PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061289

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061289

Milling Motor Spindle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

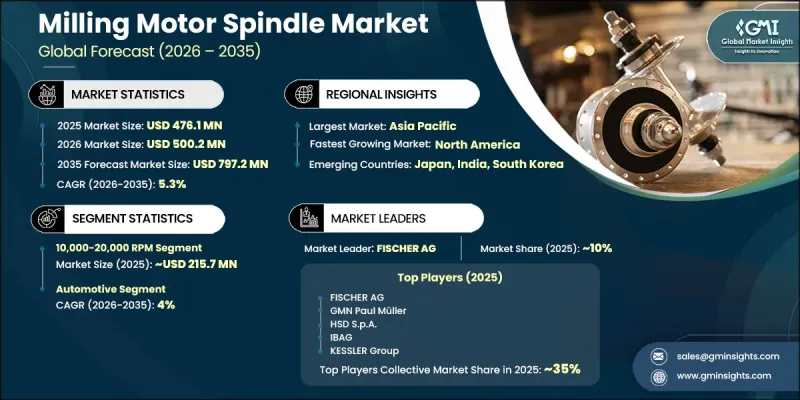

The Global Milling Motor Spindle Market was valued at USD 476.1 million in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 797.2 million by 2035.

Milling motor spindles help in advanced machining operations by transforming electrical energy into high-speed mechanical motion for precision cutting applications. These integrated systems combine essential spindle components into a compact structure that delivers improved efficiency, accuracy, and operational stability compared to traditional spindle technologies. The milling motor spindle industry continues to expand steadily due to increasing industrial automation, rapid adoption of smart manufacturing technologies, and rising demand for high-precision machining across major end-use sectors. Growing production requirements for technologically advanced components are further supporting market expansion worldwide. In addition, the increasing use of compact electronic products and next-generation semiconductor technologies is accelerating demand for ultra-precise machining solutions capable of maintaining extremely tight tolerances. The medical manufacturing sector is also contributing significantly to market growth as demand rises for highly accurate machining systems used in the production of specialized healthcare equipment and customized components.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $476.1 Million |

| Forecast Value | $797.2 Million |

| CAGR | 5.3% |

The 10,000-20,000 RPM segment generated USD 215.7 million in 2025 and is expected to grow at a CAGR of 4.8% between 2026 and 2035. This speed range remains widely preferred across industrial manufacturing applications due to its ability to deliver an effective combination of machining efficiency, cutting precision, and extended tool performance. Milling motor spindles operating within this RPM range are extensively utilized for processing a broad range of metal materials commonly used in industrial production environments. Their capability to support stable machining operations while maintaining productivity and operational reliability continues to drive strong adoption across multiple manufacturing industries.

The automotive segment accounted for 31.8% share in 2025 and is projected to grow at a CAGR of 4% through 2035. The automotive industry remains the largest end-use sector for milling motor spindles due to the extensive machining requirements associated with the production of critical vehicle components. Increasing manufacturing activity related to electric mobility is creating additional demand for advanced spindle systems capable of delivering high-precision machining for lightweight materials and complex component structures. The growing focus on efficient vehicle production, improved component quality, and precision engineering continues to strengthen spindle demand across the automotive manufacturing ecosystem.

U.S. Milling Motor Spindle Market reached USD 76.1 million in 2025, and is forecast to register a CAGR of 6.5% from 2026 to 2035. Strong industrial manufacturing capabilities, rising investments in advanced production technologies, and growing demand for precision machining solutions are supporting market growth throughout the country. Expanding production activities related to electric mobility, industrial automation, and advanced manufacturing systems are increasing the need for high-performance spindle technologies across the U.S. market. In addition, the country's well-established aerospace and industrial sectors continue to generate strong demand for precision machining systems capable of handling high-strength materials while maintaining superior accuracy and operational efficiency.

Major companies operating in the Global Milling Motor Spindle Market include FANUC Corporation, FISCHER AG, GMN Paul Muller Industrie GmbH & Co. KG, HSD S.p.A., IBAG, KESSLER Group, NSK Ltd, SycoTec GmbH & Co. KG, and United Grinding Group among global participants. Key regional players active in the industry include Changzhou Holry Electric Technology Co., Ltd., Changzhou WHD Spindle Motor Co., Ltd., Citizen Chiba Precision Co., Ltd, Guangzhou Haozhi Industrial Co., Ltd, Hiteco S.p.A., Jingjiang Jianken High-Speed Electric Motor Co., Ltd., and SETCO. Companies operating in the milling motor spindle industry are implementing several strategic initiatives to strengthen their market presence and improve competitive positioning. Leading manufacturers are investing heavily in research and development activities to introduce technologically advanced spindle systems with improved speed, efficiency, durability, and precision capabilities. Many companies are also focusing on expanding manufacturing facilities and strengthening regional distribution networks to improve customer reach and production capacity. Strategic collaborations with industrial automation providers and machining equipment manufacturers are helping market participants enhance product integration and broaden application opportunities. In addition, businesses are increasingly emphasizing customized spindle solutions tailored to specific industrial requirements, enabling them to address evolving customer demands more effectively.

Table of Contents

Chapter 1 Research methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Business trends

- 2.3 Regional

- 2.4 Speed range

- 2.5 Power rating

- 2.6 Application

- 2.7 End use industry

- 2.8 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Manufacturer

- 3.1.3 Profit margin analysis

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Automotive Industry Lightweighting Initiatives

- 3.2.1.2 Aerospace Manufacturing Complexity

- 3.2.1.3 Electronics Miniaturization Trends

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial Investment Costs

- 3.2.2.2 Technical Complexity and Maintenance Requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.7 Trade data analysis

- 3.8 Regulatory landscape

- 3.8.1 Standards and compliance requirements

- 3.8.2 Regional regulatory frameworks

- 3.8.3 Certification standards

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Speed Range, 2022 - 2035, (USD Million) (Units)

- 5.1 Key trends

- 5.2 Up to 10,000 RPM

- 5.3 10,000 to 20,000 RPM

- 5.4 Above 20,000 RPM

Chapter 6 Market Estimates & Forecast, By Power Rating, 2022 - 2035, (USD Million) (Units)

- 6.1 Key trends

- 6.2 Up to 5 kW

- 6.3 5 to 15 kW

- 6.4 Above 15 kW

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Million) (Units)

- 7.1 Key trends

- 7.2 Precision milling

- 7.3 Roughing

- 7.4 Micro-milling

- 7.5 Hard material machining

- 7.6 Mold & die making

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Million) (Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace & defense

- 8.4 Electronics & semiconductors

- 8.5 Medical devices

- 8.6 General manufacturing

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Units)

- 9.1 Key trends

- 9.2 Direct Sales

- 9.3 Indirect Sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Sweden

- 10.3.7 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 FANUC Corporation

- 11.1.2 FISCHER AG

- 11.1.3 GMN Paul Muller Industrie GmbH & Co. KG

- 11.1.4 HSD S.p.A.

- 11.1.5 IBAG

- 11.1.6 KESSLER Group

- 11.1.7 NSK Ltd

- 11.1.8 SycoTec GmbH & Co. KG

- 11.1.9 United Grinding Group

- 11.2 Regional Players

- 11.2.1 Changzhou Holry Electric Technology Co., Ltd.

- 11.2.2 Changzhou WHD Spindle Motor Co., Ltd.

- 11.2.3 Citizen Chiba Precision Co., Ltd

- 11.2.4 Guangzhou Haozhi Industrial Co., Ltd

- 11.2.5 Hiteco S.p.A.

- 11.2.6 Jingjiang Jianken High-Speed Electric Motor Co., Ltd.

- 11.2.7 SETCO

- 11.3 Emerging Players & Innovators

- 11.3.1 Zhengzhou Sinomach Precision Industry Development

- 11.3.2 Jiangsu Swift Machinery Technology Co., Ltd.

- 11.3.3 Lishui Hengli Automation Technology

- 11.3.4 DECI Spindle Motor