PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045880

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045880

Autonomous Long-Haul Trucking Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

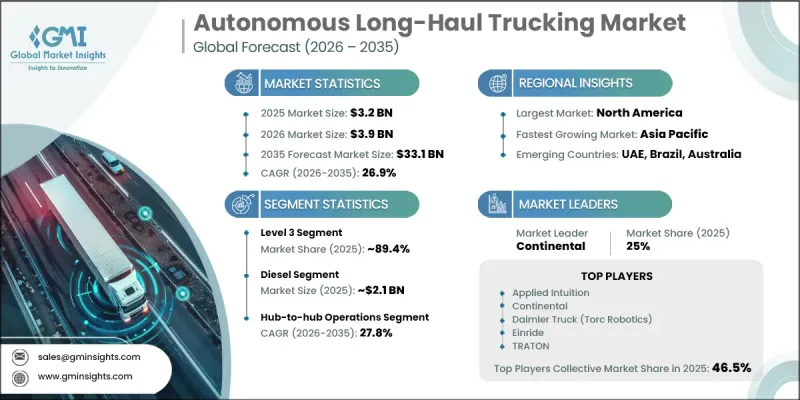

The Global Autonomous Long-Haul Trucking Market was valued at USD 3.2 billion in 2025 and is estimated to grow at a CAGR of 26.9% to reach USD 33.1 billion by 2035.

The autonomous long-haul trucking industry is evolving rapidly as logistics providers prioritize efficiency, safety, and cost optimization across freight operations. Market revenue is generated through autonomy-focused components and services, including sensor technologies, onboard computing systems, redundant control mechanisms, software licensing, over-the-air upgrades, integration services, remote operations, maintenance, and data analytics, while excluding the base vehicle cost. Growth momentum is expected to accelerate toward the latter part of the decade as Level 4 autonomy progresses from supervised deployment to fully driverless operation within defined routes. Procurement strategies are shifting from pilot-based deployments to standardized offerings integrated into manufacturer portfolios. Regulatory development and validation frameworks are supporting commercialization efforts, enabling fleet operators to advance safety protocols and operational readiness. The combination of technological innovation, structured deployment strategies, and increasing industry confidence is positioning the market for sustained expansion across global logistics networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.2 Billion |

| Forecast Value | $33.1 Billion |

| CAGR | 26.9% |

Operational deployment strategies are focused on optimizing long-distance freight movement through structured route planning and high-utilization models. Fleet operators are prioritizing specific distance ranges between logistics nodes, where continuous operation significantly improves asset productivity and reduces turnaround times. Market expansion is occurring in a phased manner, with deployment determined by infrastructure readiness and regulatory alignment. This targeted approach is enabling controlled scalability and more efficient implementation of autonomous trucking systems across key freight corridors.

The Level 3 segment held an 89.4% share, generating USD 2.8 billion in 2025. This dominance reflects current regulatory requirements that maintain human oversight while allowing advanced automation features. Level 3 systems have progressed beyond basic driver assistance by incorporating enhanced operational capabilities that improve efficiency and safety while maintaining driver involvement. Continued advancements in system functionality and validation processes are reducing adoption barriers and strengthening confidence among fleet operators.

The hub-to-hub operations segment is projected to grow with a CAGR of 27.8% between 2026 and 2035. This operating model aligns well with the current capabilities of autonomous systems, as it focuses on long-distance routes with relatively predictable driving conditions. The structured nature of these operations supports efficient logistics coordination, allowing companies to streamline freight movement between designated transfer points. This approach enables a hybrid operational framework, where autonomous systems manage extended routes while human intervention supports localized distribution tasks.

U.S. Autonomous Long-Haul Trucking Market reached USD 1.1 billion in 2025 and is expected to grow at a CAGR of 27.4% from 2026 to 2035. The country remains a key hub for innovation and deployment due to its advanced logistics ecosystem, extensive transportation infrastructure, and strong presence of technology developers and manufacturers. Large-scale freight demand and ongoing advancements in regulatory frameworks are supporting continued testing and commercialization efforts. The adoption of structured transport models is further facilitating the integration of autonomous trucking technologies into mainstream logistics operations.

Key companies operating in the Global Autonomous Long-Haul Trucking Market include Kodiak Robotics, Aurora Innovation, Applied Intuition, Continental, Daimler Truck (Torc Robotics), Einride, Hino Motors, Plus.ai, Pony AI, and TRATON. Companies in the autonomous long-haul trucking market are adopting a range of strategic initiatives to strengthen their market position. Firms are heavily investing in research and development to enhance autonomy capabilities, improve system reliability, and accelerate the transition toward higher levels of automation. Strategic collaborations with logistics providers and technology partners are being leveraged to expand deployment opportunities and validate real-world performance. Companies are also focusing on scalable business models, including software-based revenue streams and service-oriented offerings. Expansion into key logistics corridors and infrastructure partnerships is enabling more efficient deployment.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Automation Level

- 2.2.3 Propulsion

- 2.2.4 Vehicle Class

- 2.2.5 Application

- 2.2.6 End-Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Driver Shortage Crisis & Rising Labor Costs

- 3.2.1.2 Demand for 24/7 Freight Operations & Asset Utilization

- 3.2.1.3 Safety Improvements & Accident Reduction Potential

- 3.2.1.4 Fuel Efficiency Gains & Operating Cost Reduction

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Technology & Vehicle Acquisition Costs

- 3.2.2.2 Public Safety Concerns & Acceptance Barriers

- 3.2.3 Market opportunities

- 3.2.3.1 Government Infrastructure Investments in Smart Roads

- 3.2.3.2 Integration with Warehouse Automation & Last-Mile Solutions

- 3.2.3.3 Retrofit Autonomous Systems for Existing Truck Fleets

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technologies

- 3.3.1.1 LiDAR-based Perception Systems

- 3.3.1.2 Radar and Camera Sensor Fusion Systems

- 3.3.1.3 High-Definition (HD) Mapping Technology

- 3.3.2 Emerging technologies

- 3.3.2.1 Vehicle-to-Everything (V2X) Cooperative Communication Systems

- 3.3.2.2 5G/6G Ultra-Low Latency Connectivity for Freight Platooning

- 3.3.2.3 AI-Based End-to-End Driving Foundation Models

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 US - Federal Motor Carrier Safety Administration (FMCSA)

- 3.5.1.2 US - Federal Motor Carrier Safety Administration (FMCSA)

- 3.5.1.3 Canada - Transport Canada

- 3.5.2 Europe

- 3.5.2.1 EU - Directorate-General for Mobility and Transport (DG MOVE)

- 3.5.2.2 Germany - Kraftfahrt-Bundesamt (KBA)

- 3.5.3 Asia Pacific

- 3.5.3.1 China - Ministry of Industry and Information Technology (MIIT)

- 3.5.3.2 South Korea - Ministry of Land, Infrastructure and Transport (MOLIT)

- 3.5.4 Latin America

- 3.5.4.1 Brazil - Agencia Nacional de Transportes Terrestres (ANTT)

- 3.5.4.2 Mexico - Secretaria de Infraestructura, Comunicaciones y Transportes (SICT)

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE - Road and Transport Authority (RTA)

- 3.5.5.2 Saudi Arabia - Transport General Authority (TGA)

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent landscape (Driven by Primary Research)

- 3.9 Trade Data Analysis (Based on Paid Database)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Production Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

- 3.11 Cost breakdown analysis

- 3.11.1 Vehicle hardware & sensor suite costs

- 3.11.2 Autonomous software development and licensing costs

- 3.11.3 Connectivity and communication infrastructure costs

- 3.11.4 Fleet operations, remote monitoring, and maintenance costs

- 3.12 Infrastructure Readiness and Smart Road Networks

- 3.12.1 V2I Communication Systems

- 3.12.2 5G & Dedicated Short-Range Communications (DSRC) Deployment

- 3.12.3 Smart Highway Pilot Projects & Dedicated Autonomous Lanes

- 3.12.4 Charging & Fueling Infrastructure for Autonomous Electric Trucks

- 3.12.5 High-Definition Mapping Coverage & Updates

- 3.13 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.13.1 AI-Driven Disruption of Existing Business Models

- 3.13.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.13.3 Risks, Limitations & Regulatory Considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Automation Level, 2022 - 2035 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Level 3

- 5.3 Level 4

- 5.4 Level 5

Chapter 6 Market Estimates and Forecast, By Propulsion, 2022 - 2035 ($ Mn, Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Electric

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By Vehicle Class, 2022 - 2035 ($ Mn, Units)

- 7.1 Key trends

- 7.2 Class 7 (26,001-33,000 lbs GVWR)

- 7.3 Class 8 (33,001+ lbs GVWR)

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn, Units)

- 8.1 Key trends

- 8.2 Hub-to-Hub Operations

- 8.3 Long-Distance Freight Transport

- 8.4 Port & Terminal Logistics

- 8.5 Cross-Border Logistics

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn, Units)

- 9.1 Key trends

- 9.2 Logistics & Fleet Operators

- 9.3 Retail & E-Commerce

- 9.4 FMCG & Food Supply Chains

- 9.5 Industrial Goods Suppliers

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Norway

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 South Korea

- 10.4.4 India

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Vietnam

- 10.4.8 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Chile

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Aurora Innovation

- 11.1.2 Waymo (Alphabet)

- 11.1.3 Kodiak Robotics

- 11.1.4 Daimler Truck (Torc Robotics)

- 11.1.5 Volvo Autonomous Solutions

- 11.1.6 CreateAI

- 11.1.7 Plus.ai

- 11.1.8 Applied Intuition

- 11.1.9 Stack AV

- 11.1.10 Einride

- 11.1.11 Waabi Innovation

- 11.1.12 Continental

- 11.2 Regional players

- 11.2.1 Inceptio Technology

- 11.2.2 Pony AI

- 11.2.3 TRATON

- 11.2.4 Hino Motors

- 11.2.5 Gatik AI

- 11.3 Emerging players

- 11.3.1 Outrider Technologies

- 11.3.2 Minus Zero

- 11.3.3 FERNRIDE