PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061314

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061314

Vehicle-to-Grid (V2G) Communication Protocols and Aggregation Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

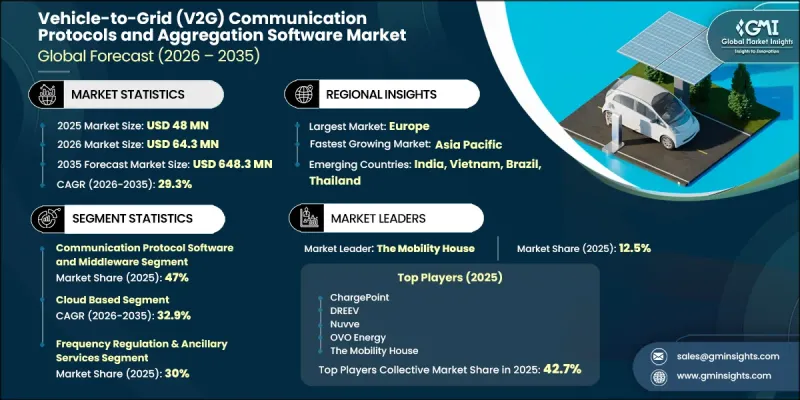

The Global Vehicle-to-Grid (V2G) Communication Protocols and Aggregation Software Market was valued at USD 48 million in 2025 and is estimated to grow at a CAGR of 29.3% to reach USD 648.3 million by 2035.

The market is witnessing rapid expansion due to the accelerating penetration of electric vehicles and the growing need for interoperable communication and aggregation platforms that enable seamless interaction between vehicles, charging infrastructure, utilities, and energy markets. Increasing deployment of bidirectional charging systems is boosting demand for standardized communication frameworks such as ISO 15118 and OCPP, alongside advanced grid integration software. These technologies enable secure energy exchange, intelligent charging control, and real-time load balancing across distributed energy ecosystems. Rising investments from utilities and grid operators in aggregation platforms are aimed at improving grid stability during peak demand periods while efficiently managing distributed EV fleets. Additionally, the growing integration of renewable energy sources and decentralized storage systems is strengthening the adoption of advanced V2G software solutions. Expanding deployment of smart charging networks, combined with increasing emphasis on energy flexibility and digital grid transformation, is further accelerating market development globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $48 Million |

| Forecast Value | $648.3 Million |

| CAGR | 29.3% |

The passenger EV cloud-based deployment segment accounted for 62% share in 2025 and is projected to grow at a CAGR of 32.9% from 2026 to 2035. Cloud-based platforms are widely preferred due to their ability to centralize control, reduce infrastructure costs, and enable scalable energy management across large and distributed charging networks. These systems also support real-time monitoring, remote software updates, and advanced analytics for charging optimization and grid interaction, making them a core enabler of large-scale V2G deployment.

The frequency regulation and ancillary services segment held a 30% share in 2025, driven by increasing demand for grid stabilization solutions supported by flexible distributed energy resources. V2G-enabled systems are increasingly utilized to provide frequency balancing by dynamically managing EV charging and discharging patterns in response to grid fluctuations. This capability is becoming essential as power systems integrate higher levels of variable renewable energy and require more responsive balancing mechanisms.

United States Vehicle-to-Grid (V2G) Communication Protocols and Aggregation Software Market held an 85% share in 2025, reaching USD 13.1 million. Market growth in the country is strongly influenced by rising electric vehicle adoption, rapid expansion of charging infrastructure, and increasing investments in smart grid modernization initiatives. Utility companies and charging network operators are actively deploying advanced communication and energy management platforms across public and commercial charging ecosystems to support large-scale EV integration and grid interaction.

Major companies operating in the Global Vehicle-to-Grid (V2G) Communication Protocols and Aggregation Software Market include Nuvve, The Mobility House, ChargePoint, Enel, DREEV, Virta, Hubject, OVO Energy, Uplight, and Virtual Peaker. Companies in the Vehicle-to-Grid (V2G) communication protocols and aggregation software market are focusing on strategic initiatives to strengthen market position and expand technological capabilities. Key players are investing heavily in software innovation to enhance interoperability, real-time energy optimization, and secure bidirectional charging communication. Partnerships with automotive manufacturers, utilities, and charging infrastructure providers are enabling faster deployment of integrated V2G ecosystems. Firms are also prioritizing cloud-native and AI-driven platforms to improve predictive load management and grid responsiveness. Expansion into large-scale pilot projects and commercial deployments is helping validate technology performance and accelerate adoption. Additionally, companies are working on aligning their platforms with global communication standards such as ISO 15118 and OCPP to ensure compatibility across diverse charging networks, while also enhancing cybersecurity frameworks to support secure energy transactions within increasingly complex distributed energy systems.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Solution

- 2.2.3 Deployment Mode

- 2.2.4 Application

- 2.2.5 End-User

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of commercial vehicle fleets

- 3.2.1.2 Rising adoption of electric commercial vehicles

- 3.2.1.3 Increasing cold chain and logistics operations

- 3.2.1.4 Stringent cabin comfort and air quality regulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High maintenance cost of advanced HVAC systems

- 3.2.2.2 Shortage of skilled service technicians

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of predictive maintenance technologies

- 3.2.3.2 Expansion of electric bus and truck fleets

- 3.2.3.3 Growth in aftermarket service networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 U.S. FERC Order 2222

- 3.6.1.2 California EV Charging Infrastructure Regulations

- 3.6.1.3 Canada Electric Vehicle Availability Standard

- 3.6.2 Europe

- 3.6.2.1 EU Alternative Fuels Infrastructure Regulation

- 3.6.2.2 EU General Data Protection Regulation

- 3.6.2.3 EU NIS2 Cybersecurity Directive

- 3.6.2.4 EU Electricity Market Design Directive

- 3.6.2.5 EU Data Act

- 3.6.3 Asia Pacific

- 3.6.3.1 India EV Charging Infrastructure Guidelines

- 3.6.3.2 India Central Electricity Authority Technical Standards

- 3.6.3.3 China Cybersecurity Law

- 3.6.3.4 China Data Security Law

- 3.6.3.5 China Personal Information Protection Law

- 3.6.3.6 China Network Data Security Regulations

- 3.6.3.7 Japan Energy Conservation Act

- 3.6.3.8 Japan Electricity Business Act

- 3.6.4 Latin America

- 3.6.4.1 Brazil General Data Protection Law

- 3.6.4.2 Brazil ANPD International Data Transfer Resolution

- 3.6.5 Middle East & Africa

- 3.6.5.1 UAE National Electric Vehicles Policy

- 3.6.5.2 UAE Personal Data Protection Law

- 3.6.5.3 UAE Information Assurance Regulation

- 3.6.5.4 UAE Electronic Transactions and Trust Services Law

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Cost breakdown analysis

- 3.11 Impact of AI and Generative AI on the Market

- 3.11.1 AI Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.11.3 Risks Limitations and Regulatory Considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.13.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Solution, 2022 - 2035 (USD Mn)

- 5.1 Key trends

- 5.2 Communication Protocol Software & Middleware

- 5.3 V2G Aggregation & Orchestration Platforms

- 5.4 Integrated V2G Software Suites

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 (USD Mn)

- 6.1 Key trends

- 6.2 Cloud-Based (SaaS)

- 6.3 On-Premise

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn)

- 7.1 Key trends

- 7.2 Frequency Regulation & Ancillary Services

- 7.3 Demand Response Management

- 7.4 Peak Shaving & Load Balancing

- 7.5 Renewable Energy Integration

- 7.6 Energy Trading & Market Participation

Chapter 8 Market Estimates & Forecast, By End User, 2022 - 2035 (USD Mn)

- 8.1 Key trends

- 8.2 Utilities & Grid Operators

- 8.3 Commercial Fleet Operators

- 8.4 Charging Point Operators (CPOs)

- 8.5 Energy Service Providers & Aggregators

- 8.6 Residential Prosumers

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Norway

- 9.3.8 Netherlands

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 ChargePoint

- 10.1.2 Driivz

- 10.1.3 Enel

- 10.1.4 Hubject

- 10.1.5 Nuvve

- 10.1.6 The Mobility House

- 10.1.7 Uplight

- 10.2 Regional Players

- 10.2.1 DREEV

- 10.2.2 ev.energy

- 10.2.3 Kaluza (OVO Energy)

- 10.2.4 OVO Energy

- 10.2.5 Virta

- 10.2.6 Virtual Peaker

- 10.2.7 WeaveGrid

- 10.3 Emerging Players

- 10.3.1 ElaadNL

- 10.3.2 Fermata Energy

- 10.3.3 FLEXECHARGE

- 10.3.4 Jedlix

- 10.3.5 Sunrun

- 10.3.6 V4Grid