PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045830

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045830

Semiconductor Memory Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

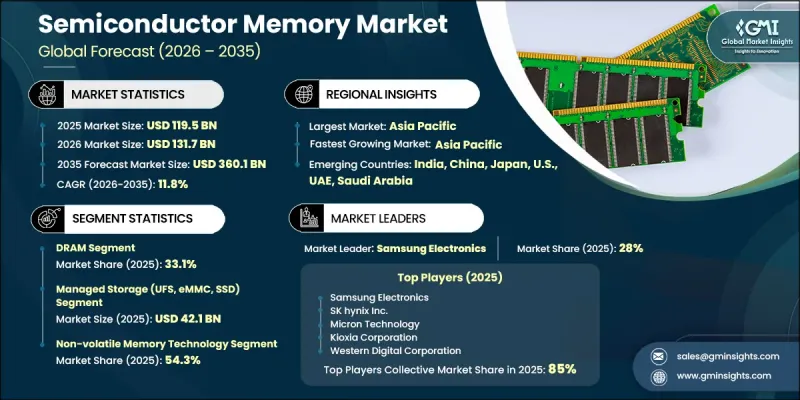

The Global Semiconductor Memory Market was valued at USD 119.5 billion in 2025 and is estimated to grow at a CAGR of 11.8% to reach USD 360.1 billion by 2035.

Rising demand for high-speed data processing, large-scale computing workloads, and advanced digital infrastructure is significantly supporting the growth of the semiconductor memory industry. Rapid expansion of cloud computing ecosystems, hyperscale data centers, and connected technologies is increasing the requirement for high-capacity and high-performance memory solutions across multiple industries. The growing use of artificial intelligence, machine learning, edge computing, and advanced networking technologies is further accelerating market expansion. Semiconductor memory solutions are becoming essential for handling complex workloads that require faster processing speeds, lower latency, and greater bandwidth efficiency. Increasing adoption of smart consumer electronics, connected vehicles, and industrial automation systems is also strengthening market demand. In addition, continuous advancements in memory architectures, packaging technologies, and energy-efficient designs are improving overall system performance while supporting the transition toward next-generation digital ecosystems. The rising deployment of advanced communication infrastructure and distributed computing environments is expected to create long-term opportunities for semiconductor memory manufacturers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $119.5 Billion |

| Forecast Value | $360.1 Billion |

| CAGR | 11.8% |

The semiconductor memory industry is witnessing substantial growth due to the increasing adoption of artificial intelligence applications that require extremely high bandwidth and scalable memory capacity. AI-driven computing environments rely heavily on advanced memory technologies to improve computational efficiency and reduce performance bottlenecks associated with large-scale data movement. Furthermore, the rapid expansion of next-generation communication networks and distributed computing infrastructure is contributing significantly to market growth. The growing deployment of advanced networking systems, edge infrastructure, and digital processing platforms is creating strong demand for semiconductor memory capable of delivering fast and reliable data access.

The DRAM segment accounted for 33.1% share in 2025, maintaining its leadership position owing to extensive adoption across cloud computing platforms, enterprise systems, automotive electronics, and consumer devices. DRAM continues to remain a preferred memory technology for applications requiring rapid data retrieval, multitasking capabilities, and high processing efficiency. Its importance as a primary operational memory solution continues to generate consistent demand across multiple end-use industries.

The HBM and 3D stacked memory segment is anticipated to register a CAGR of 12.5% throughout the forecast period. Growth in this category is driven by increasing deployment in artificial intelligence accelerators, advanced computing systems, and large-scale data center environments. These memory technologies provide significantly higher bandwidth and improved power efficiency through vertically integrated architectures. The rising intensity of data-heavy computing operations is accelerating the adoption of advanced stacked memory technologies across modern digital infrastructure.

North America Semiconductor Memory Market accounted for 37.5% share in 2025. Strong growth across the region is supported by increasing investments in cloud infrastructure, enterprise digitization, advanced computing systems, and high-capacity data centers. The growing use of artificial intelligence platforms and performance-driven computing technologies is increasing memory requirements across servers, networking equipment, and enterprise hardware. Early adoption of advanced digital technologies throughout North America continues to strengthen long-term demand for semiconductor memory solutions.

Key companies operating in the Global Semiconductor Memory Market include Intel Corporation, Samsung Electronics Co., Micron Technology, Inc., SK hynix Inc., Western Digital Corporation, Kioxia Corporation, Kingston Technology Company, Inc., ADATA Technology Co., Ltd., Nanya Technology Corporation, Macronix International Co., Ltd., Texas Instruments Incorporated, Renesas Electronics Corporation, STMicroelectronics N.V., Microchip Technology Inc., Avalanche Technology, Inc., Everspin Technologies, Inc., Winbond Electronics Corporation, and Cypress Semiconductor Corporation. Companies operating in the Semiconductor Memory Market are focusing on several strategic initiatives to strengthen their market position and improve long-term competitiveness. Major players are increasing investments in research and development to introduce advanced memory technologies with higher bandwidth, lower latency, and improved power efficiency. Businesses are also expanding manufacturing capabilities and enhancing supply chain resilience to address growing global demand. Strategic collaborations with cloud service providers, AI hardware developers, and data center operators are helping manufacturers expand their customer base and accelerate technology adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Memory type trends

- 2.2.2 Form factor trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.2.5 End-use industry trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand from AI-intensive and compute-heavy applications

- 3.2.1.2 Rapid build-out of 5G networks and distributed computing architectures

- 3.2.1.3 Sustained growth in smart devices and consumer electronics

- 3.2.1.4 Rising memory requirements in automotive and electric vehicles

- 3.2.1.5 Ongoing expansion of cloud platforms and hyperscale data centers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High volatility in memory pricing cycles

- 3.2.2.2 High capital intensity and long capacity expansion timelines

- 3.2.3 Market opportunities

- 3.2.3.1 Advanced packaging and chiplet-based memory integration

- 3.2.3.2 Localization of memory manufacturing and government-backed fab incentives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Memory Type, 2022 - 2035 (USD Billion & Units)

- 5.1 Key trends

- 5.2 DRAM

- 5.3 SRAM

- 5.4 NAND flash memory

- 5.5 NOR flash memory

- 5.6 Others (MRAM, ReRAM, PCM)

Chapter 6 Market Estimates and Forecast, By Form Factor, 2022 - 2035 (USD Billion & Units)

- 6.1 Key trends

- 6.2 Discrete IC

- 6.3 Embedded memory

- 6.4 Managed storage (UFS, eMMC, SSD)

- 6.5 HBM & 3D-stacked memory

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Volatile memory technology

- 7.3 Non-volatile memory technology

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion & Units)

- 8.1 Key trends

- 8.2 Storage memory

- 8.3 Processing memory

- 8.4 Cache memory

- 8.5 Embedded & code storage memory

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Billion & Units)

- 9.1 Key trends

- 9.2 Consumer electronics

- 9.3 Computing & IT

- 9.4 Data centers & cloud

- 9.5 Automotive electronics

- 9.6 Industrial & manufacturing

- 9.7 Telecom & networking

- 9.8 Healthcare electronics

- 9.9 Aerospace & defense

- 9.10 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Samsung Electronics Co.

- 11.1.2 SK hynix Inc.

- 11.1.3 Micron Technology, Inc.

- 11.1.4 Kioxia Corporation

- 11.1.5 Western Digital Corporation

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Kingston Technology Company, Inc.

- 11.2.1.2 Cypress Semiconductor Corporation (Infineon Technologies)

- 11.2.1.3 Microchip Technology Inc.

- 11.2.1.4 Texas Instruments Incorporated

- 11.2.1.5 Intel Corporation

- 11.2.2 Asia Pacific

- 11.2.2.1 ADATA Technology Co., Ltd.

- 11.2.2.2 Macronix International Co., Ltd.

- 11.2.2.3 Nanya Technology Corporation

- 11.2.3 Europe

- 11.2.3.1 STMicroelectronics N.V.

- 11.2.3.2 Renesas Electronics Corporation

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Everspin Technologies, Inc.

- 11.3.2 Avalanche Technology, Inc.

- 11.3.3 Winbond Electronics Corporation