PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045781

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045781

Bottled Water Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

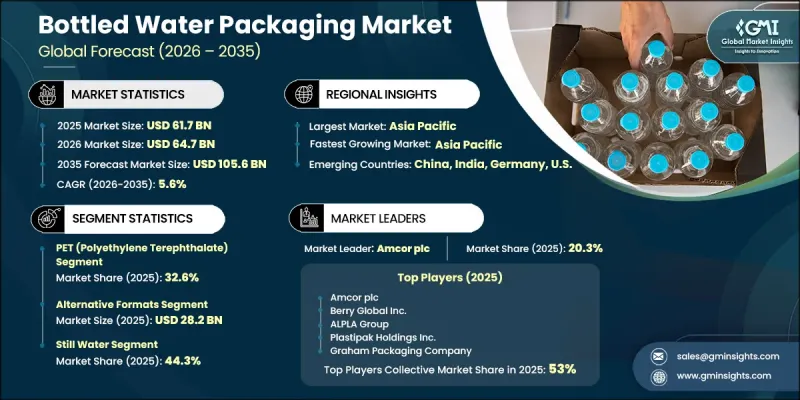

The Global Bottled Water Packaging Market was valued at USD 61.7 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 105.6 billion by 2035.

Market growth is fueled by rising consumption of packaged drinking water as consumers increasingly prioritize health, hygiene, and safe hydration solutions. Rapid urbanization and changing lifestyles are also contributing to higher demand for portable and convenient packaging formats suitable for on-the-go consumption. Expanding retail infrastructure, including organized retail stores and convenience distribution channels, continues to improve product accessibility and strengthen packaging demand worldwide. The market is also benefiting from the growing presence of private-label manufacturers and regional bottled water brands, which are increasing packaging volumes across multiple product categories. Continuous advancements in packaging efficiency and material optimization are further supporting industry expansion by improving production capabilities while reducing material usage and environmental impact. Lightweight and cost-effective packaging solutions are becoming increasingly important as manufacturers focus on sustainability goals and operational efficiency. The bottled water packaging industry continues to evolve steadily as consumer preference for hygienic packaged beverages and practical packaging formats strengthens demand across both developed and emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $61.7 Billion |

| Forecast Value | $105.6 Billion |

| CAGR | 5.6% |

The PET (polyethylene terephthalate) segment held a 32.6% share in 2025. PET packaging continues to maintain strong demand due to its lightweight structure, cost-effectiveness, and excellent barrier performance. The material supports high-volume manufacturing, efficient transportation, and compatibility with established recycling systems, making it the preferred packaging solution for bottled water products across mass-market retail and institutional applications. Increasing emphasis on lightweight packaging and recyclable materials is further strengthening the adoption of PET bottles throughout the global bottled water packaging industry.

The single-use bottles segment is expected to grow at a CAGR of 6% during 2026-2035. Market growth within this segment is driven by increasing demand for portable beverage packaging solutions that align with modern urban lifestyles and rising impulse purchasing behavior. Single-use bottle formats offer convenience, easy handling, and compatibility with fast-moving retail environments, making them highly suitable for both premium and mainstream bottled water products. Growing consumption of packaged beverages during travel, work, and outdoor activities continues to support strong demand for single-use bottled water packaging globally.

North America Bottled Water Packaging Market accounted for 31.4% share in 2025. The regional market continues to grow due to strong consumer preference for reliable and hygienic packaged drinking water solutions. Well-established retail distribution systems and high bottled water penetration across urban and suburban populations are supporting consistent demand for primary packaging products, including PET bottles, closures, and multipack solutions. Increasing focus on convenience, product safety, and sustainable packaging technologies is also contributing to market growth throughout North America.

Major companies operating in the Global Bottled Water Packaging Market include Amcor plc, Berry Global Inc., ALPLA Group, Plastipak Holdings Inc., Graham Packaging Company, Gerresheimer AG, O-I Glass Inc., Ardagh Group, Verallia, Ball Corporation, Crown Holdings Inc., Silgan Holdings Inc., RPC Group, RETAL Industries Ltd., and Resilux NV. Companies operating in the bottled water packaging market are adopting several strategic initiatives to strengthen their market position and expand their global footprint. Manufacturers are investing heavily in sustainable packaging technologies, including lightweight bottle designs, recyclable materials, and reduced plastic usage to meet evolving environmental regulations and consumer preferences. Many companies are also expanding production capacities and improving supply chain efficiency to address rising global demand for bottled water packaging solutions. Strategic mergers, acquisitions, and partnerships are helping businesses broaden their geographic reach and diversify product portfolios. In addition, packaging manufacturers are focusing on innovation in barrier technologies, packaging durability, and eco-friendly materials to improve product performance and sustainability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging format trends

- 2.2.3 Bottle size trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumption of bottled water as a hygiene and health necessity

- 3.2.1.2 Urbanization and on-the-go consumption patterns

- 3.2.1.3 Expansion of retail and convenience store networks

- 3.2.1.4 Strong penetration of private-label and regional water brands

- 3.2.1.5 Continuous innovation in lightweight and cost-efficient packaging formats

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising regulatory and environmental pressure on plastic packaging

- 3.2.2.2 Volatility in raw material and resin prices

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of alternative and refill-enabled packaging systems

- 3.2.3.2 Growth of institutional and bulk packaged water formats

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 PET (polyethylene terephthalate)

- 5.3 HDPE (high-density polyethylene)

- 5.4 Glass

- 5.5 Aluminum

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Packaging Format, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Single-use bottles

- 6.3 Returnable large jugs

- 6.4 Cans

- 6.5 Alternative formats

Chapter 7 Market Estimates and Forecast, By Bottle Size, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Small format (less than 330 ml)

- 7.3 Single-serve (330 ml to 500 ml)

- 7.4 Medium format (501 ml to 1 liter)

- 7.5 Family size (1.1 to 2 liters)

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Still water

- 8.3 Sparkling water

- 8.4 Value-added water

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Amcor plc

- 10.1.2 Berry Global Inc.

- 10.1.3 ALPLA Group

- 10.1.4 Plastipak Holdings Inc.

- 10.1.5 Graham Packaging Company

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 O-I Glass Inc.

- 10.2.1.2 Ball Corporation

- 10.2.1.3 Crown Holdings Inc.

- 10.2.1.4 Silgan Holdings Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 RETAL Industries Ltd.

- 10.2.3 Europe

- 10.2.3.1 Gerresheimer AG

- 10.2.3.2 Ardagh Group

- 10.2.3.3 Verallia

- 10.2.3.4 RPC Group (part of Berry Global)

- 10.2.3.5 Resilux NV

- 10.2.1 North America