PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072522

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072522

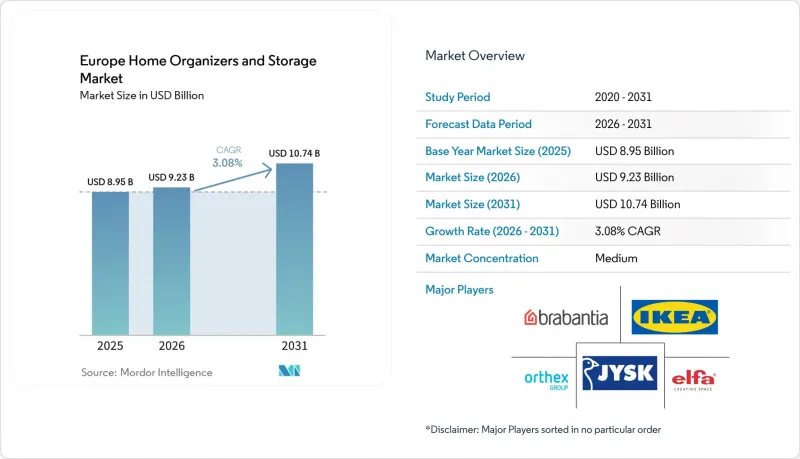

Europe Home Organizers and Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the home organizers and storage market size in Europe in 2026 is estimated at USD 9.23 billion, growing from 2025 value of USD 8.95 billion with 2031 projections showing USD 10.74 billion, growing at 3.08% CAGR over 2026-2031.

This report is Segmented by Product (Storage Baskets, Storage Boxes, Storage Bags, and More), Application (Bedroom Closets, Laundry Rooms, and More), Distribution Channel (Hypermarkets and Supermarkets, Specialty Stores, Online, Other Distribution Channels), and Geography (United Kingdom, Germany, France, Spain, Italy, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Home Organizers and Storage Market Trends and Insights

Rising DIY & Home-Improvement Culture

European households channel discretionary budgets into self-directed renovations as inflation encourages cost-saving home upgrades. The regional DIY segment is forecast to gain USD 32.9 billion between 2025 and 2029 at a 3.2% CAGR, creating steady demand for flat-pack organizers. How-to videos and retailer tutorials lower skill barriers, letting first-time buyers install modular closets without professional help. Retailers respond with QR-coded assembly guides and click-to-buy parts lists that simplify complex builds. IKEA's "Keep good things going" program reused 32.5 million pre-owned products in 2025, showing how DIY culture supports circular goals. Weekend project enthusiasm also lifts ancillary sales of screws, liners, and labelling kits, making storage one of the fastest-turning categories in big-box home centers. As consumer confidence stabilizes, DIY momentum is expected to remain a reliable volume driver through 2030.

Premiumization of Home Storage Products

The multifunctional home pushes buyers to view organizers as decor elements rather than utility bins. Consumers increasingly pay for solid-wood drawers, powder-coated steel frames, and soft-close hinges that match furniture quality standards. Retailers like The Container Store expand Custom Spaces offerings that embed LED lighting and sustainable veneers, raising average ticket sizes. Premium finishes complement rising interest in interior design, a trend amplified by social media tours of "perfect pantries" and color-coordinated closets. Higher price points create margin headroom that offsets raw-material inflation while funding store-level design consultations. Durability also speaks to environmental priorities because longer product life reduces replacement frequency. Premiumization, therefore, serves economic, aesthetic, and sustainability objectives simultaneously, reinforcing its status as a structural growth lever.

Supply-Chain Cost Inflation

Surging freight rates and resin prices squeeze margins, especially for mass-market plastic bins where consumers resist price hikes. Griffon's ClosetMaid division reported a 52% revenue drop in Europe between 2022 and 2023, citing weak demand and excess inventories built during logistics disruptions. To recover profitability, suppliers shorten bill-of-materials lists and localize component sourcing, but tooling changes raise upfront costs. Currency volatility further complicates cost planning for manufacturers reliant on Asian inputs. Retailers attempt to pass higher costs to consumers through "eco-upgrade" positioning, yet elastic segments experience volume declines when price thresholds are breached. Some brands hedge by shifting to lighter packaging that lowers dimensional weight charges, though material substitutions risk customer perception of reduced quality. Until freight indices normalize, cost inflation remains a prominent profitability headwind.

Other drivers and restraints analyzed in the detailed report include:

- Ageing Population Requiring Ergonomic Storage

- Circular-Economy Driven Modular Designs

- Slowdown in New Housing Starts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Modular Units are projected to deliver the steepest 4.52% CAGR through 2031, reflecting rising preference for components that expand with household needs. Storage Boxes remain the largest contributor, holding 28.86% of the home organizers and storage market share in 2025. The home organizers and storage market size devoted to Boxes equaled USD 2.58 billion that year, underpinning category stability. Consumers favor clear polypropylene totes for seasonal clothing rotation and heavy-duty corrugate boxes for long-term attic storage. Manufacturers differentiate through stackability indexes and reinforced lids to support warehouse-style vertical storage.

Urban renters gravitate toward modular cubes that fit studio apartments as bookcases today and shoe racks tomorrow, underscoring the value of reconfiguration. Players such as STOCUBO promote tool-free connectors and 1 cm increment sizing that lets buyers build wall-to-wall libraries without custom carpentry. Travel luggage organizers and hanging fabric compartments post steady gains by targeting specific pain points like suitcase packing and door-mounted accessory storage. As circular design moves mainstream, brands highlight component replacement programs that extend unit life and cement customer loyalty within the home organizers and storage market.

Complete Report Scope:

- By Product

- Storage Baskets

- Storage Boxes

- Storage Bags

- Hanging Storage

- Multipurpose Organizers

- Travel Luggage Organizers

- Modular Units

- Other Products

- By Application

- Bedroom Closets

- Laundry Rooms

- Home Offices

- Pantries and Kitchen

- Garages

- Other Applications

- By Distribution Channel

- Hypermarkets and Supermarkets

- Specialty Stores

- Online

- Other Distribution Channels

- By Geography

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

List of Companies Covered in this Report:

- IKEA Group

- Elfa International AB

- JYSK A/S

- Brabantia Branding BV

- Orthex Group

- Hettich Holding GmbH

- Hafele SE & Co KG

- Curver (Keter Group)

- Whitmor Inc.

- The Container Store Group Inc.

- Blum GmbH

- John Lewis PLC

- Leroy Merlin SA

- Muji Europe Holdings Ltd.

- Umbra LLC

- Tiger (Flying Tiger Copenhagen)

- Addis Housewares Ltd.

- Plast Team

- Wenko-Wenselaar GmbH

- Really Useful Products Ltd.

- H&M Home

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising DIY & Home-Improvement Culture

- 4.2.2 Premiumization of Home Storage Products

- 4.2.3 Ageing Population Requiring Ergonomic Storage

- 4.2.4 Circular-Economy Driven Modular Designs

- 4.2.5 Influencer-Led Micro-Organizing Trends

- 4.2.6 Rise of Urban Micro-Apartments

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Cost Inflation

- 4.3.2 Slowdown in New Housing Starts

- 4.3.3 Sustainability Scrutiny on Plastics

- 4.3.4 Rental Furniture & Storage-as-a-Service Models

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Competitive Rivalry

- 4.5.2 Threat of New Entrants

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Bargaining Power of Buyers

- 4.5.5 Threat of Substitutes

- 4.6 Insights Into The Latest Trends And Innovations in the Market

- 4.7 Insights On Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, Etc.) In The Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Storage Baskets

- 5.1.2 Storage Boxes

- 5.1.3 Storage Bags

- 5.1.4 Hanging Storage

- 5.1.5 Multipurpose Organizers

- 5.1.6 Travel Luggage Organizers

- 5.1.7 Modular Units

- 5.1.8 Other Products

- 5.2 By Application

- 5.2.1 Bedroom Closets

- 5.2.2 Laundry Rooms

- 5.2.3 Home Offices

- 5.2.4 Pantries and Kitchen

- 5.2.5 Garages

- 5.2.6 Other Applications

- 5.3 By Distribution Channel

- 5.3.1 Hypermarkets and Supermarkets

- 5.3.2 Specialty Stores

- 5.3.3 Online

- 5.3.4 Other Distribution Channels

- 5.4 By Geography

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Spain

- 5.4.5 Italy

- 5.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 IKEA Group

- 6.4.2 Elfa International AB

- 6.4.3 JYSK A/S

- 6.4.4 Brabantia Branding BV

- 6.4.5 Orthex Group

- 6.4.6 Hettich Holding GmbH

- 6.4.7 Hafele SE & Co KG

- 6.4.8 Curver (Keter Group)

- 6.4.9 Whitmor Inc.

- 6.4.10 The Container Store Group Inc.

- 6.4.11 Blum GmbH

- 6.4.12 John Lewis PLC

- 6.4.13 Leroy Merlin SA

- 6.4.14 Muji Europe Holdings Ltd.

- 6.4.15 Umbra LLC

- 6.4.16 Tiger (Flying Tiger Copenhagen)

- 6.4.17 Addis Housewares Ltd.

- 6.4.18 Plast Team

- 6.4.19 Wenko-Wenselaar GmbH

- 6.4.20 Really Useful Products Ltd.

- 6.4.21 H&M Home

7 Market Opportunities & Future Outlook

- 7.1 Premiumization of Home Storage and Organizers

- 7.2 Urban Living Constraints Boosting Compact Storage Designs