PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045738

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045738

Sodium Chlorite Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

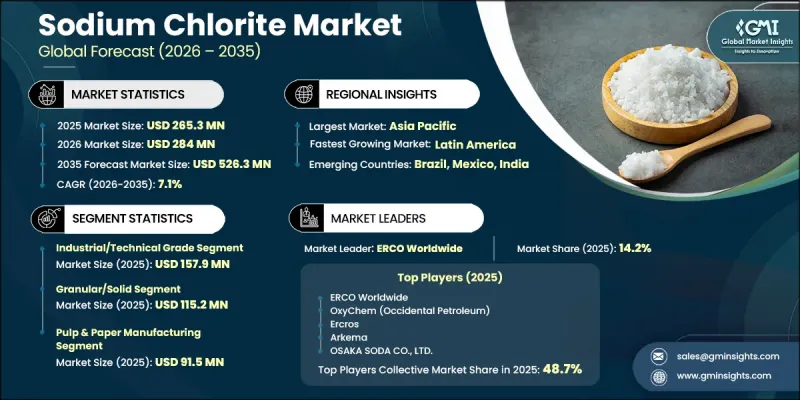

The Global Sodium Chlorite Market was valued at USD 265.3 million in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 526.3 million by 2035.

The market is expanding due to rising demand for efficient oxidation and disinfection solutions across industrial processing and water treatment applications. Sodium chlorite is produced through the reaction of sodium hydroxide and chlorine dioxide, resulting in a white crystalline compound or aqueous solution with strong oxidizing functionality. Its bleaching efficiency and antimicrobial performance make it an important material across industries that require controlled oxidation capabilities. The compound is widely utilized in pulp and paper processing, textile manufacturing, and water purification systems because of its ability to generate chlorine dioxide effectively. Sodium chlorite is also increasingly preferred in odor control and microbial treatment applications due to its stable disinfection properties and lower formation of harmful byproducts compared to conventional alternatives. Advancements in production technologies are further improving market growth, as manufacturers continue to refine synthesis and purification methods to enhance concentration control and product stability. The adoption of electrochemical production systems and advanced chemical reduction techniques is enabling suppliers to improve consistency, operational efficiency, and product quality across multiple end-use industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $265.3 Million |

| Forecast Value | $526.3 Million |

| CAGR | 7.1% |

The industrial and technical grade segment accounted for USD 157.9 million in 2025. This segment continues to lead due to extensive use in pulp and paper bleaching operations, where sodium chlorite is valued for its high oxidizing efficiency and cost-effectiveness in large-scale processing environments. Industrial-grade products deliver the performance standards required for continuous bleaching applications while supporting brightness and quality requirements across paper manufacturing and textile treatment facilities. Improvements in production systems are also helping manufacturers maintain consistent product quality for demanding industrial operations worldwide.

The granular and solid form segment reached USD 115.2 million in 2025. This form continues to dominate due to its enhanced storage stability and transportation advantages, making it highly suitable for bulk chemical distribution and extended inventory management. Granular sodium chlorite provides a longer shelf life than liquid alternatives and allows industrial users to prepare customized solution concentrations depending on operational requirements. Water treatment facilities and manufacturing plants prefer solid formulations because they support accurate dosing control while minimizing concerns related to concentration degradation over time.

North America Sodium Chlorite Market is expected to increase from USD 70.3 million in 2025 to USD 135.7 million by 2035. Regional growth is being supported by increasing demand for reliable disinfection chemicals within water treatment infrastructure and continued adoption of environmentally improved bleaching technologies across the pulp and paper sector. Expanding implementation of advanced chlorine dioxide generation systems, along with supportive regulatory frameworks focused on safer disinfection methods, is further strengthening market growth across the region.

Major companies operating in the Global Sodium Chlorite Industry include Arkema, Occidental Petroleum Corporation (OxyChem), ERCO Worldwide, Carlit Holdings Co., Ltd. (Japan Carlit), OSAKA SODA CO., LTD., Merck KGaA (MilliporeSigma / Sigma-Aldrich), Alfa Aesar (Thermo Scientific Chemicals), Ercros, Fengchen Group Co., Ltd., Dongying Shengya Chemical Co., Ltd., Gaomi Fuyihe Chem Co., Ltd., and Shandong Gaomi Gaoyuan Chemical Industry Co., Ltd. Companies in the sodium chlorite market are focusing on expanding production efficiency through advanced synthesis technologies and process optimization initiatives. Manufacturers are investing in purification systems and automated quality monitoring to improve concentration consistency and product stability. Strategic partnerships with water treatment operators and pulp processing companies are helping strengthen long-term supply agreements and market penetration. Businesses are also prioritizing environmentally responsible production methods to align with evolving regulatory standards and sustainability goals. Capacity expansion projects and regional distribution network development are improving product accessibility across high-demand markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Grade

- 2.2.2 Form

- 2.2.3 End use Industry

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By grade

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Grade, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Industrial/Technical Grade

- 5.3 Food Grade

- 5.4 Pharmaceutical Grade

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Granular/Solid

- 6.3 Liquid

- 6.4 Powder

Chapter 7 Market Estimates and Forecast, By End-use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Pulp & Paper Manufacturing

- 7.2.1 Kraft Pulp Mills

- 7.2.2 Mechanical Pulp Mills

- 7.2.3 Recycled Paper Production

- 7.3 Textile Manufacturing

- 7.3.1 Cotton & Natural Fiber Processing

- 7.3.2 Synthetic Fiber Processing

- 7.4 Water Utilities

- 7.4.1 Municipal Water Treatment Plants

- 7.4.2 Private Water Utilities

- 7.5 Food Processing & Beverage

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Alfa Aesar (Thermo Scientific Chemicals)

- 9.2 Arkema

- 9.3 Carlit Holdings Co., Ltd. (Japan Carlit)

- 9.4 Ercros

- 9.5 ERCO Worldwide

- 9.6 Fengchen Group Co.,Ltd

- 9.7 Dongying Shengya Chemical Co., Ltd.

- 9.8 Gaomi Fuyihe Chem Co., Ltd.

- 9.9 Merck KGaA (MilliporeSigma / Sigma-Aldrich)

- 9.10 Occidental Petroleum Corporation (OxyChem)

- 9.11 OSAKA SODA CO., LTD.

- 9.12 Shandong Gaomi Gaoyuan Chemical Industry Co.,Ltd