PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045791

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045791

Food Storage Container Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

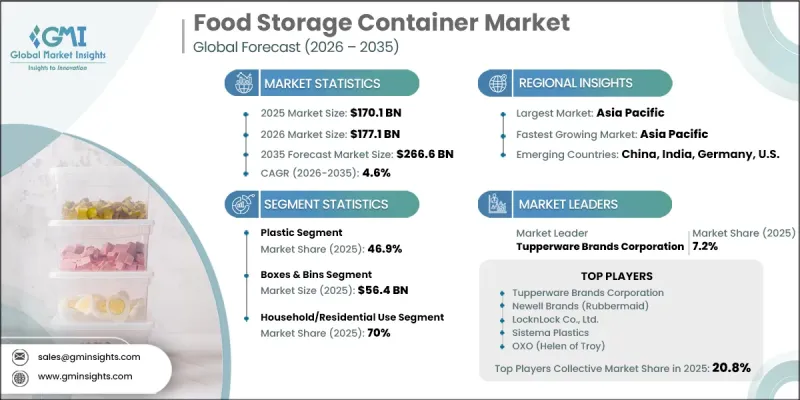

The Global Food Storage Container Market was valued at USD 170.1 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 266.6 billion by 2035.

Rising consumption of packaged meals, convenience foods, and ready-to-eat products is significantly contributing to market expansion worldwide. Increasing reliance on efficient food preservation solutions across residential and commercial sectors is creating strong demand for durable and high-performance storage containers. The market is also benefiting from growing awareness regarding food safety, hygiene, and waste reduction. Consumers are increasingly favoring premium-quality containers that help extend shelf life and maintain freshness. In addition, sustainability initiatives and circular economy policies are encouraging manufacturers to develop reusable, recyclable, and eco-conscious storage solutions. Growing adoption of multifunctional food containers that support storage, reheating, and serving applications is further strengthening industry growth. Advancements in product design, leak-proof technology, stackable formats, and microwave-safe materials are also improving consumer convenience and driving product demand across households, restaurants, and foodservice establishments globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $170.1 Billion |

| Forecast Value | $266.6 Billion |

| CAGR | 4.6% |

The glass segment is anticipated to record a CAGR of 5.9% through 2035, supported by increasing consumer preference for sustainable, non-toxic, and odor-resistant food storage solutions. Glass-based containers provide enhanced durability, superior hygiene, and compatibility with microwave and oven applications, making them highly attractive among consumers seeking long-lasting kitchen products. Rising demand for environmentally friendly and premium storage materials continues to accelerate adoption across residential and commercial kitchens.

The jars and canisters segment is forecast to grow at a CAGR of 5.8% during 2026-2035. Demand for these products is increasing as consumers prioritize organized kitchen spaces and convenient pantry storage solutions. Jars and canisters improve visibility, accessibility, and storage efficiency for dry food items while complementing modern kitchen aesthetics. Growing interest in home organization and premium kitchen accessories is further contributing to segment growth.

North America Food Storage Container Market accounted for 27.8% share in 2025. Strong demand for packaged, frozen, and bulk food products across the region continues to support market expansion. The presence of established retail networks, changing eating habits, and increasing preference for durable and large-capacity storage solutions are positively influencing product adoption. Rising disposable income and growing consumer spending on home organization and kitchen upgrades are further driving regional demand for advanced food storage containers.

Key companies operating in the Global Food Storage Container Market include Amcor plc, Brabantia Branding B.V., Sistema Plastics, Sonoco Products Company, Novolex, LocknLock Co., Berry Global Inc., Sabert Corporation, OXO, EMSA GmbH, Zojirushi, Decor Corporation Pty. Ltd., Mepal, Tupperware, Borosil Limited, Anchor Hocking, Glasslock USA, Inc., Hamilton Housewares Pvt. Ltd., Corelle Brands, Rubbermaid Commercial Products, Cambro, and Zishta. Companies operating in the food storage container market are focusing on product innovation, sustainability initiatives, and expansion of premium product portfolios to strengthen their market position. Manufacturers are increasingly introducing reusable, BPA-free, recyclable, and microwave-safe containers to align with changing consumer preferences and environmental regulations. Many companies are investing in advanced material technologies to improve durability, leak resistance, and multifunctionality. Strategic collaborations with retail chains and e-commerce platforms are helping brands expand product accessibility and strengthen customer reach globally. Businesses are also emphasizing smart packaging designs, stackable storage formats, and aesthetically appealing products to improve customer engagement.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End-User trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing consumption of packaged and ready-to-eat food products

- 3.2.1.2 Growing demand from foodservice and commercial kitchen operations

- 3.2.1.3 Rising consumer shift toward sustainable and reusable storage solutions

- 3.2.1.4 Strong demand for advanced sealing and freshness-preserving features

- 3.2.1.5 Premiumization driven by demand for durable and high-quality materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High competition from low-cost and unorganized manufacturers

- 3.2.2.2 Concerns related to plastic safety and regulatory compliance

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of smart and digitally enabled food storage ecosystems

- 3.2.3.2 Market expansion driven by urbanization and evolving kitchen infrastructure in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Plastic

- 5.2.1 Polypropylene (PP)

- 5.2.2 High-density polyethylene (HDPE)

- 5.2.3 Polyethylene terephthalate (PET)

- 5.2.4 Others

- 5.3 Glass

- 5.4 Metal

- 5.5 Others

- 5.5.1 Silicone

- 5.5.2 Bamboo fiber

- 5.5.3 Wheat straw composites

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Boxes & bins

- 6.3 Jars & canisters

- 6.4 Bottles & cans

- 6.5 Bags & pouches

- 6.6 Others

- 6.6.1 Meal prep

- 6.6.2 Lunch boxes

- 6.6.3 Bento boxes

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Refrigerator storage

- 7.3 On-the-go & lunch containers

- 7.4 Freezer storage

- 7.5 Pantry storage

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Household/residential use

- 8.3 Commercial use

- 8.3.1 Quick-service restaurants (QSR)

- 8.3.2 Hotels & lodging

- 8.3.3 Cloud kitchens

- 8.3.4 Cafes & coffee shops

- 8.3.5 Others

- 8.4 Institutional use

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Tupperware Brands Corporation

- 10.1.2 Newell Brands (Rubbermaid)

- 10.1.3 LocknLock Co., Ltd.

- 10.1.4 Sistema Plastics

- 10.1.5 OXO (Helen of Troy)

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Amcor plc

- 10.2.1.2 Anchor Hocking

- 10.2.1.3 Berry Global Inc.

- 10.2.1.4 Cambro

- 10.2.1.5 Corelle Brands

- 10.2.1.6 Novolex

- 10.2.1.7 Sabert Corporation

- 10.2.1.8 Sonoco Products Company

- 10.2.2 Asia Pacific

- 10.2.2.1 Borosil Limited

- 10.2.2.2 Decor Corporation Pty. Ltd.

- 10.2.2.3 Glasslock USA, Inc.

- 10.2.2.4 Hamilton Housewares Pvt. Ltd.

- 10.2.2.5 Zojirushi

- 10.2.2.6 Zishta

- 10.2.3 Europe

- 10.2.3.1 EMSA GmbH

- 10.2.3.2 Mepal

- 10.2.3.3 Brabantia Branding B.V.

- 10.2.1 North America