PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045746

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045746

Industrial Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

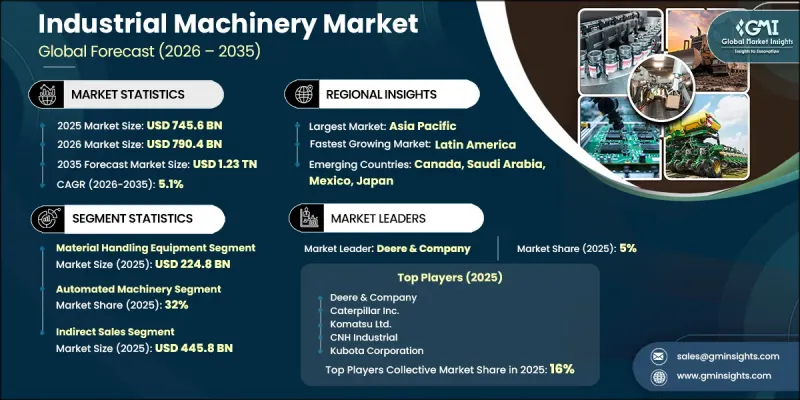

The Global Industrial Machinery Market was valued at USD 745.6 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 1.23 trillion by 2035.

Market growth is influenced by the accelerating shift toward automation across manufacturing and production environments. Industries are increasingly deploying advanced machinery to improve operational precision, enhance production speed, and reduce overall manufacturing costs. Demand for automated systems is rising as companies aim to minimize dependence on manual labor and reduce production errors across high-volume industrial operations. Sectors such as automotive, electronics, pharmaceuticals, and food processing are increasingly integrating robotics, CNC systems, and automated material handling solutions to modernize their production lines. Rising labor costs and persistent shortages of skilled workers are further encouraging end users to transition from conventional equipment to advanced automated machinery. The adoption of Industry 4.0 technologies is also reshaping the market, enabling smart, connected machines capable of real-time performance monitoring, predictive maintenance, and energy optimization. These capabilities are increasingly viewed as essential for reducing downtime and improving cost efficiency. As a result, purchasing decisions are now driven not only by machine capacity but also by digital integration, long-term operational efficiency, and compatibility with existing industrial systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $745.6 Billion |

| Forecast Value | $1.23 Trillion |

| CAGR | 5.1% |

The material handling equipment segment generated USD 224.8 billion in 2025, securing a leading position in the market. This category includes systems designed for transporting, storing, protecting, and managing materials across production plants, warehouses, logistics centers, and construction environments. Equipment such as forklifts, cranes, conveyors, pallet jacks, hoists, automated storage and retrieval systems, and industrial lift trucks plays a critical role in improving workflow efficiency, workplace safety, and material movement speed across industrial operations.

The automated machinery segment accounted for a 32% share in 2025, making it the dominant technology category. Automated systems are designed to execute multiple industrial tasks with minimal human involvement, using advanced technologies such as robotics, sensors, and software-based control systems. Their ability to enhance production accuracy, maintain consistent output quality, and improve operational efficiency has led to widespread replacement of manual systems, particularly in high-speed and precision-driven environments. Common applications include robotic assembly units, CNC machines, automated production lines, and intelligent systems used in packaging, processing, and material handling operations.

U.S. Industrial Machinery Market accounted for a 77.9% share in 2025, reaching USD 91.9 billion. Growth in the country is driven by strong investments in automation technologies, energy-efficient machinery, and advanced manufacturing systems aimed at improving productivity and operational modernization. High demand from automotive, aerospace, construction, food processing, and electronics industries continues to support equipment adoption. Additionally, manufacturing reshoring initiatives and federal infrastructure development programs are further reinforcing demand for heavy machinery, smart production systems, and advanced material handling equipment across the country.

Key players operating in the Global Industrial Machinery Industry include Caterpillar Inc., Deere & Company, Komatsu Ltd., CNH Industrial NV, Volvo Construction Equipment, Liebherr Group, Atlas Copco AB, JCB, Hitachi Construction Machinery, Kubota Corporation, Sandvik AB, Ingersoll Rand Inc., Manitowoc Company, Honeywell International, ASML Holding NV, Metso, AGCO Corporation, Terex Corporation, Alfa Laval AB, GEA Group AG, and Illinois Tool Works Inc. Companies in the industrial machinery market are focusing on expanding automation and smart manufacturing capabilities by integrating advanced digital technologies into equipment design. They are investing heavily in research and development to improve machine efficiency, durability, and precision. Strategic partnerships with industrial end users are helping manufacturers tailor solutions to specific production requirements. Firms are also strengthening global distribution and service networks to enhance customer support and reduce downtime. A growing emphasis is placed on predictive maintenance solutions and IoT-enabled machinery to improve lifecycle performance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Operation

- 2.2.4 Application

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Industrial automation & industry 4.0

- 3.2.1.2 Infrastructure & construction spending

- 3.2.1.3 Energy transition & sustainability focus

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Supply chain disruptions

- 3.2.2.2 Regulatory & compliance burden

- 3.2.3 Opportunities

- 3.2.3.1 Smart & connected machinery

- 3.2.3.2 Sustainability-driven innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory framework

- 3.5.1 Safety standards & compliance (ISO, OSHA, CE)

- 3.5.2 Environmental regulations (emissions, noise)

- 3.5.3 Import/export regulations & tariffs

- 3.5.4 Labor & workplace safety laws

- 3.5.5 Regional regulatory variations

- 3.5.6 Upcoming regulatory changes (2026-2035)

- 3.6 Pricing analysis

- 3.6.1 Historical price trend analysis

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6.3 Regional price variations

- 3.6.4 Impact of raw material costs on pricing

- 3.7 Trade data analysis (driven by paid data base) (8479)

- 3.7.1 Import/export volume & value trends

- 3.7.2 Key trade corridors & tariff impact

- 3.7.3 Top exporting countries

- 3.7.4 Top importing countries

- 3.7.5 Trade balance analysis by region

- 3.8 Impact of AI & generative AI on the market

- 3.8.1 AI-driven disruption of existing business models

- 3.8.2 GenAI use cases & adoption roadmap by segment

- 3.8.3 Risks, limitations & regulatory considerations

- 3.8.4 Predictive maintenance & AI integration

- 3.8.5 Autonomous machinery development

- 3.9 Capacity & production landscape (driven by primary research)

- 3.9.1 Installed capacity by region & key producer

- 3.9.2 Capacity utilization rates & expansion pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Agricultural machinery

- 5.2.1 Tractors

- 5.2.2 Harvesters & combines

- 5.2.3 Planting & seeding equipment

- 5.2.4 Irrigation systems

- 5.2.5 Other agricultural machinery

- 5.3 Construction & earth-moving equipment

- 5.3.1 Excavators

- 5.3.2 Bulldozers

- 5.3.3 Loaders

- 5.3.4 Cranes

- 5.3.5 Dump trucks

- 5.3.6 Graders & scrapers

- 5.3.7 Other construction equipment

- 5.4 Material handling equipment

- 5.4.1 Forklifts

- 5.4.2 Conveyors

- 5.4.3 Hoists & cranes

- 5.4.4 Automated storage & retrieval systems (as/rs)

- 5.4.5 Palletizers

- 5.5 Processing machinery

- 5.5.1 Food processing equipment

- 5.5.2 Plastics processing machinery

- 5.5.3 Metalworking & metal forming machines

- 5.5.4 Woodworking machinery

- 5.5.5 Chemical processing equipment

- 5.6 Packaging machinery

- 5.6.1 Filling machines

- 5.6.2 Palletizing machines

- 5.6.3 Labelling machines

- 5.6.4 Wrapping machines

- 5.6.5 Other packaging equipment

- 5.7 Industrial robots & automation cells

- 5.7.1 Articulated robots

- 5.7.2 Scara robots

- 5.7.3 Collaborative robots (cobots)

- 5.7.4 Cartesian/gantry robots

- 5.7.5 Automated manufacturing cells

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Operation, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automated machinery

- 6.3 Semi-automated machinery

- 6.4 Manual machinery

- 6.5 Robotic machinery

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Construction & mining

- 7.3 Agriculture

- 7.4 Food & beverage processing

- 7.5 Automotive manufacturing

- 7.6 Pharmaceuticals

- 7.7 Chemical processing

- 7.8 Packaging operations

- 7.9 Semiconductor manufacturing

- 7.10 Metal fabrication

- 7.11 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Caterpillar Inc.

- 10.1.2 Deere & Company

- 10.1.3 Komatsu Ltd.

- 10.1.4 CNH Industrial NV

- 10.1.5 Volvo Construction Equipment

- 10.1.6 Liebherr Group

- 10.1.7 Atlas Copco AB

- 10.2 Regional players

- 10.2.1 JCB

- 10.2.2 Hitachi Construction Machinery

- 10.2.3 Kubota Corporation

- 10.2.4 Sandvik AB

- 10.2.5 Ingersoll Rand Inc

- 10.2.6 Manitowoc Company

- 10.2.7 Honeywell International

- 10.3 Emerging players

- 10.3.1 ASML Holding NV

- 10.3.2 Metso

- 10.3.3 AGCO Corporation

- 10.3.4 Terex Corporation

- 10.3.5 Alfa Laval AB

- 10.3.6 GEA Group AG

- 10.3.7 Illinois Tool Works Inc