PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061348

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061348

Marine Gensets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

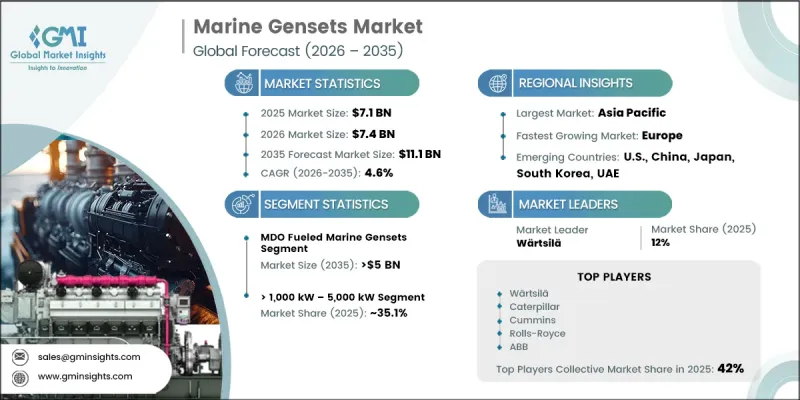

The Global Marine Gensets Market was valued at USD 7.1 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 11.1 billion by 2035.

The market is witnessing steady growth driven by the expansion of global seaborne trade supported by rising industrialization, urbanization, and infrastructure development in emerging economies. Increasing movement of commodities such as crude oil, minerals, chemicals, and agricultural goods is strengthening demand for reliable onboard power systems. Continuous investment in shipping fleets and port infrastructure is further supporting market expansion. Marine gensets are widely used onboard vessels to generate electrical power for essential systems including lighting, navigation, and climate control. Growing maritime tourism, rising disposable incomes, and higher spending on leisure travel are also contributing to increased demand for passenger vessels and recreational boating solutions across global waters.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.1 Billion |

| Forecast Value | $11.1 Billion |

| CAGR | 4.6% |

The MDO-fueled marine gensets segment is projected to reach USD 5 billion by 2035. Growth in this segment is supported by tightening environmental regulations aimed at reducing emissions from marine operations. Operators are increasingly selecting fuel-efficient and dependable solutions that comply with global emission standards while maintaining performance in high and medium-speed applications. Expansion of international maritime trade, particularly in developing regions, is also reinforcing demand for efficient marine power systems. Favorable shipping industry conditions and modernization of fleets are further enhancing the adoption of advanced genset technologies.

The > 1,000 kW - 5,000 kW power-rated segment accounted for 35.1% share in 2025. Demand in this category is driven by expanding recreational boating activities and the growing maritime tourism industry. Increasing adoption of marine vessels such as yachts, tugboats, and similar high-capacity craft is strengthening the requirement for reliable onboard power systems. Rising disposable incomes and infrastructure development are further encouraging investment in marine leisure activities, supporting long-term market growth.

U.S. Marine Gensets Market was valued at USD 724.8 million in 2025. Market expansion is supported by ongoing technological advancements, including hybrid propulsion systems and integration of renewable energy solutions aimed at improving vessel efficiency and sustainability. Strong demand for offshore vessels, yachts, and tugboats, combined with supportive policies for cleaner marine technologies, is further driving growth. Continuous shipbuilding activity across commercial and defense segments is also contributing to sustained demand for advanced marine power generation systems.

Key companies operating in the Global Marine Gensets Market include Caterpillar, Cummins, Wartsila, Rolls-Royce, Volvo Penta, Mitsubishi Heavy Industries, ABB, YANMAR HOLDINGS, DEUTZ AG, Scania, Nidec Corporation, Kirloskar, Fischer Panda, Anglo Belgian Corporation, AKSA POWER GENERATION, Everllence, GlobalTec Solutions, Mase Generators of North America, Societe Internationale des Moteurs Baudouin, Sole Advance, and Deere & Company. Companies in the marine gensets market are focusing on improving fuel efficiency and reducing emissions through advanced engine technologies and hybrid system integration. Many players are investing in R&D to develop compact, high-performance gensets suitable for a wide range of vessel types. Strategic partnerships with shipbuilders and marine operators are strengthening product deployment and customization capabilities. Manufacturers are also expanding their offerings to include hybrid and multi-fuel systems to meet evolving environmental regulations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Fuel trends

- 2.1.3 Power rating trends

- 2.1.4 Application trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of marine gensets

- 3.8 Emerging opportunities & trends

- 3.9 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

- 3.11 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.11.1 By region (Driven by Primary Research)

- 3.11.2 By power rating (Driven by Primary Research)

- 3.12 Trade data analysis (Driven by Primary Research)

- 3.12.1 Import/export value trends (Driven by Primary Research)

- 3.12.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Capacity by region & key producer (Driven by Primary Research)

- 3.13.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.14 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.14.1 AI-Driven production optimization (Driven by Primary Research)

- 3.14.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 MDO

- 5.3 MGO

- 5.4 LNG

- 5.5 Hybrid

- 5.6 Others

Chapter 6 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 ≤ 1,000 kW

- 6.3 > 1,000 kW - 5,000 kW

- 6.4 > 5,000 kW - 10,000 kW

- 6.5 > 10,000 kW - 20,000 kW

- 6.6 > 20,000 kW

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Merchant

- 7.2.1 Container vessels

- 7.2.2 Bulk carriers

- 7.2.3 RO-RO

- 7.2.4 Others

- 7.3 Offshore

- 7.3.1 Drilling RIGS & ships

- 7.3.2 Anchor handling vessels

- 7.3.3 Offshore support vessels

- 7.3.4 Floating production units

- 7.3.5 Platform supply vessels

- 7.4 Cruise & Ferry

- 7.4.1 Cruise vessels

- 7.4.2 Passenger vessels

- 7.4.3 Passenger/cargo vessels

- 7.4.4 Others

- 7.5 Navy

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 Norway

- 8.3.5 France

- 8.3.6 Russia

- 8.3.7 Denmark

- 8.3.8 Netherlands

- 8.3.9 Belgium

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Vietnam

- 8.4.7 Singapore

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Iran

- 8.5.4 Angola

- 8.5.5 Egypt

- 8.5.6 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Mexico

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 AKSA POWER GENERATION

- 9.3 Anglo Belgian Corporation

- 9.4 Caterpillar

- 9.5 Cummins

- 9.6 Deere & Company

- 9.7 DEUTZ AG

- 9.8 Everllence

- 9.9 Fischer Panda

- 9.10 GlobalTec Solutions

- 9.11 Kirloskar

- 9.12 Mase Generators of North America

- 9.13 Mitsubishi Heavy Industries

- 9.14 Nidec Corporation

- 9.15 Rehlko

- 9.16 Rolls-Royce

- 9.17 Scania

- 9.18 Societe Internationale des Moteurs Baudouin

- 9.19 Sole Advance

- 9.20 Volvo Penta

- 9.21 Wartsila

- 9.22 YANMAR HOLDINGS