PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061333

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061333

North America Suncare Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

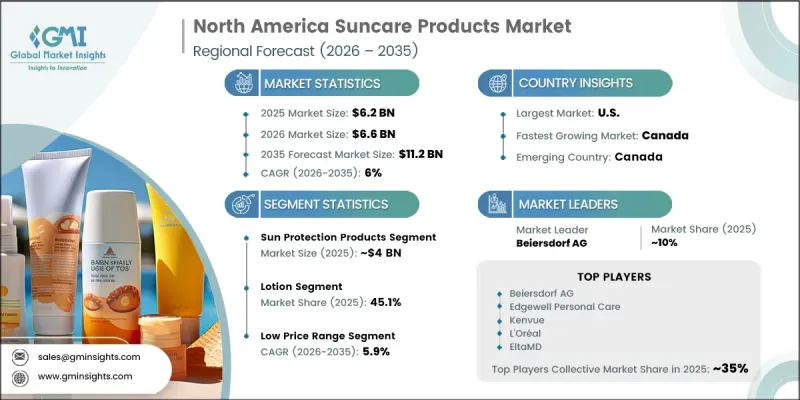

North America Suncare Products Market was valued at USD 6.2 billion in 2025 and is estimated to grow at a CAGR of 6% to reach USD 11.2 billion by 2035.

The market continues to expand as sun protection becomes a year-round personal care essential rather than a seasonal product in the region. Strong dermatological awareness and widespread public health guidance emphasizing daily SPF usage are reinforcing consumer adoption of sunscreen products. Research from the American Academy of Dermatology indicates that consistent use of SPF 30 sunscreen significantly reduces the risk of squamous cell carcinoma and melanoma, further strengthening consumer trust in preventive skincare routines. Rising product diversification is also shaping the market, with brands offering formulations tailored to sensitive skin, acne-prone skin, and anti-aging needs, improving personalization and consumer reach. Growing participation in outdoor recreational activities, tourism, and sports is further boosting demand across North America. Regions with strong travel and beach tourism activity experience pronounced seasonal consumption spikes. Increasing awareness of UV exposure risks, combined with lifestyle shifts toward preventive skincare, continues to support long-term market expansion. The availability of advanced formulations and multifunctional skincare products is further strengthening consumer adoption across both mass and premium segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.2 Billion |

| Forecast Value | $11.2 Billion |

| CAGR | 6% |

The sun protection products segment generated USD 4 billion in 2025 and is projected to grow at a CAGR of 6.3% from 2026 to 2035. This segment continues to lead the North America suncare products market as consumers increasingly understand the long-term risks of ultraviolet exposure, including premature aging, skin damage, and skin cancer. Strong demand is supported by growing emphasis on daily skincare routines that integrate sun protection as a fundamental step.

The lotion segment accounted for 45.1% share in 2025. Lotion-based sunscreens remain highly preferred due to their smooth application, even coverage, and ease of use across large skin areas. These formulations are widely adopted for their hydrating properties and compatibility with everyday skincare routines. Their versatility makes them suitable for outdoor activities, travel, and extended sun exposure, supporting consistent consumer demand across different usage occasions.

U.S. Suncare Products Market reached USD 4.7 billion in 2025 and is expected to grow at a CAGR of 5.6% from 2026 to 2035. Market growth in the country is driven by high consumer awareness regarding UV protection, strong influence of dermatological recommendations, and increasing demand for advanced skincare formulations combined with SPF benefits. Consumers are increasingly seeking lightweight, non-greasy, and multifunctional products that support daily use while offering broad-spectrum protection. The presence of leading skincare brands and dermatologist-recommended product lines further reinforces market dominance in the U.S. across both mass-market and premium categories.

Major companies operating in the North America Suncare Products Market include L'Oreal, Beiersdorf AG, Johnson & Johnson Consumer Health, Unilever, Edgewell Personal Care, Estee Lauder Companies, Shiseido Company, and Galderma. Regional players include EltaMD, Badger Company, Australian Gold, Thinksport, Colorescience, Blue Lizard, MDSolarSciences, and Knowlton Development. Emerging companies in the North America suncare products market include Supergoop!, Sun Bum, Coola LLC, Black Girl Sunscreen, and Vacation Inc. Companies operating in the North America suncare products market are adopting multiple strategies to strengthen their competitive position and expand consumer reach. A key focus is on product innovation, with brands developing advanced formulations that combine sun protection with skincare benefits such as hydration, anti-aging, and skin tone improvement. Manufacturers are also expanding dermatologist-backed and clinically tested product portfolios to build consumer trust and credibility. Increasing investment in clean beauty, reef-safe formulations, and sustainable packaging is helping brands align with environmentally conscious consumer preferences. Companies are strengthening distribution networks through e-commerce platforms, retail partnerships, and direct-to-consumer channels to improve accessibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Product type

- 2.2.3 Product formulation

- 2.2.4 Form

- 2.2.5 Price

- 2.2.6 Consumer group

- 2.2.7 Application

- 2.2.8 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Raw material suppliers

- 3.1.2.1 UV filter manufacturers

- 3.1.2.2 Emollient & moisturizer suppliers

- 3.1.2.3 Packaging material providers (tubes, bottles, pumps)

- 3.1.2.4 Fragrance & additive suppliers

- 3.1.3 Brand owners & product developers

- 3.1.4 Distribution & logistics layer

- 3.1.5 Retail & End-Channel partners

- 3.1.6 Value addition at each stage

- 3.1.7 Profit margin

- 3.1.8 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising awareness of skin cancer & UV protection

- 3.2.1.2 Increasing outdoor recreational activities & tourism

- 3.2.1.3 Growing demand for multi-functional beauty products

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Stringent regulatory approval processes for new ingredients

- 3.2.2.2 Environmental concerns over chemical UV filters

- 3.2.3 Opportunities

- 3.2.3.1 Innovation in mineral & hybrid formulations

- 3.2.3.2 Blue light protection & anti-pollution product development

- 3.2.3.3 Sustainable & reef-safe sunscreen demand

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 UV filter technology evolution

- 3.5.2 Formulation technology breakthroughs

- 3.5.3 Delivery system innovations

- 3.5.4 Multi-functional product development

- 3.5.5 Sustainability & clean beauty innovations

- 3.5.6 Digital & smart suncare technologies

- 3.5.7 Emerging technology frontiers

- 3.6 Price trends

- 3.6.1 By product

- 3.6.2 Historical price trend analysis

- 3.6.3 Price pricing strategy by player type (premium / value / cost-plus)

- 3.6.4 Regional price variation analysis

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.1.1 US

- 3.7.1.1.1 Consumer Product Safety Commission (CPSC) 16 Code of Federal Regulations (CFR) part 1512

- 3.7.1.1.2 FDA OTC Monograph System (21 CFR 352)

- 3.7.1.1.3 GRASE (Generally Recognized as Safe & Effective) Status

- 3.7.1.1.4 New Ingredient Approval Pathway (SUNDIA Act Implications)

- 3.7.1.1.5 SPF Testing Requirements (FDA Final Rule 2011/2019)

- 3.7.1.1.6 Labeling & Claims Regulations (Broad Spectrum, Water Resistance)

- 3.7.1.1.7 State-Level Bans

- 3.7.1.2 Canada

- 3.7.1.2.1 International Organization for Standardization (ISO) 4210

- 3.7.1.2.2 NPN (Natural Product Number) Requirements

- 3.7.1.2.3 Pre-Market Authorization Process

- 3.7.1.2.4 SPF & UVA Testing Standards

- 3.7.1.1 US

- 3.7.1 North America

- 3.8 Supply chain analysis

- 3.8.1 Raw material sourcing landscape

- 3.8.2 Manufacturing footprint

- 3.8.3 Logistics & distribution networks

- 3.8.4 Supply chain resilience & risk factors

- 3.8.5 Supply chain sustainability initiatives

- 3.9 Trade statistics (driven by paid database) (HS code- 33049990)

- 3.9.1 Major importing countries

- 3.9.2 Major exporting countries

- 3.9.3 Import/export volume & value trends

- 3.9.4 Key trade corridors & tariff impact

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.11.1 Channel coverage by region & format (modern vs. Traditional trade)

- 3.11.2 Last-mile infrastructure gaps & emerging channel shifts

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Consumer buying behavior analysis

- 3.14.1 Purchase Decision-Making Process

- 3.14.2 Demographic trends

- 3.14.3 Factors affecting buying decisions

- 3.14.4 Consumer product adoption

- 3.14.5 Preferred distribution channel

- 3.14.6 Brand preference

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Sun protection products

- 5.2.1 Daily wear sunscreen (SPF 15-30)

- 5.2.2 High protection sunscreens (SPF 50+)

- 5.2.3 Tinted sunscreens & bb/cc creams with SPF

- 5.3 After sun products

- 5.3.1 Cooling gels & lotions

- 5.3.2 Repair & hydration treatments

- 5.3.3 Anti-aging after-sun care

- 5.4 Self-tanning products

- 5.4.1 Gradual tanners

- 5.4.2 Instant bronzers

- 5.4.3 Tanning mousses & sprays

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Product Formulation, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Chemical sunscreens

- 6.3 Mineral sunscreens

- 6.4 Hybrid formulations

Chapter 7 Market Estimates & Forecast, By Form, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Lotion

- 7.3 Spray

- 7.4 Gel

- 7.5 Stick

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Price, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By Consumer Group, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Men

- 9.3 Women

- 9.4 Kids

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Body

- 10.3 Face

- 10.4 Lip

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 Online

- 11.2.1 E-commerce websites

- 11.2.2 Company-owned websites

- 11.3 Offline

- 11.3.1 Hypermarkets & supermarkets

- 11.3.2 Specialty stores

- 11.3.3 Pharmacies & drugstores

- 11.3.4 Others

Chapter 12 Market Estimates & Forecast, By Country, 2022 - 2035, (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 U.S.

- 12.3 Canada

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 L'Oreal

- 13.1.2 Beiersdorf AG

- 13.1.3 Johnson & Johnson Consumer Health

- 13.1.4 P&G

- 13.1.5 Shiseido Company

- 13.1.6 Unilever

- 13.1.7 Kao Corporation

- 13.1.8 Edgewell Personal Care

- 13.1.9 Estee Lauder Companies

- 13.1.10 Amorepacific Corporation

- 13.1.11 Coty Inc.

- 13.2 Regional players

- 13.2.1 Pierre Fabre Group

- 13.2.2 ISDIN

- 13.2.3 Rohto Pharmaceutical

- 13.2.4 Lotus Herbals

- 13.2.5 Cancer Council

- 13.2.6 Grupo Boticario

- 13.2.7 Genomma Lab Internacional

- 13.3 Emerging Players

- 13.3.1 Supergoop!

- 13.3.2 Sun Bum

- 13.3.3 Bondi Sands

- 13.3.4 Coola LLC