PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061344

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061344

Aircraft Auxiliary Power Unit (APU) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

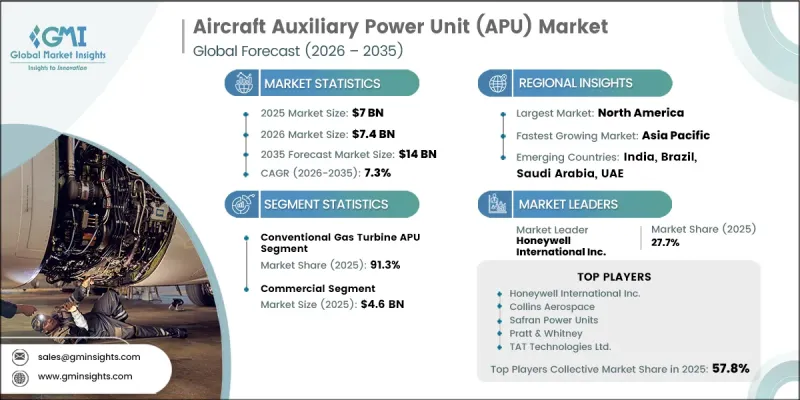

The Global Aircraft Auxiliary Power Unit Market accounted for USD 7 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 14 billion by 2035.

Growth across the aircraft auxiliary power unit industry is being fueled by continuous fleet modernization, increasing aircraft operational cycles, and higher maintenance requirements linked to rising flight frequencies. Growing investments in advanced onboard power technologies are also supporting industry expansion as airlines and defense operators prioritize efficient and reliable auxiliary systems. The adoption of hybrid-electric and fuel-cell-powered APUs is creating additional revenue opportunities due to their enhanced efficiency and premium pricing compared to traditional turbine-based systems. Demand is also benefiting from the transition toward more-electric aircraft platforms, where modern auxiliary power solutions are becoming essential components in both retrofit and factory-installed applications. Expanding global air traffic, rising aircraft production, and increasing preference for self-sufficient onboard power capabilities continue to strengthen long-term market demand across commercial and military aviation sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7 Billion |

| Forecast Value | $14 Billion |

| CAGR | 7.3% |

The aircraft auxiliary power unit industry continues to gain momentum due to the steady rise in worldwide aircraft deliveries, which is increasing the number of active aircraft equipped with onboard power systems across both defense and commercial aviation. The expanding fleet base is driving strong line-fit demand while also generating long-term servicing and overhaul requirements as aircraft accumulate operational hours. In addition, airlines are increasingly prioritizing independent onboard power generation to reduce reliance on airport-based support infrastructure during turnaround procedures. This trend is creating stronger procurement demand at regional airports and developing aviation hubs where ground support capabilities remain limited. Greater operational flexibility, improved turnaround efficiency, and reduced dependence on airport infrastructure are further contributing to market growth.

The hybrid-electric APU segment is forecast to witness a CAGR of 15.3% throughout 2035. Growing environmental regulations and the development of next-generation aircraft programs are encouraging airlines and operators to adopt more energy-efficient onboard power technologies. Increasing advancements in electric propulsion systems and integrated aircraft power architectures are further accelerating adoption. Long-term industry potential is expected to remain strong as manufacturers continue to focus on sustainable aviation technologies and low-emission aircraft solutions.

The commercial segment generated USD 4.6 billion in 2025. Segment growth is primarily supported by extensive global commercial aircraft fleets and recurring maintenance, repair, and overhaul activities. High aircraft utilization rates continue to create stable aftermarket demand for auxiliary power systems and replacement components. Ongoing airline network expansion, rising passenger traffic, and increasing route frequencies are also contributing to sustained demand across the commercial aviation sector. The large installed fleet base and consistent servicing requirements continue to reinforce the segment's leading market position.

North America Aircraft Auxiliary Power Unit Market held a 37.4% share in 2025. The regional market continues to benefit from high aircraft usage rates and strict maintenance regulations that require structured APU inspection and overhaul cycles. Consistent aircraft operations across commercial and regional aviation fleets are supporting strong aftermarket demand throughout the region. At the same time, continuous aircraft production and new fleet deliveries are strengthening OEM installation demand for advanced auxiliary power systems. The presence of established aerospace manufacturers, extensive aviation infrastructure, and ongoing technological investments further support regional market expansion.

Key companies operating in the Global Aircraft Auxiliary Power Unit Market include Honeywell International Inc., Pratt & Whitney, Safran Power Units, Collins Aerospace, Hamilton Sundstrand, PBS Aerospace Inc., Aerosila JSC, Klimov, TAT Technologies Ltd., Technodinamika, Motor Sich JSC, Microturbo, Jenoptik AG, Dewey Electronics Corporation, and Kinetics Ltd. Companies operating in the aircraft auxiliary power unit market are focusing on advanced product innovation, strategic collaborations, and long-term supply agreements to strengthen their market position. Leading manufacturers are investing heavily in hybrid-electric and fuel-efficient APU technologies to align with evolving aviation sustainability targets and next-generation aircraft requirements. Many industry participants are expanding their maintenance, repair, and overhaul capabilities to capture growing aftermarket revenue opportunities generated by increasing aircraft utilization rates. Strategic partnerships with aircraft OEMs and airline operators are also helping companies secure long-term installation and servicing contracts. In addition, market players are prioritizing geographic expansion, production capacity enhancement, and technology integration to improve operational efficiency and broaden customer reach. Continuous investments in lightweight materials, digital monitoring systems, and low-emission power solutions are further enabling companies to strengthen their competitive presence within the global aircraft auxiliary power unit industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology type trends

- 2.2.2 Aircraft platform trends

- 2.2.3 Power rating trends

- 2.2.4 Sales channel trends

- 2.2.5 End users trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of global aircraft fleet

- 3.2.1.2 Increasing aircraft modernization and retrofit programs

- 3.2.1.3 Growth in air passenger traffic

- 3.2.1.4 Expansion of aircraft maintenance, repair, and overhaul (MRO) activities

- 3.2.1.5 Rising focus on aircraft operational efficiency and ground support optimization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and complexity of advanced APU systems

- 3.2.2.2 Supply chain disruptions and component availability challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of hybrid-electric and more-electric aircraft architectures

- 3.2.3.2 Advancements in digital APU monitoring and predictive maintenance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology Type, 2022 - 2035 (USD Million)

- 5.1 Key trend

- 5.2 Conventional gas turbine APUs

- 5.3 Hybrid-electric APUs

- 5.4 Electric/battery-powered APUs

- 5.5 Fuel cell-based APUs

- 5.6 By End Users

Chapter 6 Market Estimates and Forecast, By Aircraft Platform, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Commercial aviation

- 6.2.1 Narrow-body aircraft

- 6.2.2 Wide-body aircraft

- 6.2.3 Regional jets

- 6.3 Military aviation

- 6.3.1 Fighter & combat aircraft

- 6.3.2 Transport & tanker aircraft

- 6.3.3 Special mission platforms

- 6.4 Business & general aviation

- 6.4.1 Business jets

- 6.4.2 Light general aviation aircraft

- 6.5 Rotorcraft

- 6.5.1 Commercial helicopters

- 6.5.2 Military helicopters

- 6.6 Unmanned aerial vehicles (UAVs)

- 6.6.1 Medium-altitude long-endurance (MALE)

- 6.6.2 High-altitude long-endurance (HALE)

Chapter 7 Market Estimates and Forecast, By Power Rating, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Low power APUs (<50 kVA)

- 7.3 Medium power APUs (50-150 kVA)

- 7.4 High power APUs (>150 kVA)

Chapter 8 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 OEM (line-fit/new installation)

- 8.3 Aftermarket

Chapter 9 Market Estimates and Forecast, By End Users, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Military

- 9.3 Commercial

- 9.4 Civil & government

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Honeywell International Inc.

- 11.1.2 Collins Aerospace

- 11.1.3 Safran Power Units

- 11.1.4 Pratt & Whitney

- 11.1.5 TAT Technologies Ltd.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Hamilton Sundstrand

- 11.2.1.2 Dewey Electronics Corporation

- 11.2.2 Asia Pacific

- 11.2.2.1 Aerosila JSC

- 11.2.2.2 Klimov

- 11.2.2.3 Motor Sich JSC

- 11.2.2.4 Technodinamika

- 11.2.3 Europe

- 11.2.3.1 PBS Aerospace Inc.

- 11.2.3.2 Microturbo

- 11.2.3.3 Jenoptik AG

- 11.2.4 Middle East & Africa

- 11.2.4.1 Kinetics Ltd.

- 11.2.1 North America