PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044089

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044089

Analog Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

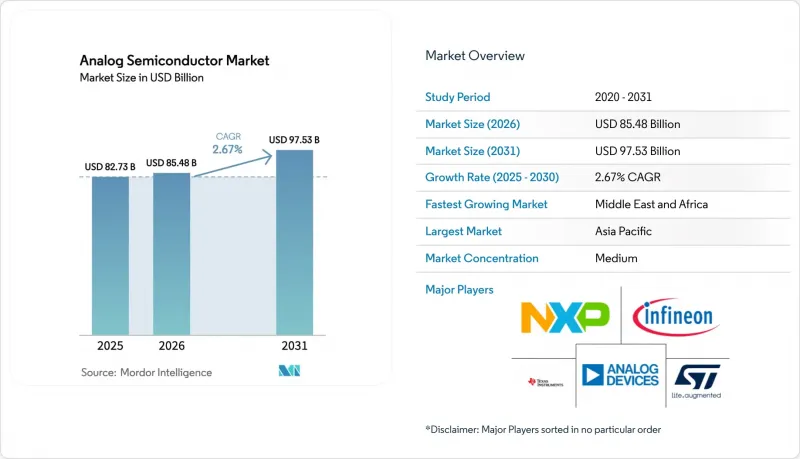

The analog semiconductor market size is expected to increase from USD 85.48 billion in 2026 to USD 97.53 billion by 2031, growing at a CAGR of 2.67% over 2026-2031. Volume shipments will climb from 244.73 billion units in 2026 to 342.88 billion units by 2031, a 6.98% CAGR that widens the gap between unit and revenue growth as price pressure persists in commodity categories. Application-specific analog ICs retained a sizeable revenue base in 2025, yet rising standardization in edge-computing and factory-automation hardware is steering many new designs toward general-purpose parts, tightening competitive dynamics across catalog portfolios. Asia-Pacific manufacturers account for almost half of global demand, propelled by gallium-nitride fast-charging ecosystems, while defense-driven projects in the Middle East create premium opportunities for radiation-hardened front-ends. Simultaneously, 300 mm fab ramps in Texas and Dresden aim to relieve long-standing wafer bottlenecks, but near-term allocation risk remains for fabless suppliers that depend on external foundries.

Global Analog Semiconductor Market Trends and Insights

Proliferation Of Fast-Charging Power Adapters In Asian Smartphone Ecosystems

Asian handset makers standardized USB-PD 3.1 and proprietary 65 W-240 W fast-charge protocols in 2025, a shift that required gallium-nitride power management ICs with higher switching frequencies and reduced thermal budgets. Navitas shipped more than 100 million GaN devices into these adapters, while Renesas integrated USB-C controllers and GaN gate drivers to cut external components by one-fifth. Local tier-two OEMs quickly embraced the lower bill-of-materials cost, accelerating design cycles and reinforcing Asia-Pacific's dominance within the analog semiconductor market.

Industrial IoT Adoption Elevating Demand For High-Precision Data Converters In North America

Factories across the United States deployed over 15 million IoT sensor nodes in 2025, each calling for 16-bit-plus ADCs with microvolt-level noise floors. Analog Devices' multisensor front-ends trimmed discrete counts by 40%, and Texas Instruments delivered delta-sigma converters supporting 40 kHz sampling for vibration analytics. The resulting demand uplift bolsters catalog revenues and keeps high-accuracy converters at premium price points within the analog semiconductor market.

300 mm Fab Capacity Bottlenecks Limiting PMIC Supply

Texas Instruments and GlobalFoundries added new lines, yet TSMC still allocates most 300 mm tools to advanced logic, leaving analog runs on legacy nodes oversubscribed. Lead times stretched beyond 20 weeks in late 2025 and automotive programs felt acute shortages as integrated device manufacturers diverted wafers to in-house needs. The tight capacity continues to restrain output of high-volume power-management ICs, tempering near-term expansion in the analog semiconductor market.

Other drivers and restraints analyzed in the detailed report include:

- Roll-Out Of 5G Infrastructure Amplifying RF Analog IC Demand In East Asia

- AI-Accelerated Edge Devices Requiring Ultra-Low-Power Data-Acquisition ICs

- Volatility In Analog Wafer-Foundry Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General-purpose ICs accounted for modest revenue in 2025 yet are projected to lead growth at a 6.52% CAGR, reflecting their fit with modular hardware platforms that dominate industrial automation. The analog semiconductor market size tied to these catalog amplifiers and comparators will expand as OEMs adopt off-the-shelf parts to shave months from development schedules.

Application-specific designs, while still responsible for 45.71% revenue in 2025, face slower gains as custom ASIC projects require longer validation windows. Automotive battery-management ASICs and 5G RF front-ends illustrate how high-volume sectors will keep bespoke analog relevant, but their share of the analog semiconductor market will gradually normalize as configurable catalog alternatives improve performance envelopes. Industrial ASICs address harsh environments, with onsemi's Treo platform integrating isolated gate drivers and current sensing for silicon carbide traction inverters

Operational amplifiers are forecast to post a 5.83% CAGR, driven by precision sensing in medical and industrial endpoints. Premium amplifiers with microvolt offset voltages sustain higher average selling prices, preserving value contribution within the analog semiconductor market size for signal-conditioning devices. Analog Devices' AD7380, a 16-bit successive-approximation ADC with integrated voltage reference, eliminates external precision resistors and reduces printed circuit board area by 30%.

Power-management parts, holding 29.83% share in 2025, confront steeper price erosion because smartphone and notebook OEMs wield greater purchasing leverage. Conversely, high-resolution converters and rugged interface transceivers benefit from tighter electromagnetic-compatibility standards, helping stabilize margins despite rising wafer costs. Diodes and transistors serve niche roles in electrostatic discharge protection and load switching, yet discrete shipments declined 5% year-over-year in 2025 as integrated solutions gained share.

The Analog Semiconductor Market Report is Segmented by Device Type (General Purpose Analog IC and Application-Specific Analog IC), Component (Resistors, Capacitors, Inductors, and More), Wafer Size (200mm, 300mm, and More), End-User Industry (Consumer Electronics, IT and Telecom, Automotive and Transportation, and More), and Geography. The Market Forecasts are Provided in Terms of Both Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific remains the center of gravity for the analog semiconductor market, accounting for 45.72% of revenue in 2025. Supply ecosystems in China, Japan, and South Korea absorb high-volume analog for smartphones, automotive power modules, and 5G radios. Government incentives such as China's CNY 344 billion (USD 47 billion) National IC Fund and Japan's equipment tax credits underpin local capacity expansions, reinforcing regional self-reliance. India's semiconductor incentive program attracted proposals for analog fabs, yet regulatory approvals extended beyond 24 months, delaying capacity additions until 2027.

The Middle East is projected to chart the fastest CAGR of 7.02% through 2031 as defense agencies modernize avionics and satellite payloads. United Arab Emirates and Saudi Arabia initiatives funnel capital into design centers that specialize in radiation-tolerant front-ends, carving out a premium sub-segment within the analog semiconductor market.

North America accounts for roughly one-quarter of global revenue, with CHIPS Act grants totaling USD 39 billion catalyzing domestic wafer production. Europe follows at nearly one-fifth share, supported by the EUR 43 billion (USD 46.9 billion) EU Chips Act, while South America and Africa collectively represent less than 10% yet display selective uptake in automotive and off-grid energy systems.

List of Companies Covered in this Report:

- Texas Instruments Inc.

- Analog Devices Inc.

- STMicroelectronics N.V.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- onsemi

- Renesas Electronics Corp.

- Microchip Technology Inc.

- Rohm Co., Ltd.

- Skyworks Solutions Inc.

- Cirrus Logic Inc.

- Silicon Laboratories Inc.

- Monolithic Power Systems Inc.

- Diodes Incorporated

- Vicor Corp.

- Power Integrations Inc.

- Semtech Corp.

- Qorvo Inc.

- Allegro MicroSystems Inc.

- Vishay Intertechnology Inc.

- Maxim Integrated Products Inc.

- Richtek Technology Corp.

- Broadcom Inc.

- Tower Semiconductor Ltd.

- AnalogicTech Corp.

- Nordic Semiconductor ASA (Analog Front-End ICs)

- Alpha & Omega Semiconductor Ltd.

- Silergy Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification Surge in 48 V Mild-Hybrid Vehicles Across Europe

- 4.2.2 Proliferation of Fast-Charging Power Adapters in Asian Smartphone Ecosystems

- 4.2.3 Industrial IoT Adoption Elevating Demand for High-Precision Data Converters in North America

- 4.2.4 Roll-Out of 5 G Infrastructure Amplifying RF Analog IC Demand in East Asia

- 4.2.5 Escalating Defense Modernization Driving Radiation-Hardened Analog Procurement in the Middle East

- 4.2.6 AI-Accelerated Edge Devices Requiring Ultra-Low-Power Data-Acquisition ICs

- 4.3 Market Restraints

- 4.3.1 300 mm Fab Capacity Bottlenecks Limiting PMIC Supply

- 4.3.2 Volatility in Analog Wafer-Foundry Pricing

- 4.3.3 Design-In Cycles Stretching Time-to-Revenue for Niche Automotive ASICs

- 4.3.4 Counterfeit Passive Components Undermining Reliability in South-East Asia

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Device Type (Value and Volume)

- 5.1.1 General Purpose Analog IC

- 5.1.1.1 Amplifiers and Comparators

- 5.1.1.2 Interface

- 5.1.1.3 Power Management

- 5.1.1.4 Signal Conversion

- 5.1.2 Application-Specific Analog IC

- 5.1.2.1 Automotive

- 5.1.2.2 Communications

- 5.1.2.3 Computer

- 5.1.2.4 Consumer

- 5.1.2.5 Industrial

- 5.1.1 General Purpose Analog IC

- 5.2 By Component (Value)

- 5.2.1 Resistors

- 5.2.2 Capacitors

- 5.2.3 Inductors

- 5.2.4 Diodes

- 5.2.5 Transistors

- 5.2.6 Operational Amplifiers

- 5.3 By Wafer Size (Value)

- 5.3.1 200 mm

- 5.3.2 300 mm

- 5.3.3 Other Sizes

- 5.4 By End-User Industry (Value)

- 5.4.1 Consumer Electronics

- 5.4.2 IT and Telecom

- 5.4.3 Automotive and Transportation

- 5.4.4 Industrial and Manufacturing

- 5.4.5 Healthcare Devices

- 5.4.6 Aerospace and Defense

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Texas Instruments Inc.

- 6.4.2 Analog Devices Inc.

- 6.4.3 STMicroelectronics N.V.

- 6.4.4 Infineon Technologies AG

- 6.4.5 NXP Semiconductors N.V.

- 6.4.6 onsemi

- 6.4.7 Renesas Electronics Corp.

- 6.4.8 Microchip Technology Inc.

- 6.4.9 Rohm Co., Ltd.

- 6.4.10 Skyworks Solutions Inc.

- 6.4.11 Cirrus Logic Inc.

- 6.4.12 Silicon Laboratories Inc.

- 6.4.13 Monolithic Power Systems Inc.

- 6.4.14 Diodes Incorporated

- 6.4.15 Vicor Corp.

- 6.4.16 Power Integrations Inc.

- 6.4.17 Semtech Corp.

- 6.4.18 Qorvo Inc.

- 6.4.19 Allegro MicroSystems Inc.

- 6.4.20 Vishay Intertechnology Inc.

- 6.4.21 Maxim Integrated Products Inc.

- 6.4.22 Richtek Technology Corp.

- 6.4.23 Broadcom Inc.

- 6.4.24 Tower Semiconductor Ltd.

- 6.4.25 AnalogicTech Corp.

- 6.4.26 Nordic Semiconductor ASA (Analog Front-End ICs)

- 6.4.27 Alpha & Omega Semiconductor Ltd.

- 6.4.28 Silergy Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment