PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061367

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061367

Cold Chain Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

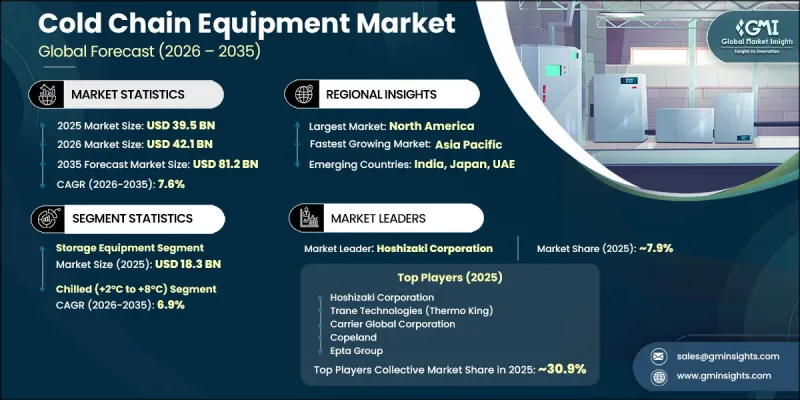

The Global Cold Chain Equipment Market was valued at USD 39.5 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 81.2 billion by 2035.

The market is witnessing strong expansion owing to rising demand for temperature-controlled storage and transportation across pharmaceuticals, biotechnology, healthcare, and food and beverage industries. The increasing global consumption of biologics, vaccines, frozen foods, and temperature-sensitive pharmaceutical products is significantly strengthening the need for advanced refrigeration systems and controlled logistics infrastructure. Cold chain equipment plays a crucial role in ensuring product safety by maintaining precise temperature conditions across end-to-end supply chains, thereby minimizing spoilage and ensuring regulatory compliance. The rapid expansion of organized retail networks, pharmaceutical distribution systems, and e-commerce grocery platforms is further reinforcing market growth. At the same time, the industry is undergoing a major technological shift with the integration of IoT-enabled monitoring systems, smart sensors, and real-time tracking solutions that improve visibility and operational control. Automation adoption is also rising, allowing companies to enhance efficiency and reduce product loss risks. Increasing regulatory pressure regarding food safety standards and pharmaceutical handling requirements continues to encourage investments in advanced cold chain infrastructure. Additionally, the expansion of biologics manufacturing and global vaccine distribution programs is further accelerating demand for reliable and scalable cold chain systems across developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $39.5 Billion |

| Forecast Value | $81.2 Billion |

| CAGR | 7.6% |

The storage equipment segment accounted for USD 18.3 billion in 2025 and is expected to grow at a CAGR of 5.4% from 2026 to 2035. This segment leads the market due to rising investments in refrigerated warehouses, cold rooms, industrial cooling systems, and pharmaceutical-grade storage facilities. These solutions are essential for preserving temperature stability over long durations across applications such as food processing, vaccine storage, biologics preservation, and pharmaceutical inventory management. Continued expansion of organized cold storage networks and the growing global frozen food supply chain are further strengthening segment performance.

The chilled temperature range segment (2°C to 8°C) held 37.9% share in 2025 and is projected to grow at a CAGR of 6.9% through 2035. This segment remains highly important due to its extensive use in dairy products, vaccines, fresh produce, biologics, and temperature-sensitive medicines. Chilled systems help maintain product integrity while reducing deterioration risks during storage and transportation. Rising distribution of biologics and processed food products requiring stable refrigerated environments continues to drive consistent demand for chilled cold chain solutions.

United States Cold Chain Equipment Market reached USD 10.9 billion in 2025 and is forecast to grow at a CAGR of 6.8% through 2035. Growth in the country is supported by strong pharmaceutical production capabilities, advanced healthcare logistics systems, and highly developed refrigerated food distribution networks. Increasing demand for vaccines, biologics, frozen foods, and temperature-sensitive medicines is encouraging greater investment in cold storage infrastructure and transport refrigeration technologies. The market is also benefiting from the growing adoption of energy-efficient cooling systems, automated warehouses, and IoT-based monitoring platforms that enhance operational performance and regulatory adherence.

Major players operating in the Global Cold Chain Equipment Industry Include Carrier Global Corporation, Trane Technologies, Daikin Industries Ltd., Johnson Controls International PLC, Copeland, Danfoss A/S, Dover Corporation (Hillphoenix), Liebherr Group, Blue Star Limited, Voltas Limited, CIMC (China International Marine Containers), Arneg Group, Hoshizaki Corporation, Epta Group, ThermoSafe, Peli BioThermal, Cold Chain Technologies, va-Q-tec AG, Panasonic Corporation, Haier Biomedical, and Frigoglass S.A. Companies in the cold chain equipment market are focusing on strengthening their position through digital transformation, especially by integrating IoT-based tracking systems, smart temperature sensors, and cloud-enabled monitoring platforms. They are investing heavily in energy-efficient refrigeration technologies to reduce operational costs while meeting sustainability goals. Strategic partnerships with logistics providers and pharmaceutical firms are expanding their service networks and improving distribution efficiency. Many players are also prioritizing automation in warehousing and transportation to enhance accuracy and reduce human error. Product innovation, particularly in modular and scalable cold storage systems, is helping companies address diverse end-user requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Temperature range

- 2.2.4 Application

- 2.2.5 Mode of operation

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for temperature-sensitive transportation and storage solutions

- 3.2.1.2 Expansion of biologics, vaccines, and temperature-sensitive pharmaceutical products

- 3.2.1.3 Growing investment in organized cold storage infrastructure and food logistics

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High installation and operational costs associated with advanced refrigeration systems

- 3.2.2.2 Energy consumption and maintenance complexity of cold chain infrastructure

- 3.2.3 Opportunities

- 3.2.3.1 Increasing adoption of IoT-enabled monitoring and automation technologies

- 3.2.3.2 Expansion of pharmaceutical cold chain infrastructure across emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.10 Trade data analysis (HS Code 8418 for active refrigerating/freezing machinery and HS Code 9406 for insulated cold room structures) (driven by paid database)

- 3.10.1 Import/export volume and value trends (driven by paid database)

- 3.10.2 Key trade corridors and tariff impact (driven by paid database)

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases and adoption roadmap by segment

- 3.11.3 Risks, limitations and regulatory considerations

- 3.12 Capacity and production landscape (driven by primary research)

- 3.12.1 Installed capacity by region and key producer (driven by primary research)

- 3.12.2 Capacity utilization rates and expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Storage Equipment

- 5.3 Transportation Equipment

- 5.4 Monitoring & Control Systems

- 5.5 Temperature-Controlled Packaging

Chapter 6 Market Estimates & Forecast, By Temperature Range, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Controlled Ambient (+15°C to +25°C)

- 6.3 Chilled (+2°C to +8°C)

- 6.4 Frozen (-18°C to -25°C)

- 6.5 Cryogenic (Below -80°C)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Food & Beverages

- 7.2.1 Fruits & Vegetables

- 7.2.2 Dairy Products

- 7.2.3 Meat, Fish & Seafood

- 7.2.4 Processed Food & Ready-to-Eat Meals

- 7.2.5 Bakery & Confectioneries

- 7.2.6 Others

- 7.3 Pharmaceuticals

- 7.3.1 Vaccines

- 7.3.2 Biologics & Biosimilars

- 7.3.3 Temperature-Sensitive APIs

- 7.3.4 Clinical Trial Materials

- 7.4 Healthcare

- 7.4.1 Blood Products & Plasma

- 7.4.2 Organs & Tissue for Transplantation

- 7.4.3 Medical Supplies & Reagents

- 7.5 Chemicals

- 7.5.1 Specialty Chemicals

- 7.5.2 Volatile Compounds

- 7.6 Biotechnology

- 7.6.1 Cell & Gene Therapies

- 7.6.2 Research Samples & Biobanking

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Mode of Operation, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Active Systems

- 8.3 Passive Systems

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct Sales

- 9.3 Indirect Sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Top Global Players

- 11.1.1 Carrier Global Corporation

- 11.1.2 Daikin Industries Ltd.

- 11.1.3 Trane Technologies

- 11.1.4 Copeland

- 11.1.5 Johnson Controls International PLC

- 11.1.6 Danfoss A/S

- 11.1.7 Dover Corporation (Hillphoenix)

- 11.2 Regional Champions

- 11.2.1 Blue Star Limited

- 11.2.2 Voltas Limited

- 11.2.3 CIMC (China International Marine Containers)

- 11.2.4 Liebherr Group

- 11.2.5 Hoshizaki Corporation

- 11.2.6 Arneg Group

- 11.2.7 Epta Group

- 11.3 Emerging & Specialized Players

- 11.3.1 ThermoSafe

- 11.3.2 Peli BioThermal

- 11.3.3 Cold Chain Technologies

- 11.3.4 va-Q-tec AG

- 11.3.5 Panasonic Corporation

- 11.3.6 Haier Biomedical

- 11.3.7 Frigoglass S.A.