PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071368

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071368

Zero Turn Mower Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

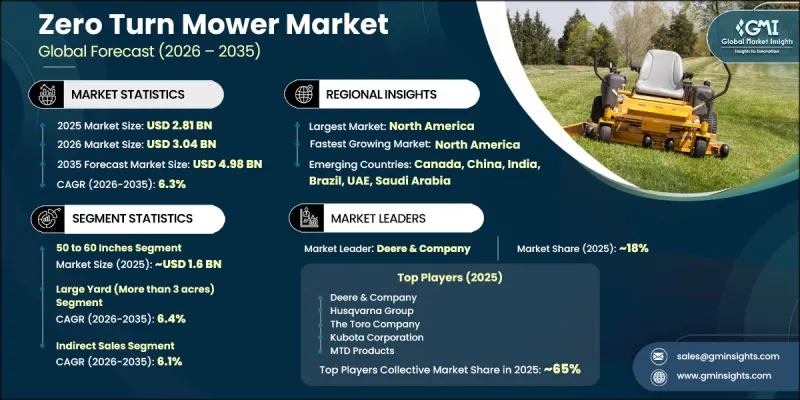

The Global Zero Turn Mower Market was valued at USD 2.81 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 4.98 billion by 2035.

The market is witnessing expansion due to the rising need for efficient and time-saving lawn maintenance solutions across residential, commercial, and institutional applications. Zero turn mowers are increasingly preferred over conventional mowing equipment because they deliver higher operational speed, improved maneuverability, and greater cutting precision. These advantages allow users to manage large green spaces more efficiently while achieving consistent and high-quality results. The growing demand for professional landscaping and grounds maintenance services is further accelerating adoption across multiple end-use sectors. Urban development trends, rising disposable incomes, and increasing focus on outdoor aesthetics are also contributing to higher equipment demand. Additionally, technological advancements are reshaping the industry through the integration of smart features such as GPS-enabled navigation, semi-autonomous operation, telematics solutions, and mobile application-based controls. The shift toward electrified and intelligent outdoor equipment is further strengthening market growth as end users increasingly prioritize performance, convenience, and sustainability in lawn care operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.81 Billion |

| Forecast Value | $4.98 Billion |

| CAGR | 6.3% |

The zero turn mower market is also benefiting from the expansion of commercial landscaping services and the increasing emphasis on maintaining well-designed outdoor environments. Demand is rising across residential communities, commercial properties, municipal spaces, and recreational facilities, all of which require efficient and high-performance mowing solutions. Technological integration continues to play a key role in market evolution, with manufacturers introducing advanced systems that enhance operational efficiency and user experience. The increasing preference for mechanized lawn care solutions is reducing manual labor requirements while improving productivity. These combined factors are contributing to steady market expansion across global regions.

The 50 to 60 inches segment accounted for USD 1.6 billion in 2025 and is expected to grow at a CAGR of 6.7% from 2026 to 2035. This segment is widely adopted due to its balanced cutting width, which makes it suitable for moderately large lawns, commercial landscapes, public green spaces, and institutional properties. It offers an effective combination of productivity and maneuverability, allowing operators to navigate complex landscapes while maintaining efficient mowing performance. Professional landscaping providers frequently prefer this category because it delivers faster cutting capability compared to smaller machines while still ensuring precision around obstacles and detailed landscape layouts. Growing adoption among property owners with larger outdoor spaces is also supporting demand as users transition toward more efficient mowing solutions that reduce operating time and improve overall lawn quality.

The indirect sales channel segment held a 68% share and is projected to grow at a CAGR of 6.1% from 2026 to 2035. This channel includes specialty retailers, large-format retail networks, and online distribution platforms that enable manufacturers to reach a broader customer base across both urban and rural regions. Indirect channels are particularly effective for high-value equipment as they provide customers with financing options, extensive product availability, and after-sales service support. Buyers often prefer authorized distributors due to the availability of product demonstrations, expert consultation, installation assistance, and maintenance services, all of which enhance purchasing confidence and long-term customer satisfaction.

United States Zero Turn Mower Market generated USD 900 million in 2025 and is anticipated to grow at a CAGR of 6.4% from 2026 to 2035. Market growth in the country is driven by a large base of residential users with expansive lawn areas, particularly in suburban locations, which supports consistent demand for high-performance mowing equipment. Increasing reliance on professional landscaping services, supported by rising income levels and growing emphasis on outdoor aesthetics, continues to boost product adoption. Expansion of public green infrastructure, including recreational parks, sports fields, and landscaped urban spaces, further strengthens demand. The country's well-established landscaping industry and preference for advanced, time-efficient equipment continue to reinforce market expansion.

Key companies operating in the Global Zero Turn Mower Market include Deere & Company (John Deere), The Toro Company, Husqvarna Group, Kubota Corporation, Textron Inc. (Bad Boy Mowers, E-Z-GO), Stanley Black & Decker (Cub Cadet), Briggs & Stratton LLC, Exmark Manufacturing, Scag Power Equipment, Hustler Turf Equipment, Wright Manufacturing, STIGA Group, AL-KO Gardentech, EGO Power+ (Chervon), Bad Boy Mowers, Spartan Mowers, Altoz, Mean Green Mowers, Raymo (robotic mowers), Country Clipper, and Greenworks Commercial. Companies operating in the zero turn mower market are focusing on product innovation, electrification, and smart technology integration to strengthen their competitive position. Manufacturers are investing in research and development to enhance cutting efficiency, fuel or battery performance, and overall durability of equipment. The adoption of GPS-enabled systems, telematics, and semi-autonomous capabilities is helping companies differentiate their offerings in a competitive landscape. Strategic partnerships with distributors and service providers are improving market penetration and customer support capabilities. Firms are also expanding their product portfolios to include electric and hybrid models in response to rising sustainability concerns. Strengthening after-sales services, improving financing options, and expanding digital sales channels are further helping companies enhance customer accessibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fuel type/power source

- 2.2.3 Cutting width

- 2.2.4 Yard space

- 2.2.5 End user

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for fast and efficient lawn maintenance equipment

- 3.2.1.2 Rising adoption of professional landscaping and grounds maintenance services

- 3.2.1.3 Growing development of golf courses, parks, sports fields, and public green spaces

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial purchase cost compared to traditional lawn mowers

- 3.2.2.2 Significant maintenance and repair expenses, especially for advanced models

- 3.2.3 Opportunities

- 3.2.3.1 Growing demand for electric and battery-powered zero-turn mowers driven by sustainability trends

- 3.2.3.2 Expansion of urban green infrastructure and smart city projects

- 3.2.3.3 Technological advancements such as AI-based navigation and IoT integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Trade data analysis (HS Code 8433.11)

- 3.7.1 Import/export volume & value trends

- 3.7.2 Key trade corridors & tariff impact

- 3.8 Pricing analysis

- 3.8.1 Historical price trend analysis (driven by primary research)

- 3.8.2 Pricing strategy by player type (premium / value / mass market)

- 3.8.3 Price positioning of technology vs traditional products

- 3.8.4 Regional price variations

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Fuel Type/Power Source, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Gasoline

- 5.3 Electric

- 5.4 Hybrid

- 5.5 Propane

Chapter 6 Market Estimates & Forecast, By Cutting Width, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Less than 50 inches

- 6.3 50 to 60 inches

- 6.4 More than 60 inches

Chapter 7 Market Estimates & Forecast, By Yard Space, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Small yard (less than 1 acre)

- 7.3 Medium yard (1 to 3 acres)

- 7.4 Large yard (More than 3 acres)

Chapter 8 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Golf course centers

- 8.3.2 Playgrounds

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Top Global Players

- 11.1.1 The Toro Company

- 11.1.2 Deere & Company (John Deere)

- 11.1.3 Husqvarna Group

- 11.1.4 Kubota Corporation

- 11.1.5 Textron Inc. (Bad Boy Mowers, E-Z-GO)

- 11.1.6 Briggs & Stratton LLC

- 11.1.7 The Stanley Black & Decker (Cub Cadet)

- 11.2 Regional Champions

- 11.2.1 Scag Power Equipment

- 11.2.2 Exmark Manufacturing

- 11.2.3 Hustler Turf Equipment

- 11.2.4 Wright Manufacturing

- 11.2.5 STIGA Group

- 11.2.6 AL-KO Gardentech

- 11.2.7 EGO Power+ (Chervon)

- 11.3 Emerging Players

- 11.3.1 Bad Boy Mowers

- 11.3.2 Spartan Mowers

- 11.3.3 Altoz

- 11.3.4 Mean Green Mowers

- 11.3.5 Raymo

- 11.3.6 Country Clipper

- 11.3.7 Greenworks Commercial