PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045695

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045695

Analog Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

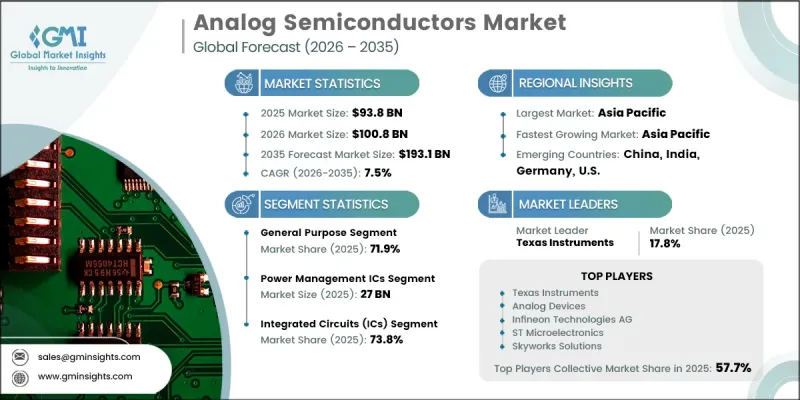

The Global Analog Semiconductors Market was valued at USD 93.8 billion in 2025 and is estimated to grow at a CAGR of 7.5% to reach USD 193.1 billion by 2035.

Growth in the analog semiconductors industry is supported by the rising adoption of vehicle electrification technologies, increasing demand for efficient power regulation systems, and the growing use of safety-focused electronic components across industries. Expanding industrial automation activities are also contributing to market growth, as advanced manufacturing systems require accurate signal processing and real-time operational control. In addition, increasing emphasis on energy-efficient electronic products is creating strong demand for high-performance analog components capable of optimizing power consumption. Rapid upgrades in communication infrastructure and the expansion of next-generation connectivity networks are further accelerating industry development. Investments in renewable energy projects and power conversion technologies are also strengthening market opportunities for analog semiconductors manufacturers. Furthermore, advancements in semiconductor design processes, including the integration of intelligent optimization technologies, are helping improve design precision, reduce development complexity, and accelerate the production cycle for analog integrated circuits. These technological improvements continue to support the broader expansion of the analog semiconductors market across multiple end-use industries worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $93.8 Billion |

| Forecast Value | $193.1 Billion |

| CAGR | 7.5% |

The analog semiconductor market is witnessing strong momentum due to the growing transition toward electric mobility, which is significantly increasing the requirement for advanced power management technologies. Rising production of electrified vehicles is creating higher demand for analog semiconductor devices used in battery management systems, power delivery networks, and motor control applications. At the same time, expanding industrial automation is further supporting market growth, as automated systems depend heavily on analog integrated circuits for precise sensing, control functions, and operational efficiency. The increasing use of intelligent design optimization technologies in semiconductor development has also improved manufacturing accuracy and accelerated product development processes. These advancements are helping semiconductor companies reduce redesign expenses, shorten prototyping timelines, and enhance overall product performance, thereby contributing to the continued expansion of the analog semiconductors industry.

In 2025, the general purpose segment accounted for 71.9% share owing to its broad adoption across automotive, industrial, communication, and consumer electronics applications. These components are widely utilized for essential functions related to signal conditioning and power regulation, making them critical for high-volume manufacturing environments. Their flexibility, compatibility with various electronic systems, and cost-effective performance continue to drive widespread demand across multiple industries. Consistent usage across a broad range of applications is expected to support the long-term growth and market dominance of the general purpose segment within the analog semiconductor industry.

The power management ICs segment generated USD 27 billion in 2025. Strong market demand for power management integrated circuits is primarily driven by their critical role in controlling voltage levels, managing battery systems, and distributing power efficiently across electronic devices and industrial systems. These components are extensively used in automotive systems, communication infrastructure, industrial equipment, and consumer electronics because of their high reliability and system optimization capabilities. Increasing focus on energy efficiency and advanced electronic functionality is expected to further accelerate the adoption of power management ICs across high-volume applications, strengthening the segment's position within the global analog semiconductors market.

North America Analog Semiconductors Market held a 26.5% share in 2025. Growth across the regional market is being fueled by substantial investments in transportation electrification, modernization of industrial infrastructure, and the deployment of energy-efficient technologies. Increasing adoption of electric mobility solutions, industrial automation systems, renewable energy infrastructure, and advanced charging networks is driving strong demand for high-performance analog semiconductors components throughout the region. Government initiatives supporting domestic semiconductor production, energy infrastructure enhancement, and expansion of the electric vehicle ecosystem are also contributing to regional market growth.

Key companies operating in the Global Analog Semiconductors Market include Analog Devices, Broadcom, Diodes, Infineon Technologies, MediaTek, Microchip Technology, MinebeaMitsumi, Murata Manufacturing, NXP Semiconductors, ON Semiconductor, Qorvo, Qualcomm Technologies, Renesas Electronics, Semtech, Skyworks Solutions, ST Microelectronics, Taiwan Semiconductor, Taiwan Semiconductor Manufacturing Company, Texas Instruments, and Toshiba. Companies operating in the analog semiconductors industry are implementing several strategic initiatives to strengthen their market presence and maintain competitive advantage. Leading manufacturers are investing heavily in research and development to introduce advanced semiconductor technologies focused on higher efficiency, reduced power consumption, and improved system integration. Many companies are expanding production capacity and upgrading fabrication facilities to meet rising global demand across automotive, industrial, and communication sectors. Strategic collaborations, acquisitions, and partnerships are also being used to broaden technology portfolios and strengthen supply chain capabilities. In addition, businesses are focusing on innovation in power management, signal processing, and intelligent semiconductor design to improve product performance and reduce manufacturing complexity.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Components trends

- 2.2.3 Form factor trends

- 2.2.4 End-use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for electric and hybrid vehicles

- 3.2.1.2 Expansion of industrial automation and smart manufacturing

- 3.2.1.3 Rising need for efficient power management in electronic devices

- 3.2.1.4 Accelerating deployment of 5G and advanced communication infrastructure

- 3.2.1.5 Rising adoption of renewable energy and power conversion systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited availability of skilled analog design engineers

- 3.2.2.2 High sensitivity of analog components to process variations

- 3.2.3 Market opportunities

- 3.2.3.1 Growing integration of analog solutions in advanced driver-assistance and autonomous systems

- 3.2.3.2 Rising adoption of analog components in distributed energy storage systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 General purpose

- 5.3 Application specific

Chapter 6 Market Estimates and Forecast, By Components, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Data converters

- 6.3 Amplifiers

- 6.4 Power management ICs

- 6.5 Interface ICs

- 6.6 Sensors

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Form Factor, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Integrated circuits (ICs)

- 7.3 Discrete components

Chapter 8 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Aerospace & defense

- 8.3 Automotive

- 8.4 Consumer electronics

- 8.5 Healthcare

- 8.6 Industrial

- 8.7 Telecommunications

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Texas Instruments

- 10.1.2 Analog Devices

- 10.1.3 Infineon Technologies AG

- 10.1.4 ST Microelectronics

- 10.1.5 Skyworks Solutions

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Broadcom

- 10.2.1.2 Diodes

- 10.2.1.3 Microchip Technology

- 10.2.1.4 ON Semiconductor

- 10.2.1.5 Qorvo

- 10.2.1.6 Qualcomm Technologies

- 10.2.1.7 Semtech

- 10.2.2 Asia Pacific

- 10.2.2.1 MediaTek

- 10.2.2.2 MinebeaMitsumi

- 10.2.2.3 Murata Manufacturing

- 10.2.2.4 Renesas Electronics

- 10.2.2.5 Taiwan Semiconductor

- 10.2.2.6 Taiwan Semiconductor Manufacturing Company

- 10.2.2.7 Toshiba

- 10.2.3 Europe

- 10.2.3.1 NXP Semiconductors

- 10.2.1 North America