEM MARKET

- TABLE 29 DEMATIC AI-DRIVEN CONVEYOR OPTIMIZATION IMPLEMENTATION IN CONVEYOR SYSTEM MARKET

- TABLE 30 FMH CONVEYORS AI ENABLED WAREHOUSE AUTOMATION IMPLEMENTATION IN CONVEYOR SYSTEM MARKET

- TABLE 31 INDUSTRY ADOPTION TRENDS FOR CONVEYOR-AS-A-SERVICE

- TABLE 32 INDUSTRY-WISE CONVEYOR COMPONENTS REQUIRING PREDICTIVE MAINTENANCE

- TABLE 33 INDUSTRY-SPECIFIC KPI STRUCTURES IN PERFORMANCE-BASED CONVEYOR SERVICE CONTRACTS

- TABLE 34 ROLE OF CONVEYOR SYSTEMS IN DARK WAREHOUSES

- TABLE 35 CONVEYOR SYSTEMS VS. AMRS

- TABLE 36 CONVEYOR SYSTEMS VS. ROBOT PICKING TECHNOLOGIES

- TABLE 37 CONVEYOR SYSTEMS VS. DRONE-BASED INVENTORY MONITORING

- TABLE 38 REVENUE STREAMS FROM PREDICTIVE MAINTENANCE AND REMOTE MONITORING SERVICES

- TABLE 39 PREDICTIVE MAINTENANCE AND REMOTE MONITORING SERVICES

- TABLE 40 REGULATIONS PERTAINING TO CONVEYOR SYSTEMS, BY INDUSTRY

- TABLE 41 REGULATIONS PERTAINING TO CONVEYOR SYSTEMS, BY REGION

- TABLE 42 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 43 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 44 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 45 SUSTAINABILITY INITIATIVES PERTAINING TO INDIA

- TABLE 46 SUSTAINABILITY INITIATIVES PERTAINING TO CHINA

- TABLE 47 SUSTAINABILITY INITIATIVES PERTAINING TO JAPAN

- TABLE 48 SUSTAINABILITY INITIATIVES PERTAINING TO SOUTH KOREA

- TABLE 49 SUSTAINABILITY INITIATIVES PERTAINING TO GERMANY

- TABLE 50 SUSTAINABILITY INITIATIVES PERTAINING TO UK

- TABLE 51 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY INDUSTRY (%)

- TABLE 52 KEY BUYING CRITERIA, BY INDUSTRY

- TABLE 53 CONVEYOR SYSTEM MARKET, BY TYPE, 2022-2025 (THOUSAND METERS)

- TABLE 54 CONVEYOR SYSTEM MARKET, BY TYPE, 2026-2033 (THOUSAND METERS)

- TABLE 55 CONVEYOR SYSTEM MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 56 CONVEYOR SYSTEM MARKET, BY TYPE, 2026-2033 (USD MILLION)

- TABLE 57 BELT: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 58 BELT: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 59 BELT: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 60 BELT: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 61 ROLLER: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 62 ROLLER: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 63 ROLLER: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 64 ROLLER: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 65 TRI-PLANAR: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 66 TRI-PLANAR: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 67 TRI-PLANAR: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 68 TRI-PLANAR: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 69 CRESCENT: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 70 CRESCENT: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 71 CRESCENT: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 72 CRESCENT: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 73 PALLET: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 74 PALLET: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 75 PALLET: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 76 PALLET: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 77 OVERHEAD: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 78 OVERHEAD: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 79 OVERHEAD: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 80 OVERHEAD: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 81 FLOOR: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 82 FLOOR: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 83 FLOOR: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 84 FLOOR: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 85 BUCKET: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 86 BUCKET: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 87 BUCKET: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 88 BUCKET: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 89 CABLE: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 90 CABLE: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 91 CABLE: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 92 CABLE: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 93 OTHER TYPES: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 94 OTHER TYPES: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 95 OTHER TYPES: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 96 OTHER TYPES: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 97 CONVEYOR SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 98 CONVEYOR SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 99 ALUMINUM PROFILE: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 100 ALUMINUM PROFILE: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 101 DRIVING UNIT: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 102 DRIVING UNIT: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 103 EXTREMITY UNIT: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 104 EXTREMITY UNIT: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 105 OTHER COMPONENTS: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 106 OTHER COMPONENTS: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 107 CONVEYOR SYSTEM MARKET, BY OPERATION, 2022-2025 (USD MILLION)

- TABLE 108 CONVEYOR SYSTEM MARKET, BY OPERATION, 2026-2033 (USD MILLION)

- TABLE 109 MANUAL: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 110 MANUAL: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 111 SEMI-AUTOMATIC: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 112 SEMI-AUTOMATIC: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 113 AUTOMATIC: CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 114 AUTOMATIC: CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 115 CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY TYPE, 2022-2025 (THOUSAND METERS)

- TABLE 116 CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY TYPE, 2026-2033 (THOUSAND METERS)

- TABLE 117 CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 118 CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY TYPE, 2026-2033 (USD MILLION)

- TABLE 119 BELT: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 120 BELT: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 121 BELT: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 122 BELT: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 123 CRESCENT: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 124 CRESCENT: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 125 CRESCENT: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 126 CRESCENT: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 127 TRI-PLANAR: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 128 TRI-PLANAR: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 129 TRI-PLANAR: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 130 TRI-PLANAR: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 131 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 132 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 133 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 134 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 135 CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY TYPE, 2022-2025 (THOUSAND METERS)

- TABLE 136 CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY TYPE, 2026-2033 (THOUSAND METERS)

- TABLE 137 CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY TYPE, 2022-2025 (USD MILLON)

- TABLE 138 CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY TYPE, 2026-2033 (USD MILLION)

- TABLE 139 BELT: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 140 BELT: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 141 BELT: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 142 BELT: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 143 ROLLER: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 144 ROLLER: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 145 ROLLER: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 146 ROLLER: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 147 PALLET: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 148 PALLET: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 149 PALLET: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 150 PALLET: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 151 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 152 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 153 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 154 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 155 CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY TYPE, 2022-2025 (THOUSAND METERS)

- TABLE 156 CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY TYPE, 2026-2033 (THOUSAND METERS)

- TABLE 157 CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 158 CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY TYPE, 2026-2033 (USD MILLION)

- TABLE 159 BELT: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 160 BELT: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 161 BELT: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 162 BELT: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 163 CABLE: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 164 CABLE: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 165 CABLE: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 166 CABLE: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 167 BUCKET: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 168 BUCKET: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 169 BUCKET: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 170 BUCKET: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 171 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 172 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 173 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 174 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 175 MINING CONVEYOR SYSTEM MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 176 MINING CONVEYOR SYSTEM MARKET, BY APPLICATION, 2026-2033 (USD MILLION)

- TABLE 177 NUMBER OF OPEN-PIT MINES GLOBALLY, 2025

- TABLE 178 OPEN-PIT MINING CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 179 OPEN-PIT MINING CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 180 NUMBER OF UNDERGROUND MINES GLOBALLY, 2025

- TABLE 181 UNDERGROUND MINING CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 182 UNDERGROUND MINING CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 183 MINING CONVEYOR SYSTEM MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 184 MINING CONVEYOR SYSTEM MARKET, BY TECHNOLOGY, 2026-2033 (USD MILLION)

- TABLE 185 DRIVE MINING CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 186 DRIVE MINING CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 187 GEARLESS MINING CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 188 GEARLESS MINING CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 189 AUTOMATED MINING CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 190 AUTOMATED MINING CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 191 CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY TYPE, 2022-2025 (THOUSAND METERS)

- TABLE 192 CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY TYPE, 2026-2033 (THOUSAND METERS)

- TABLE 193 CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 194 CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY TYPE, 2026-2033 (USD MILLION)

- TABLE 195 FLOOR: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 196 FLOOR: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 197 FLOOR: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 198 FLOOR: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 199 OVERHEAD: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 200 OVERHEAD: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 201 OVERHEAD: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 202 OVERHEAD: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 203 ROLLER: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 204 ROLLER: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 205 ROLLER: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 206 ROLLER: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 207 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 208 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 209 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 210 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 211 CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY TYPE, 2022-2025 (THOUSAND METERS)

- TABLE 212 CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY TYPE, 2026-2033 (THOUSAND METERS)

- TABLE 213 CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 214 CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY TYPE, 2026-2033 (USD MILLION)

- TABLE 215 BELT: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 216 BELT: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 217 BELT: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 218 BELT: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 219 ROLLER: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 220 ROLLER: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 221 ROLLER: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 222 ROLLER: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 223 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 224 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 225 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 226 OTHER TYPES: CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 227 CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY SUB-INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 228 CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY SUB-INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 229 CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY SUB-INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 230 CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY SUB-INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 231 MEAT & POULTRY: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 232 MEAT & POULTRY: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 233 MEAT & POULTRY: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 234 MEAT & POULTRY: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 235 DAIRY: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 236 DAIRY: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 237 DAIRY: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 238 DAIRY: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 239 OTHER SUB-INDUSTRIES: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 240 OTHER SUB-INDUSTRIES: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 241 OTHER SUB-INDUSTRIES: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 242 OTHER SUB-INDUSTRIES: CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY REGION, 2026-2033 (USD MILLION)

- TABLE 243 CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND METERS)

- TABLE 244 CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND METERS)

- TABLE 245 CONVEYOR SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 246 CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 247 ASIA PACIFIC: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND METERS)

- TABLE 248 ASIA PACIFIC: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND METERS)

- TABLE 249 ASIA PACIFIC: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 250 ASIA PACIFIC: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 251 CHINA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 252 CHINA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 253 CHINA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 254 CHINA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 255 INDIA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 256 INDIA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 257 INDIA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 258 INDIA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 259 JAPAN: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 260 JAPAN: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 261 JAPAN: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 262 JAPAN: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 263 SOUTH KOREA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 264 SOUTH KOREA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 265 SOUTH KOREA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 266 SOUTH KOREA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 267 REST OF ASIA PACIFIC: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 268 REST OF ASIA PACIFIC: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 269 REST OF ASIA PACIFIC: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 270 REST OF ASIA PACIFIC: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 271 EUROPE: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND METERS)

- TABLE 272 EUROPE: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND METERS)

- TABLE 273 EUROPE: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 274 EUROPE: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 275 GERMANY: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 276 GERMANY: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 277 GERMANY: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 278 GERMANY: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 279 FRANCE: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 280 FRANCE: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 281 FRANCE: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 282 FRANCE: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 283 UK: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 284 UK: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 285 UK: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 286 UK: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 287 SPAIN: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 288 SPAIN: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 289 SPAIN: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 290 SPAIN: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 291 ITALY: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 292 ITALY: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 293 ITALY: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 294 ITALY: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 295 RUSSIA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 296 RUSSIA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 297 RUSSIA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 298 RUSSIA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 299 REST OF EUROPE: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 300 REST OF EUROPE: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 301 REST OF EUROPE: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 302 REST OF EUROPE: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 303 NORTH AMERICA: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND METERS)

- TABLE 304 NORTH AMERICA: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND METERS)

- TABLE 305 NORTH AMERICA: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 306 NORTH AMERICA: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 307 US: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 308 US: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 309 US: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 310 US: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 311 CANADA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 312 CANADA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 313 CANADA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 314 CANADA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 315 MEXICO: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 316 MEXICO: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 317 MEXICO: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 318 MEXICO: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 319 REST OF THE WORLD: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND METERS)

- TABLE 320 REST OF THE WORLD: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND METERS)

- TABLE 321 REST OF THE WORLD: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 322 REST OF THE WORLD: CONVEYOR SYSTEM MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 323 BRAZIL: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 324 BRAZIL: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 325 BRAZIL: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 326 BRAZIL: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 327 SOUTH AFRICA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (THOUSAND METERS)

- TABLE 328 SOUTH AFRICA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (THOUSAND METERS)

- TABLE 329 SOUTH AFRICA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 330 SOUTH AFRICA: CONVEYOR SYSTEM MARKET, BY INDUSTRY, 2026-2033 (USD MILLION)

- TABLE 331 OVERVIEW OF STRATEGIES ADOPTED BY COMPANIES IN CONVEYOR SYSTEM MARKET

- TABLE 332 CONVEYOR SYSTEM MARKET: MARKET SHARE ANALYSIS, 2025

- TABLE 333 CONVEYOR SYSTEM MARKET: REGION FOOTPRINT

- TABLE 334 CONVEYOR SYSTEM MARKET: TYPE FOOTPRINT

- TABLE 335 CONVEYOR SYSTEM MARKET: COMPONENT FOOTPRINT

- TABLE 336 CONVEYOR SYSTEM MARKET: INDUSTRY FOOTPRINT

- TABLE 337 CONVEYOR SYSTEM MARKET: OPERATION FOOTPRINT

- TABLE 338 CONVEYOR SYSTEM MARKET: DETAILED LIST OF START-UPS/SMES

- TABLE 339 CONVEYOR SYSTEM MARKET: COMPETITIVE BENCHMARKING OF START-UPS/SMES

- TABLE 340 CONVEYOR SYSTEM MARKET: PRODUCT LAUNCHES/ENHANCEMENTS, 2025-2026

- TABLE 341 CONVEYOR SYSTEM MARKET: DEALS, 2025-2026

- TABLE 342 CONVEYOR SYSTEM MARKET: EXPANSIONS, 2025-2026

- TABLE 343 CONVEYOR SYSTEM MARKET: OTHERS, 2025-2026

- TABLE 344 DAIFUKU CO., LTD.: COMPANY OVERVIEW

- TABLE 345 DAIFUKU CO., LTD.: PRODUCTS/SOLUTIONS OFFERED

- TABLE 346 DAIFUKU CO., LTD.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 347 DAIFUKU CO., LTD.: DEALS

- TABLE 348 DAIFUKU CO., LTD.: EXPANSIONS

- TABLE 349 DAIFUKU CO., LTD.: OTHERS

- TABLE 350 CONTINENTAL AG: COMPANY OVERVIEW

- TABLE 351 CONTINENTAL AG: PRODUCTS/SOLUTIONS OFFERED

- TABLE 352 CONTINENTAL AG: PRODUCT LAUNCHES

- TABLE 353 CONTINENTAL AG: DEALS

- TABLE 354 CONTINENTAL AG: EXPANSIONS

- TABLE 355 CONTINENTAL AG: OTHERS

- TABLE 356 DEMATIC: COMPANY OVERVIEW

- TABLE 357 DEMATIC: PRODUCTS/SOLUTIONS OFFERED

- TABLE 358 DEMATIC: PRODUCT LAUNCHES

- TABLE 359 DEMATIC: DEALS

- TABLE 360 DEMATIC: OTHERS

- TABLE 361 VANDERLANDE INDUSTRIES B.V.: COMPANY OVERVIEW

- TABLE 362 VANDERLANDE INDUSTRIES B.V.: PRODUCTS/SOLUTIONS OFFERED

- TABLE 363 VANDERLANDE INDUSTRIES B.V.: EXPANSIONS

- TABLE 364 VANDERLANDE INDUSTRIES B.V.: OTHERS

- TABLE 365 INTERROLL GROUP: COMPANY OVERVIEW

- TABLE 366 INTERROLL GROUP: PRODUCTS/SOLUTIONS OFFERED

- TABLE 367 INTERROLL GROUP: PRODUCT LAUNCHES

- TABLE 368 INTERROLL GROUP: DEALS

- TABLE 369 INTERROLL GROUP: EXPANSIONS

- TABLE 370 INTERROLL GROUP: OTHERS

- TABLE 371 FIVES GROUP: COMPANY OVERVIEW

- TABLE 372 FIVES GROUP: PRODUCTS/SOLUTIONS OFFERED

- TABLE 373 FIVES GROUP: PRODUCT LAUNCHES/ENHANCEMENTS

- TABLE 374 FIVES GROUP: DEALS

- TABLE 375 FIVES GROUP: EXPANSIONS

- TABLE 376 FIVES GROUP: OTHERS

- TABLE 377 SIEMENS AG: COMPANY OVERVIEW

- TABLE 378 SIEMENS AG: PRODUCTS/SOLUTIONS OFFERED

- TABLE 379 SIEMENS AG: PRODUCT LAUNCHES

- TABLE 380 SIEMENS AG: DEALS

- TABLE 381 SIEMENS AG: EXPANSIONS

- TABLE 382 SIEMENS AG: OTHERS

- TABLE 383 BOSCH REXROTH KFT.: COMPANY OVERVIEW

- TABLE 384 BOSCH REXROTH KFT.: PRODUCTS/SOLUTIONS OFFERED

- TABLE 385 BOSCH REXROTH KFT.: PRODUCT LAUNCHES/ENHANCEMENTS

- TABLE 386 BOSCH REXROTH KFT.: DEALS

- TABLE 387 BOSCH REXROTH KFT.: EXPANSIONS

- TABLE 388 BOSCH REXROTH KFT.: OTHERS

- TABLE 389 DURR GROUP: COMPANY OVERVIEW

- TABLE 390 DURR GROUP: PRODUCTS/SOLUTIONS OFFERED

- TABLE 391 DURR GROUP: PRODUCT LAUNCHES/ENHANCEMENTS

- TABLE 392 DURR GROUP: DEALS

- TABLE 393 DURR GROUP: EXPANSIONS

- TABLE 394 DURR GROUP: OTHERS

- TABLE 395 HONEYWELL INTERNATIONAL INC.: COMPANY OVERVIEW

- TABLE 396 HONEYWELL INTERNATIONAL INC.: PRODUCTS/SOLUTIONS OFFERED

- TABLE 397 HONEYWELL INTERNATIONAL INC.: PRODUCT LAUNCHES

- TABLE 398 HONEYWELL INTERNATIONAL INC.: DEALS

- TABLE 399 HONEYWELL INTERNATIONAL INC.: EXPANSIONS

- TABLE 400 HONEYWELL INTERNATIONAL INC.: OTHERS

- TABLE 401 MURATA MACHINERY, LTD.: COMPANY OVERVIEW

- TABLE 402 MURATA MACHINERY, LTD.: PRODUCTS/SOLUTIONS OFFERED

- TABLE 403 MURATA MACHINERY, LTD.: PRODUCT LAUNCHES/ENHANCEMENTS

- TABLE 404 MURATA MACHINERY, LTD.: DEALS

- TABLE 405 MURATA MACHINERY, LTD.: OTHERS

- TABLE 406 SWISSLOG HOLDING AG: COMPANY OVERVIEW

- TABLE 407 SWISSLOG HOLDING AG: PRODUCTS/SOLUTIONS OFFERED

- TABLE 408 SWISSLOG HOLDING AG: PRODUCT LAUNCHES/ENHANCEMENTS

- TABLE 409 SWISSLOG HOLDING AG: DEALS

- TABLE 410 SWISSLOG HOLDING AG: EXPANSIONS

- TABLE 411 SWISSLOG HOLDING AG: OTHERS

- TABLE 412 METSO: COMPANY OVERVIEW

- TABLE 413 METSO: PRODUCTS/SOLUTIONS OFFERED

- TABLE 414 METSO: PRODUCT LAUNCHES

- TABLE 415 METSO: DEALS

- TABLE 416 METSO: EXPANSIONS

- TABLE 417 METSO: OTHERS

- TABLE 418 TAIKISHA LTD: COMPANY OVERVIEW

- TABLE 419 TAIKISHA LTD: PRODUCTS/SOLUTIONS OFFERED

- TABLE 420 TAIKISHA LTD: EXPANSIONS

- TABLE 421 TAIKISHA LTD.: OTHERS

- TABLE 422 KNAPP AG: COMPANY OVERVIEW

- TABLE 423 TGW LOGISTICS GROUP: COMPANY OVERVIEW

- TABLE 424 SEMPERIT AG HOLDING: COMPANY OVERVIEW

- TABLE 425 BEUMER GROUP: COMPANY OVERVIEW

- TABLE 426 KARDEX: COMPANY OVERVIEW

- TABLE 427 HYTROL CONVEYOR COMPANY, INC.: COMPANY OVERVIEW

- TABLE 428 SSI SCHAEFER: COMPANY OVERVIEW

- TABLE 429 WESTFALIA TECHNOLOGIES, INC.: COMPANY OVERVIEW

- TABLE 430 DMW&H: COMPANY OVERVIEW

- TABLE 431 OMNIA DELLA TOFFOLA SPA: COMPANY OVERVIEW

- TABLE 432 FLEXLINK: COMPANY OVERVIEW

- TABLE 433 FLEXICON CORPORATION: COMPANY OVERVIEW

- TABLE 434 MECALUX, S.A.: COMPANY OVERVIEW

- TABLE 435 ASSUMPTIONS FOR FOOD & BEVERAGE INDUSTRY

- TABLE 436 ASSUMPTIONS FOR AUTOMOTIVE INDUSTRY

- TABLE 437 ASSUMPTIONS FOR RETAIL & DISTRIBUTION INDUSTRY

- TABLE 438 ASSUMPTIONS FOR AIRPORT INDUSTRY

- TABLE 439 ASSUMPTIONS FOR ELECTRONICS INDUSTRY

- TABLE 440 ASSUMPTIONS FOR MINING INDUSTRY

- TABLE 441 RISK ASSESSMENT

List of Figures

- FIGURE 1 CONVEYOR SYSTEM MARKET SEGMENTATION

- FIGURE 2 CONVEYOR SYSTEM MARKET DYNAMICS

- FIGURE 3 CONVEYOR SYSTEM MARKET GROWTH, 2022-2033

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN CONVEYOR SYSTEM MARKET

- FIGURE 5 DISRUPTIVE TRENDS IMPACTING GROWTH OF CONVEYOR SYSTEM MARKET

- FIGURE 6 SEMI-AUTOMATIC AND DRIVING UNITS SEGMENTS TO ACHIEVE SIGNIFICANT GROWTH IN 2026-2033

- FIGURE 7 ASIA PACIFIC TO ACCOUNT FOR LARGEST GROWING MARKET DURING FORECAST PERIOD

- FIGURE 8 RISING AUTOMATION ACROSS INDUSTRIES TO DRIVE MARKET

- FIGURE 9 BELT CONVEYOR SYSTEMS TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 10 AUTOMATIC TO SURPASS OTHER SEGMENTS DURING FORECAST PERIOD

- FIGURE 11 DRIVING UNIT SEGMENT TO HOLD LEADING SHARE DURING FORECAST PERIOD

- FIGURE 12 PALLET SEGMENT TO BE FASTEST-GROWING SEGMENT IN RETAIL & DISTRIBUTION INDUSTRY DURING FORECAST PERIOD

- FIGURE 13 BELT SEGMENT TO EXPERIENCE SIGNIFICANT GROWTH IN ELECTRONICS INDUSTRY DURING FORECAST PERIOD

- FIGURE 14 MEAT & POULTRY SEGMENT TO DOMINATE FOOD & BEVERAGE INDUSTRY DURING FORECAST PERIOD

- FIGURE 15 OVERHEAD SEGMENT TO BE FASTEST-GROWING SEGMENT IN AUTOMOTIVE INDUSTRY DURING FORECAST PERIOD

- FIGURE 16 BELT SEGMENT TO BE DOMINANT IN AIRPORT INDUSTRY DURING FORECAST PERIOD

- FIGURE 17 BUCKET TO FORM FASTEST-GROWING SEGMENT IN MINING INDUSTRY DURING FORECAST PERIOD

- FIGURE 18 OPEN-PIT MINING SEGMENT TO BE LARGER THAN UNDERGROUND MINING SEGMENT DURING FORECAST PERIOD

- FIGURE 19 DRIVE TO BE LARGEST MARKET SEGMENT DURING FORECAST PERIOD

- FIGURE 20 EUROPE AND NORTH AMERICA TO HOLD LARGEST MARKET SHARES DURING FORECAST PERIOD

- FIGURE 21 CONVEYOR SYSTEM MARKET DYNAMICS

- FIGURE 22 ECOSYSTEM ANALYSIS

- FIGURE 23 SUPPLY CHAIN ANALYSIS

- FIGURE 24 AVERAGE SELLING PRICE OF CONVEYOR SYSTEMS, BY TYPE, 2023-2025 (USD)

- FIGURE 25 AVERAGE SELLING PRICE OF CONVEYOR SYSTEMS, BY REGION, 2023-2025 (USD)

- FIGURE 26 IMPORT DATA, BY COUNTRY, 2021-2025 (USD THOUSAND)

- FIGURE 27 EXPORT DATA, BY COUNTRY, 2021-2025 (USD THOUSAND)

- FIGURE 28 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 29 INVESTMENT AND FUNDING SCENARIO, 2022-2025

- FIGURE 30 PATENT ANALYSIS

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY INDUSTRY

- FIGURE 32 KEY BUYING CRITERIA, BY INDUSTRY

- FIGURE 33 CONVEYOR SYSTEM MARKET, BY TYPE, 2026-2033 (USD MILLION)

- FIGURE 34 CONVEYOR SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- FIGURE 35 CONVEYOR SYSTEM MARKET, BY OPERATION, 2026-2033 (USD MILLION)

- FIGURE 36 CONVEYOR SYSTEM MARKET FOR AIRPORT INDUSTRY, BY TYPE, 2026-2033 (USD MILLION)

- FIGURE 37 CONVEYOR SYSTEM MARKET FOR RETAIL & DISTRIBUTION INDUSTRY, BY TYPE, 2026-2033 (USD MILLION)

- FIGURE 38 CONVEYOR SYSTEM MARKET FOR MINING INDUSTRY, BY TYPE, 2026-2033 (USD MILLION)

- FIGURE 39 MINING CONVEYOR SYSTEM MARKET, BY APPLICATION, 2026-2033 (USD MILLION)

- FIGURE 40 MINING CONVEYOR SYSTEM MARKET, BY TECHNOLOGY, 2026-2033 (USD MILLION)

- FIGURE 41 CONVEYOR SYSTEM MARKET FOR AUTOMOTIVE INDUSTRY, BY TYPE, 2026-2033 (USD MILLION)

- FIGURE 42 CONVEYOR SYSTEM MARKET FOR ELECTRONICS INDUSTRY, BY TYPE, 2026-2033 (USD MILLION)

- FIGURE 43 CONVEYOR SYSTEM MARKET FOR FOOD & BEVERAGE INDUSTRY, BY SUB-INDUSTRY, 2026-2033 (USD MILLION)

- FIGURE 44 CONVEYOR SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- FIGURE 45 ASIA PACIFIC: CONVEYOR SYSTEM MARKET SNAPSHOT

- FIGURE 46 EUROPE: CONVEYOR SYSTEM MARKET SNAPSHOT

- FIGURE 47 NORTH AMERICA: CONVEYOR SYSTEM MARKET SNAPSHOT

- FIGURE 48 REST OF THE WORLD, 2026-2033 (USD MILLION)

- FIGURE 49 MARKET SHARE ANALYSIS OF KEY PLAYERS, 2021-2025

- FIGURE 50 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2021-2025

- FIGURE 51 COMPANY VALUATION OF KEY PLAYERS

- FIGURE 52 FINANCIAL MATRIX OF KEY PLAYERS

- FIGURE 53 CONVEYOR SYSTEM MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 54 CONVEYOR SYSTEM MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2026

- FIGURE 55 CONVEYOR SYSTEM MARKET: COMPANY FOOTPRINT

- FIGURE 56 CONVEYOR SYSTEM MARKET: COMPANY EVALUATION MATRIX (START-UPS/SMES), 2026

- FIGURE 57 DAIFUKU CO., LTD.: COMPANY SNAPSHOT

- FIGURE 58 CONTINENTAL AG: COMPANY SNAPSHOT

- FIGURE 59 DEMATIC: COMPANY SNAPSHOT

- FIGURE 60 VANDERLANDE INDUSTRIES B.V.: COMPANY SNAPSHOT

- FIGURE 61 INTERROLL GROUP: COMPANY SNAPSHOT

- FIGURE 62 FIVES GROUP: COMPANY SNAPSHOT

- FIGURE 63 SIEMENS AG: COMPANY SNAPSHOT

- FIGURE 64 BOSCH REXROTH KFT.: COMPANY SNAPSHOT

- FIGURE 65 DURR GROUP: COMPANY SNAPSHOT

- FIGURE 66 HONEYWELL INTERNATIONAL INC.: COMPANY SNAPSHOT

- FIGURE 67 METSO: COMPANY SNAPSHOT

- FIGURE 68 TAIKISHA LTD: COMPANY SNAPSHOT

- FIGURE 69 RESEARCH DESIGN

- FIGURE 70 RESEARCH DESIGN MODEL

- FIGURE 71 BREAKDOWN OF PRIMARY INTERVIEWS

- FIGURE 72 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 73 BOTTOM-UP APPROACH (INDUSTRY AND REGION)

- FIGURE 74 TOP-DOWN APPROACH (TYPE AND COMPONENT)

- FIGURE 75 DATA TRIANGULATION

- FIGURE 76 GROWTH PROJECTIONS FROM DEMAND-SIDE DRIVERS

- FIGURE 77 DEMAND- AND SUPPLY-SIDE FACTOR ANALYSIS