PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045864

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045864

Intermediate Metal Conduit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

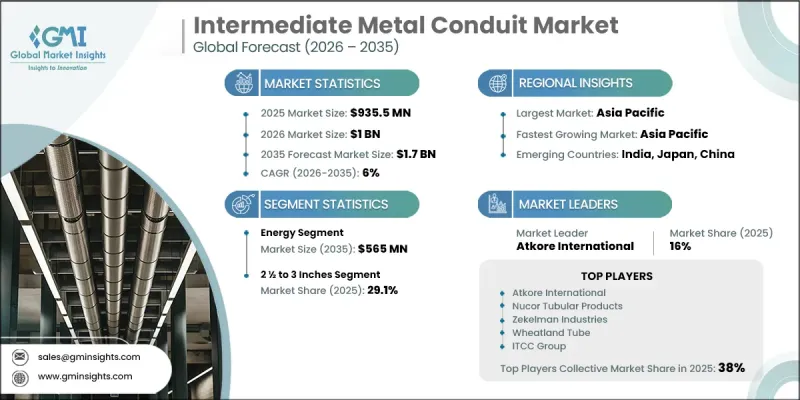

The Global Intermediate Metal Conduit Market was valued at USD 935.5 million in 2025 and is estimated to grow at a CAGR of 6% to reach USD 1.7 billion by 2035.

Rapid urbanization, large-scale infrastructure modernization, and expanding industrial development are major factors driving growth across the intermediate metal conduit industry. Increasing emphasis on electrical safety and reliable wiring systems across commercial, residential, and industrial sectors continues to strengthen demand for intermediate metal conduits. These conduits are gaining widespread adoption due to their cost efficiency, durability, and strong protective capabilities compared to heavier conduit alternatives. Rising implementation of strict electrical and fire safety regulations is also supporting market expansion globally. In addition, ongoing upgrades to power transmission and distribution infrastructure, coupled with increasing installations in challenging operating environments, are accelerating product adoption. Growing investments in renewable energy projects, smart grid systems, data centers, and advanced electrical infrastructure are further contributing to rising demand for intermediate metal conduits, particularly in regions focused on strengthening grid reliability and improving safety standards. The market is also witnessing an increasing preference for lightweight and economical conduit systems capable of supporting efficient electrical installations across modern construction and industrial applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $935.5 Million |

| Forecast Value | $1.7 Billion |

| CAGR | 6% |

The intermediate metal conduit market continues to experience steady demand due to its combination of structural strength, corrosion resistance, and installation flexibility. Commercial and residential construction projects are increasingly utilizing intermediate metal conduits because they provide reliable electrical protection while reducing overall installation costs. Expanding industrial automation activities and rising investment in advanced infrastructure projects are further contributing to market growth. In addition, increasing focus on long-term electrical safety and improved system durability is encouraging broader adoption of intermediate metal conduits across multiple end-use sectors worldwide.

The 21/2 to 3 trade size segment accounted for 29.1% share in 2025. Rising utilization of larger conduit systems across industrial facilities, large-scale construction developments, and energy infrastructure projects is significantly contributing to segment expansion. Intermediate metal conduits within this trade size range are widely preferred for extensive electrical wiring applications because they offer high mechanical strength, corrosion resistance, and cost-effective installation performance. Increasing investments in renewable energy infrastructure and expanding power distribution networks are also driving demand for larger conduit sizes capable of supporting high-capacity electrical systems operating under demanding environmental conditions.

U.S. Intermediate Metal Conduit Market was valued at USD 137.7 million in 2025. Market growth across the country is supported by rising infrastructure investments, industrial expansion, and increasingly stringent safety regulations governing electrical installations. Growing demand for durable and cost-efficient conduit systems in commercial construction and industrial wiring applications continues to strengthen product adoption. In addition, the expansion of renewable energy projects and advancements in construction technologies are creating additional opportunities for intermediate metal conduit manufacturers throughout the United States market.

Major companies operating in the Global Intermediate Metal Conduit Market include ALEX, ARNET, Atkore International, Baolai Steel, Cat Van Loi, East Steel Pipe, ELECMAN, Eurotray, Hangzhou EVT Electrical, Hangzhou Topele Electrical, ITCC Group, Lonwow Industry, Nucor Tubular Products, Southern Steel Pipe, Tianjin Rainbow Steel, TSI INOX CONDUIT, Western Tube & Conduit, Wheatland Tube, Zekelman Industries, and ZHEJIANG AXWILL ELECTRICAL. Companies operating in the intermediate metal conduit market are adopting several strategic initiatives to strengthen their competitive position and expand market presence. Manufacturers are investing in advanced production technologies to improve product durability, corrosion resistance, and installation efficiency. Businesses are also focusing on expanding manufacturing capacity and strengthening distribution networks to meet rising global demand across infrastructure and industrial projects. Strategic partnerships with construction firms, utility providers, and industrial contractors are helping companies improve market penetration and secure long-term supply agreements. In addition, market participants are increasing investments in product innovation to develop lightweight and high-performance conduit systems that comply with evolving electrical safety standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.8.3.1 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Trade size trends

- 2.4 Application trends

- 2.5 End use trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.7 Cost structure analysis of intermediate metallic conduits

- 3.8 Trade data analysis (Driven by Primary Research)

- 3.8.1 Import/export value trends (Driven by Primary Research)

- 3.8.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.9 Production capacity & utilization (Driven by Primary Research)

- 3.9.1 Production capacity by region (Driven by Primary Research)

- 3.9.2 Utilization rates and expansion pipeline (Driven by Primary Research)

- 3.10 Emerging opportunities & trends

- 3.11 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key Developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Trade Size, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 1/2 to 1

- 5.3 1 1/4 to 2

- 5.4 2 1/2 to 3

- 5.5 3 to 4

- 5.6 5 to 6

- 5.7 Others

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Rail infrastructure

- 6.3 Manufacturing facilities

- 6.4 Shipbuilding & offshore facilities

- 6.5 Process plants

- 6.6 Energy

- 6.7 Others

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

- 7.5 Utility

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 France

- 8.3.2 Germany

- 8.3.3 Italy

- 8.3.4 UK

- 8.3.5 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ALEX

- 9.2 ARNET

- 9.3 Atkore International

- 9.4 Baolai Steel

- 9.5 Cat Van Loi

- 9.6 East Steel Pipe

- 9.7 ELECMAN

- 9.8 Eurotray

- 9.9 Hangzhou EVT Electrical

- 9.10 Hangzhou Topele Electrical

- 9.11 ITCC Group

- 9.12 Lonwow Industry

- 9.13 Nucor Tubular Products

- 9.14 Southern Steel Pipe

- 9.15 Tianjin Rainbow Steel

- 9.16 TSI INOX CONDUIT

- 9.17 Western Tube & Conduit

- 9.18 Wheatland Tube

- 9.19 Zekelman Industries

- 9.20 ZHEJIANG AXWILL ELECTRICAL