PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045753

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045753

1-Hexene Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

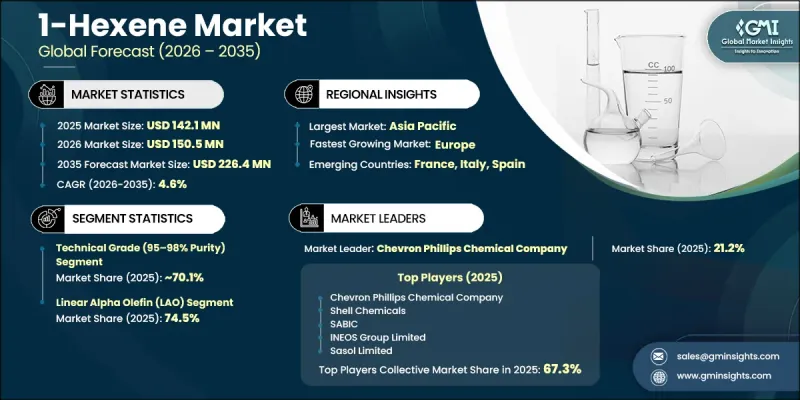

The Global 1-Hexene Market was valued at USD 142.1 million in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 226.4 million by 2035.

The 1-hexene industry continues to witness stable growth due to its extensive use as a key comonomer in the production of high-density polyethylene (HDPE) and linear low-density polyethylene (LLDPE). These polyethylene materials are widely utilized across multiple industrial sectors for manufacturing packaging products, pipes, industrial containers, and various plastic components. Rising demand from the automotive and construction industries for lightweight and durable materials is further supporting market expansion, as 1-hexene improves the strength, flexibility, and performance characteristics of polyethylene-based products. Market growth is also influenced by fluctuations in raw material availability and pricing, particularly because 1-hexene production depends heavily on ethylene derived from crude oil and natural gas sources. Variations in feedstock costs, geopolitical uncertainties, and supply chain disruptions continue to impact overall production economics. At the same time, increasing focus on sustainable manufacturing practices and advancements in polymer technologies are encouraging the development of bio-based alternatives and higher-performance polyethylene products, supporting long-term growth opportunities within the global 1-hexene market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $142.1 Million |

| Forecast Value | $226.4 Million |

| CAGR | 4.6% |

The technical grade segment with 95-98% purity accounted for 70.1% share in 2025. This segment continues to maintain strong demand due to its widespread utilization across industrial manufacturing operations, chemical processing activities, and solvent formulation applications where ultra-high purity specifications are not essential. Its cost-effectiveness and suitability for large-scale industrial usage continue to support growth across multiple end-use industries.

The linear alpha olefin (LAO) segment held a share of 74.5% in 2025. Strong market preference for LAO-based 1-hexene products is attributed to their superior product consistency, higher purity levels, and enhanced performance in downstream chemical processing and polymerization applications. The linear molecular structure of LAO supports improved reactivity and processing efficiency, making it highly suitable for producing high-quality polymers and industrial chemical products. Expanding utilization across plastic manufacturing, surfactant production, and industrial chemical applications continues to strengthen the segment's market leadership.

North America 1-Hexene Market was valued at USD 44.4 million in 2025 and is anticipated to grow at a CAGR of 4.7% between 2026 and 2035. Regional market growth is being supported by strong chemical manufacturing activities and increasing export demand across the United States and Canada. Rising consumption of industrial coatings, adhesives, and specialty chemical products is contributing to expanding demand for 1-hexene throughout the region. In addition, increasing investments in sustainable chemical processing technologies and innovation-driven manufacturing practices are positively influencing market development across North America.

Major companies operating in the Global 1-Hexene Market include Chevron Phillips Chemical Company, SABIC, Shell Chemicals, INEOS Group Limited, Sasol Limited, Qatar Chemical Company (Q-Chem), Idemitsu Kosan Co., Ltd., SIBUR Holding, Sinopec, and PetroChina. Companies operating in the 1-hexene market are adopting multiple strategies to strengthen their market position and improve long-term competitiveness. Leading manufacturers are increasing investments in research and development activities to enhance production efficiency, improve product purity, and support sustainable chemical manufacturing practices. Many companies are also focusing on expanding production capacities and strengthening supply chain networks to address rising global demand and minimize raw material supply disruptions. Strategic collaborations, joint ventures, and partnerships with downstream polymer manufacturers are helping businesses expand their market reach and improve customer relationships. In addition, organizations are prioritizing the development of bio-based and environmentally sustainable 1-hexene solutions to align with evolving environmental regulations and sustainability goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Purity

- 2.2.3 Product type

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.2.6 End use industry

- 2.2.7 Application

- 2.2.8 End use industry

- 2.2.9 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for high-performance polyethylene in packaging applications

- 3.2.1.2 Expansion of downstream petrochemical capacities in Asia Pacific

- 3.2.1.3 Lightweighting trend in packaging & automotive industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in raw material prices (ethylene & crude oil)

- 3.2.2.2 Oversupply concerns & weak demand in certain regions

- 3.2.3 Market opportunities

- 3.2.3.1 Diversification into specialty chemicals & high-performance polymers

- 3.2.3.2 Emerging applications in agriculture & advanced packaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Purity, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Technical grade (95-98% purity)

- 5.3 Pure grade (≥99% purity)

Chapter 6 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Linear alpha olefin (LAO)

- 6.3 Branched olefin

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Polyethylene production

- 7.3 Heptanol production

- 7.4 Flavors

- 7.5 Perfumes

- 7.6 Dyes

- 7.7 Resins

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Chemical industry

- 9.3 Plastics industry

- 9.4 Packaging industry

- 9.4.1 Flexible packaging

- 9.4.2 Rigid packaging

- 9.4.3 E-commerce & logistics packaging

- 9.5 Construction industry

- 9.6 Consumer goods

- 9.6.1 Household products & appliances

- 9.6.2 Personal care & cosmetics

- 9.6.3 Toys & recreational products

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Chevron Phillips Chemical Company

- 11.2 SABIC

- 11.3 Shell Chemicals

- 11.4 INEOS Group Limited

- 11.5 Sasol Limited

- 11.6 Qatar Chemical Company (Q-Chem)

- 11.7 Idemitsu Kosan Co., Ltd.

- 11.8 SIBUR Holding

- 11.9 Sinopec

- 11.10 PetroChina