PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061320

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061320

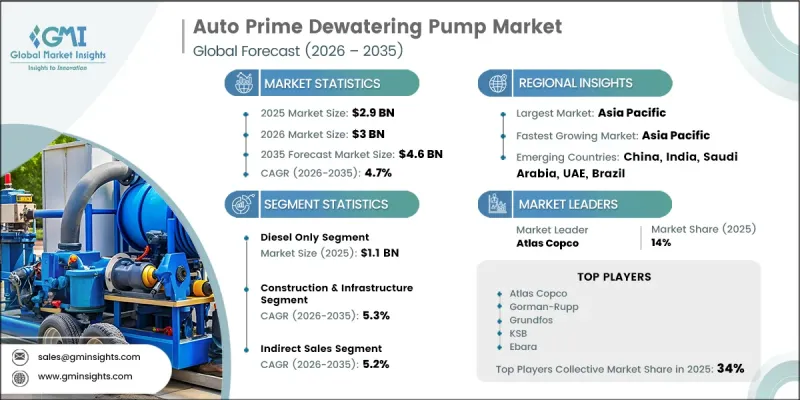

Auto Prime Dewatering Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Auto Prime Dewatering Pump Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 4.6 billion by 2035.

The global auto prime dewatering pump industry is witnessing steady expansion due to the growing requirement for advanced water management systems across multiple industrial sectors. Increasing incidents of water accumulation, emergency drainage requirements, and rising demand for efficient fluid handling solutions are creating favorable market conditions for auto-prime dewatering pumps. Expanding industrial operations and rising investments in resource extraction activities are also contributing significantly to market growth, as efficient water removal systems remain essential for uninterrupted operations. Technological progress in pump engineering, automation systems, and operational efficiency is further strengthening product adoption worldwide. Modern auto-prime dewatering pumps are designed to operate independently without requiring continuous manual intervention, making them highly preferred across industrial applications. In addition, increasing focus on reducing water wastage, improving operational productivity, and lowering maintenance requirements is supporting long-term demand. Enhanced energy efficiency, durable pump configurations, and advanced automation capabilities are also driving broader acceptance of auto-prime dewatering systems across infrastructure, industrial, and municipal operations globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 4.7% |

The global auto prime dewatering pump market is experiencing strong momentum due to increasing emphasis on efficient water control and drainage management. Advanced pump technologies are improving overall energy efficiency while simplifying maintenance procedures, which is becoming increasingly important for industries focused on operational optimization and sustainable water management practices. Growing efforts to improve water conservation and drainage efficiency have significantly accelerated the adoption of auto-prime dewatering pumps across worldwide markets. Rising demand from infrastructure development activities, industrial projects, and municipal drainage operations is also contributing to market expansion, as these systems play an essential role in maintaining continuous operational workflows and minimizing disruptions caused by water accumulation.

In 2025, the diesel-only segment accounted for USD 1.1 billion. Demand for diesel-powered systems remains strong due to their dependable performance and ability to operate effectively in locations with limited power availability. Their capability to handle intensive operational workloads also makes them highly suitable for large-scale industrial and infrastructure-related applications.

The construction and infrastructure segment held a 33.7% share in 2025 and is expected to register a CAGR of 5.3% between 2026 and 2035. Growth within this segment is being driven by rapid urban expansion and the increasing number of infrastructure development activities taking place globally. Demand for auto-prime dewatering pumps continues to rise because these systems effectively prevent water buildup at project locations, ensuring uninterrupted operations and improved construction efficiency.

United States Auto Prime Dewatering Pump Market accounted for 81% share and generated USD 596.9 million in 2025. Market growth across the country is being supported by rising infrastructure development activities and increasing investments in drainage management systems. Expanding construction operations and growing focus on disaster management solutions are contributing to higher demand for efficient dewatering technologies. In addition, recurring extreme weather conditions and rising precipitation levels are further strengthening the requirement for advanced dewatering pump systems capable of supporting emergency water removal and operational continuity.

Key companies operating in the Auto Prime Dewatering Pump Market include Atlas Copco, Ebara, Flowserve Corporation, Gorman-Rupp, Grundfos Holding, KSB, Sulzer, Cosmos Pumps, Esdhar Dewatering Solution, Logic Dewatering KSA, Rover Industry, Sky Dewatering, SPP Pumps, Thompson Pump, DEFU Pumps, HCP Pump, MBH Pumps, Remko Pumps, SB Pumps India, Solidpump, and Truflo Pumping Systems. Companies active in the auto prime dewatering pump industry are focusing on product innovation, expansion of distribution networks, and technological advancements to strengthen their market presence. Manufacturers are investing in energy-efficient pump technologies, automated monitoring systems, and durable product designs to improve operational performance and reduce maintenance costs. Strategic collaborations, regional expansion initiatives, and partnerships with infrastructure and industrial contractors are helping companies broaden their customer base and enhance market reach. Many players are also prioritizing research and development activities to introduce advanced pumping solutions with improved efficiency, higher reliability, and greater automation capabilities.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Power source

- 2.2.3 Discharge port diameter

- 2.2.4 Flow rate capacity

- 2.2.5 End use industry

- 2.2.6 Distribution channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Price trends

- 3.4.1 Historical price trend analysis

- 3.4.2 Pricing strategy by player type

- 3.5 Regulatory framework

- 3.5.1 North America: EPA Discharge Regulations, OSHA Site Safety & ANSI/HI Pump Standards

- 3.5.2 Europe: EU Machinery Directive, ATEX Directive & CE Marking Requirements

- 3.5.3 Asia Pacific: Regional Environmental Discharge Standards & Mining Safety Regulations

- 3.5.4 Middle East & Africa: ATEX / IECEx Compliance for O&G Sector & GCC GSO/SASO Standards

- 3.5.5 Global Sustainability Mandates: Emissions Targets & Noise Ordinance Impact on Diesel Auto-Prime

- 3.6 Porter's five forces analysis

- 3.7 PESTEL analysis

- 3.8 Trade Data Analysis (Based on Paid Database) (HS Code: 8413)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of traditional business models

- 3.9.2 GenAI use cases & adoption roadmap by customer segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Future market trends

- 3.11 Technology and innovation landscape

- 3.11.1 Current technological trends

- 3.11.2 Emerging technologies

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Power Source, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Diesel only

- 5.3 Electric only

- 5.4 Diesel-electric dual drive

- 5.5 Hydraulic drive

Chapter 6 Market Estimates & Forecast, By Discharge Port Diameter, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 4-Inch / 100mm

- 6.3 6-Inch / 150mm

- 6.4 8-Inch / 200mm

- 6.5 10-Inch / 250mm

- 6.6 12-Inch & above / 300mm+

Chapter 7 Market Estimates & Forecast, By Flow Rate Capacity, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Up to 200 m3/hr

- 7.3 201-400 m3/hr

- 7.4 401-600 m3/hr

- 7.5 Above 600 m3/hr

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Construction & infrastructure

- 8.3 Mining & quarrying

- 8.4 Oil, gas & refineries

- 8.5 Municipal & wastewater

- 8.6 Industrial manufacturing

- 8.7 Others (defense & military, agriculture & irrigation etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global key players

- 11.1.1 Atlas Copco

- 11.1.2 Ebara

- 11.1.3 Flowserve Corporation

- 11.1.4 Gorman-Rupp

- 11.1.5 Grundfos Holding

- 11.1.6 KSB

- 11.1.7 Sulzer

- 11.2 Regional Players

- 11.2.1 Cosmos Pumps

- 11.2.2 Esdhar Dewatering Solution

- 11.2.3 Logic Dewatering KSA

- 11.2.4 Rover Industry

- 11.2.5 Sky Dewatering

- 11.2.6 SPP Pumps

- 11.2.7 Thompson Pump

- 11.3 Emerging/Niche Specialists

- 11.3.1 DEFU Pumps

- 11.3.2 HCP Pump

- 11.3.3 MBH Pumps

- 11.3.4 Remko Pumps

- 11.3.5 SB Pumps India

- 11.3.6 Solidpump

- 11.3.7 Truflo Pumping Systems