PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045827

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045827

Asia Pacific Central PV Inverter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

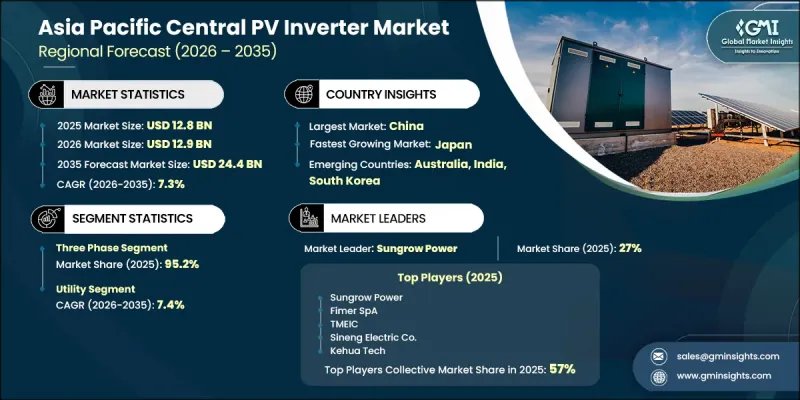

Asia Pacific Central PV Inverter Market was valued at USD 12.8 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 24.4 billion by 2035.

Market growth is driven by the increasing focus on lowering electricity generation costs and improving energy efficiency across large-scale solar power projects. Central PV inverters are gaining widespread adoption because they provide lower capital costs per watt, simplified maintenance requirements, and optimized balance of system expenses. Their capability to efficiently manage high-capacity direct current inputs while delivering strong operational performance over extended periods makes them highly suitable for utility-scale solar installations. Expanding investments in renewable energy infrastructure across Asia Pacific are further accelerating the deployment of central PV inverter technologies. In addition, the ongoing transition toward smart grid systems throughout the region is creating favorable conditions for advanced inverter integration. Governments are increasingly prioritizing grid modernization, digital monitoring technologies, and renewable energy integration policies to strengthen energy infrastructure and support rising solar power generation capacities. Continuous expansion of utility-scale solar developments and rising focus on grid reliability are expected to support long-term growth of the Asia Pacific central PV inverter industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.8 Billion |

| Forecast Value | $24.4 Billion |

| CAGR | 7.3% |

The three-phase segment accounted for 95.2% share and is projected to grow at a CAGR of 7.2% through 2035. Increasing deployment of large-scale solar photovoltaic facilities across the region is creating strong demand for three-phase central PV inverters due to their ability to manage high-capacity power generation efficiently. These systems support balanced electricity transmission and improve operational efficiency throughout the energy distribution process. The growing presence of major inverter manufacturers and technology providers across Asia Pacific is further contributing to segment expansion and technological advancements within the market.

The commercial sector is expected to grow at a CAGR of 6.7% through 2035. Rising government support for commercial decarbonization initiatives and increased accessibility to renewable energy procurement programs are encouraging businesses to adopt solar power solutions at a faster pace. Favorable regulatory frameworks and renewable energy policies are enabling commercial organizations to transition toward clean electricity sources, which is positively influencing demand for central PV inverter systems across the commercial segment.

China Central PV Inverter Market held a 73.5% share in 2025 and is projected to generate USD 12.8 billion by 2035. Market expansion in China is being supported by the rapid construction of large-scale solar power facilities across desert and semi-arid regions. These high-capacity solar developments require efficient centralized power conversion technologies capable of supporting large transmission networks and minimizing system complexity, making central PV inverters a preferred solution. In addition, increasing emphasis on maintaining grid stability and meeting stringent grid compliance standards amid rising renewable energy integration is expected to further strengthen demand for central PV inverters throughout the country.

Major companies operating in the Asia Pacific Central PV Inverter Market include ABB, Chint Power Systems, Delta Electronics, Eaton, Fimer SpA, Fronius International, Hitachi Energy, Hyosung Heavy Industries, INVT Solar, Kehua Tech, KSTAR, Omron Corporation, SAJ Electric, Sineng Electric Co., Sungrow Power, Statcon Energiaa, Tabuchi Electric, TBEA, TMEIC, and Waaree Energies. Companies operating in the Asia Pacific Central PV Inverter Market are adopting several strategic initiatives to strengthen their market presence and improve long-term competitiveness. Leading players are increasing investments in research and development to introduce advanced inverter technologies with higher efficiency, enhanced grid support capabilities, and improved operational reliability. Strategic collaborations with solar project developers, utility providers, and energy infrastructure companies are helping manufacturers expand their customer base and accelerate product adoption across emerging markets. Many companies are also focusing on expanding regional manufacturing facilities and supply chain networks to meet growing demand and improve delivery capabilities. In addition, businesses are prioritizing smart inverter integration, digital monitoring systems, and energy management solutions to align with evolving grid modernization initiatives.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Phase trends

- 2.4 Nominal Output Voltage trends

- 2.5 Nominal Output Power trends

- 2.6 Application trends

- 2.7 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of central PV inverter market

- 3.8 Price trend analysis (Driven by Primary Research)

- 3.8.1 Historical price trend analysis (Driven by Primary Research)

- 3.8.2 Central PV inverter pricing by phase (USD/MW) (Driven by Primary Research)

- 3.9 Trade data analysis (Driven by Primary Research)

- 3.9.1 Import/export value trends (Driven by Primary Research)

- 3.9.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.10 Production capacity & utilization (Driven by Primary Research)

- 3.10.1 Production capacity by country (Driven by Primary Research)

- 3.10.2 Utilization rates and expansion pipeline (Driven by Primary Research)

- 3.11 Impact of AI & generative AI on the market [SOLUTION CORE]

- 3.11.1 Predictive maintenance & fault detection

- 3.11.2 Grid optimization & load forecasting

- 3.11.3 Digital twin simulation & testing

- 3.11.4 Risks, limitations & regulatory considerations

- 3.12 Emerging opportunities & trends

- 3.12.1 Digitalization & IoT integration

- 3.12.2 Emerging market penetration

- 3.13 Overall investment scenario and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 China

- 4.2.2 Australia

- 4.2.3 India

- 4.2.4 Japan

- 4.2.5 South Korea

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Phase, 2022 - 2035 (USD Billion & MW)

- 5.1 Key trends

- 5.2 Single Phase

- 5.3 Three Phase

Chapter 6 Market Size and Forecast, By Nominal Output Voltage, 2022 - 2035 (USD Billion & MW)

- 6.1 Key trends

- 6.2 230 - 400 V

- 6.3 401 - 600 V

Chapter 7 Market Size and Forecast, By Nominal Output Power, 2022 - 2035 (USD Billion & MW)

- 7.1 Key trends

- 7.2 <110 kW

- 7.3 >110 kW

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion & MW)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Industrial

- 8.4 Utility

Chapter 9 Market Size and Forecast, By Country, 2022 - 2035 (USD Billion & MW)

- 9.1 Key trends

- 9.2 China

- 9.3 Australia

- 9.4 India

- 9.5 Japan

- 9.6 South Korea

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Chint Power Systems

- 10.3 Delta Electronics

- 10.4 Eaton

- 10.5 Fimer SpA

- 10.6 Fronius International

- 10.7 Hitachi Energy

- 10.8 Hyosung Heavy Industries

- 10.9 INVT Solar

- 10.10 Kehua Tech

- 10.11 KSTAR

- 10.12 Omron Corporation

- 10.13 SAJ Electric

- 10.14 Sineng Electric Co.

- 10.15 Sungrow Power

- 10.16 Statcon Energiaa

- 10.17 Tabuchi Electric

- 10.18 TBEA

- 10.19 TMEIC

- 10.20 Waaree Energies