PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061371

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061371

North America Electric Zero Turn Mower Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

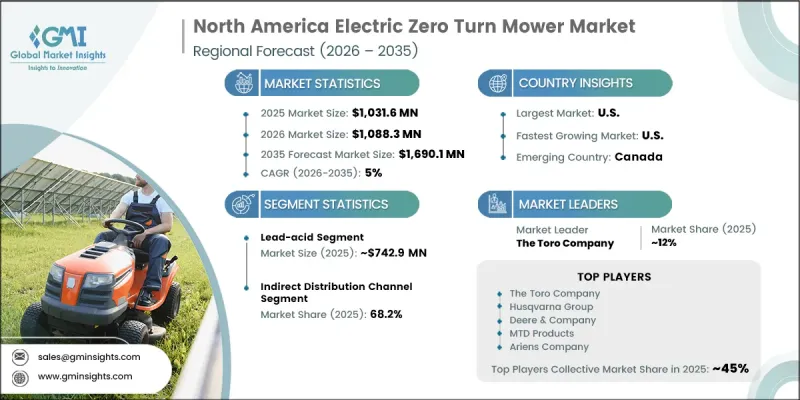

North America Electric Zero Turn Mower Market was valued at USD 1,031.6 million in 2025 and is estimated to grow at a CAGR of 5% to reach USD 1,690.1 million by 2035.

The market is witnessing steady growth due to increasingly strict environmental regulations focused on reducing emissions and noise pollution from outdoor power equipment. Growing adoption of sustainable landscaping solutions across commercial and residential sectors is significantly supporting demand for electric zero-turn mowers throughout North America. The expansion of professional landscaping services is also contributing to market growth, particularly across large outdoor properties and commercial maintenance applications. Businesses are increasingly transitioning toward electric mowing equipment to lower operating expenses, minimize maintenance requirements, and align with sustainability goals. Rising investments in green infrastructure and outdoor space enhancement projects are further accelerating the adoption of advanced lawn care technologies. In addition, continuous advancements in battery technology are improving the overall performance and practicality of electric zero-turn mowers. Developments in energy storage systems are enabling longer operating durations, improved charging efficiency, and enhanced energy management, making electric models more competitive with conventional fuel-powered alternatives. These technological improvements continue to strengthen the long-term growth outlook for the North America electric zero turn mower industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1,031.6 Million |

| Forecast Value | $1,690.1 Million |

| CAGR | 5% |

The lead-acid battery segment generated USD 742.9 million in 2025 and is anticipated to grow at a CAGR of 4.5% from 2026 to 2035. Strong growth within this segment is primarily supported by the affordability and broad availability of lead-acid battery systems, making them highly attractive to cost-conscious consumers and smaller landscaping operators. Compared to alternative battery technologies, lead-acid batteries offer lower upfront equipment costs, helping reduce the total purchase price of electric zero-turn mowers. This pricing advantage continues to encourage adoption among entry-level users and businesses seeking economical lawn maintenance solutions.

The indirect distribution channel accounted for 68.2% share, and is expected to grow at a CAGR of 4.8% through 2035. Manufacturers continue to rely heavily on extensive dealer networks, distributors, retail outlets, and online sales platforms to strengthen market penetration across both urban and rural areas. These intermediary channels play a major role in influencing purchasing decisions by offering product guidance, financing assistance, technical support, and after-sales services. Such support remains especially important for high-value landscaping equipment, helping manufacturers improve customer engagement and expand market reach across diverse buyer segments.

U.S. Electric Zero Turn Mower Market reached USD 927 million in 2025, and is projected to grow at a CAGR of 5.1% between 2026 and 2035. The country continues to lead regional demand due to strong environmental policies encouraging the transition toward low-emission outdoor equipment. Regulatory measures focused on reducing reliance on traditional fuel-powered lawn equipment are accelerating the shift toward electric alternatives throughout the U.S. market. In addition, the country remains at the forefront of technological innovation and product development within the electric landscaping equipment sector. Manufacturers are actively investing in advanced battery systems, smart connectivity solutions, intelligent automation technologies, and precision control systems to improve operational performance and attract both residential and commercial users.

Major companies operating in the North America Electric Zero Turn Mower Market include The Toro Company, John Deere, Husqvarna Group, Honda Power Equipment, AriensCo, Briggs & Stratton, Techtronic Industries (Ryobi), Doosan Bobcat, The Grasshopper Company, Bad Boy Mowers, Metalcraft of Mayville, MTD Products, Stanley Black & Decker, STIHL, Generac Holdings, Greenworks Commercial, Chervon, Globe Tools, Encore Power Equipment, and Mean Green Products. Companies operating in the North America electric zero turn mower industry are implementing several strategic initiatives to strengthen their market position and improve competitive advantage. Leading manufacturers are investing heavily in battery innovation, smart technologies, and automation systems to enhance equipment efficiency, runtime, and overall user experience. Many companies are also focusing on expanding product portfolios with environmentally friendly and energy-efficient models to align with evolving sustainability regulations and customer preferences. Strategic partnerships with dealers, distributors, and online retail platforms are helping businesses strengthen regional market penetration and improve customer accessibility. In addition, companies are emphasizing after-sales support, financing programs, and maintenance services to enhance customer satisfaction and brand loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Battery type

- 2.2.3 Cutting width

- 2.2.4 Battery capacity

- 2.2.5 Yard space

- 2.2.6 End use

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent emission and noise regulations

- 3.2.1.2 Expansion of commercial landscaping industry

- 3.2.1.3 Advancements in battery technology

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial purchase cost

- 3.2.2.2 Performance concerns in heavy-duty applications

- 3.2.3 Opportunities

- 3.2.3.1 Advancements in battery technology

- 3.2.3.2 Integration of smart and autonomous technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Trade data analysis (HS Code 8433.11)

- 3.7.1 Import/export volume & value trends

- 3.7.2 Key trade corridors & tariff impact

- 3.7.3 Cross-border e-commerce flows

- 3.8 Pricing analysis

- 3.8.1 Historical price trend analysis (driven by primary research)

- 3.8.2 Pricing strategy by player type (premium / value / mass market)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behavior analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Battery Type, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Lithium-ion

- 5.3 Lead-acid

Chapter 6 Market Estimates & Forecast, By Cutting Width, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Less than 50 inches

- 6.3 50 to 60 inches

- 6.4 More than 60 inches

Chapter 7 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Up to 18 kWh

- 7.3 18 - 25 kWh

- 7.4 26 -35 kWh

- 7.5 More than 35 kWh

Chapter 8 Market Estimates & Forecast, By Yard Space, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Small yard (less than 1 acre)

- 8.3 Medium yard (1 to 3 acres)

- 8.4 Large yard (More than 3 acres)

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.3.1 Parks & recreation departments

- 9.3.2 Public facilities & government properties

- 9.3.3 Schools & universities

- 9.3.4 Golf courses & sports fields

- 9.3.5 Golf courses

- 9.3.6 Athletic fields & sports complexes

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Country, 2022 - 2035, (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 U.S.

- 11.3 Canada

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 The Toro Company

- 12.1.2 John Deere

- 12.1.3 Husqvarna Group

- 12.1.4 Honda Power Equipment

- 12.1.5 AriensCo

- 12.1.6 Briggs & Stratton

- 12.1.7 Techtronic Industries (Ryobi)

- 12.2 Regional Champions

- 12.2.1 Doosan Bobcat

- 12.2.2 The Grasshopper Company

- 12.2.3 Bad Boy Mowers

- 12.2.4 Metalcraft of Mayville

- 12.2.5 MTD Products

- 12.2.6 Stanley Black & Decker

- 12.2.7 STIHL

- 12.3 Emerging Players

- 12.3.1 Generac Holdings

- 12.3.2 Greenworks Commercial

- 12.3.3 Chervon

- 12.3.4 Globe Tools

- 12.3.5 Encore Power Equipment

- 12.3.6 Mean Green Products