PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061390

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061390

Uninterruptible Power Supply (UPS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

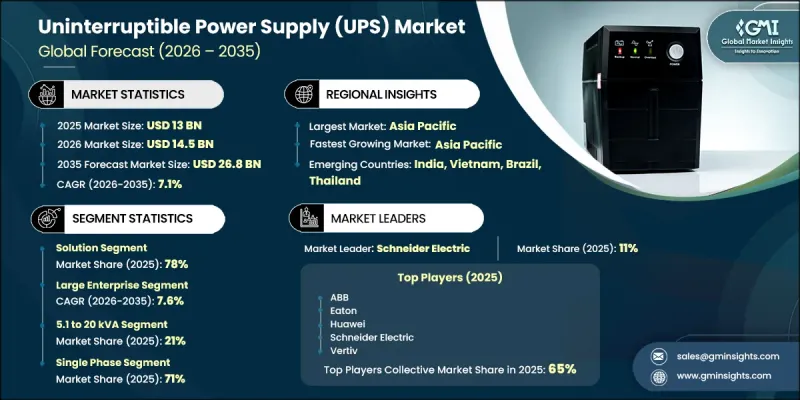

The Global Uninterruptible Power Supply (UPS) Market was valued at USD 13 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 26.8 billion by 2035.

The uninterruptible power supply industry is experiencing substantial growth due to rising dependence on digital infrastructure across industries such as healthcare, manufacturing, telecommunications, and data centers. Businesses are increasingly investing in advanced backup power solutions to maintain uninterrupted operations and safeguard sensitive equipment from power disruptions. Rapid expansion of hyperscale data centers is further accelerating demand for UPS systems, as continuous power protection is essential for servers, networking systems, and mission-critical infrastructure. In addition, increasing incidents of voltage fluctuations and power outages are encouraging wider deployment of UPS solutions across residential, commercial, and industrial sectors. Growing industrial automation and the adoption of connected manufacturing technologies are also strengthening the need for reliable power backup systems. Manufacturers are increasingly integrating lithium-ion batteries into UPS products because of their superior energy density, longer operational life, and extended runtime compared to conventional battery technologies. The adoption of modular UPS architecture is also gaining momentum, particularly in industrial facilities and data centers, due to its scalability, simplified maintenance, and ability to support expanding power requirements efficiently.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13 Billion |

| Forecast Value | $26.8 Billion |

| CAGR | 7.1% |

The large enterprise segment accounted for 68.3% share in 2025 and is anticipated to grow at a CAGR of 7.6% from 2026 to 2035. Large organizations are making significant investments in high-capacity UPS systems to ensure continuous operations across critical facilities. These systems are widely deployed to support advanced infrastructure and protect essential electronic equipment from unexpected power interruptions and voltage instability. Enterprises are increasingly upgrading their backup power infrastructure to minimize operational downtime, improve business continuity, and maintain uninterrupted workflow during electrical disturbances. Rising digital transformation initiatives and the growing importance of operational resilience are expected to continue supporting demand within this segment.

The single-phase segment held a 71% share in 2025. Demand for compact and lower-capacity backup power systems remains steady across residential properties, educational facilities, retail spaces, and small commercial establishments. Single-phase UPS systems are preferred for applications that require reliable and cost-effective power backup solutions without the need for high-capacity infrastructure. Their compact design, ease of installation, and suitability for smaller operations continue to drive widespread adoption across multiple end-use sectors.

U.S. Uninterruptible Power Supply (UPS) Market held an 85% share in 2025 and generated USD 3.7 billion. Market growth in the country is being driven by rising investments in hyperscale data centers, expanding healthcare infrastructure, and increasing deployment of industrial automation technologies. Growing reliance on cloud computing platforms, artificial intelligence workloads, and digital financial services is further contributing to the need for dependable power backup systems in critical environments. In addition, increasing concerns related to grid instability, severe weather conditions, and unexpected power failures are encouraging the adoption of UPS systems across residential, commercial, and industrial applications throughout the country.

Major companies operating in the Global Uninterruptible Power Supply (UPS) Market include Vertiv, Eaton, ABB, Schneider Electric, Huawei, Delta Electronics, Mitsubishi Electric, Legrand, Socomec, and CyberPower. Companies in the uninterruptible power supply market are implementing several strategic initiatives to strengthen their market presence and improve competitive positioning. Leading manufacturers are focusing on the development of energy-efficient and modular UPS systems that offer higher scalability and simplified maintenance for industrial and commercial applications. Businesses are also increasing investments in lithium-ion battery technology to deliver longer-lasting and more reliable backup power solutions. Strategic partnerships with data center operators, cloud service providers, and industrial automation companies are helping market participants expand their customer base and improve product integration capabilities. In addition, companies are prioritizing digital monitoring technologies, remote management solutions, and predictive maintenance capabilities to enhance operational efficiency and customer experience. Geographic expansion, continuous product innovation, and investments in smart power infrastructure remain key strategies supporting long-term growth in the Uninterruptible Power Supply (UPS) Market.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Organization Size

- 2.2.4 Capacity

- 2.2.5 Phase

- 2.2.6 Topology

- 2.2.7 Distribution Channel

- 2.2.8 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for data centers and cloud infrastructure

- 3.2.1.2 Increasing power outages and grid instability

- 3.2.1.3 Growth in industrial automation and smart manufacturing

- 3.2.1.4 Expansion of telecommunications and 5G infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High installation and maintenance costs

- 3.2.2.2 Limited battery lifespan and disposal concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of edge computing infrastructure

- 3.2.3.2 Adoption of lithium-ion battery technology

- 3.2.3.3 Integration with renewable energy systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 U.S. Department of Energy energy conservation standards for uninterruptible power supplies

- 3.6.1.2 UL 1778 safety and compliance requirements for uninterruptible power systems

- 3.6.1.3 National Electrical Code installation requirements for UPS systems

- 3.6.1.4 NFPA 110 and NFPA 111 requirements for emergency and standby power systems

- 3.6.1.5 Canadian Electrical Code and CSA C22.2 No. 107.3 requirements for UPS systems

- 3.6.2 Europe

- 3.6.2.1 Low Voltage Directive 2014 35 EU

- 3.6.2.2 Electromagnetic Compatibility Directive 2014 30 EU

- 3.6.2.3 Ecodesign requirements for standby and off mode power consumption

- 3.6.2.4 Restriction of Hazardous Substances Directive for electrical and electronic equipment

- 3.6.2.5 Waste Electrical and Electronic Equipment Directive and Batteries Regulation

- 3.6.3 Asia Pacific

- 3.6.3.1 China hazardous substance control requirements for electrical and electronic products

- 3.6.3.2 China regulations for recovery and disposal of waste electric and electronic products

- 3.6.3.3 India IS 16242 Part 1 general and safety requirements for UPS

- 3.6.3.4 Japan Electrical Appliances and Materials Safety Act and PSE marking requirements

- 3.6.3.5 Australia electrical goods safety and energy efficiency framework

- 3.6.4 Latin America

- 3.6.4.1 Brazil INMETRO conformity assessment and compulsory certification requirements

- 3.6.4.2 Brazil reverse logistics requirements for electronic waste and batteries

- 3.6.4.3 Mexico electrical installation requirements under NOM 001 SEDE 2012

- 3.6.4.4 Mexico UPS equipment standard based on UL 1778 and IEC 62040

- 3.6.4.5 Mercosur trade facilitation and technical harmonization frameworks

- 3.6.5 Middle East & Africa

- 3.6.5.1 UAE Certificates of Conformity for products subject to technical regulations

- 3.6.5.2 UAE telecommunications equipment approval and registration requirements

- 3.6.5.3 Saudi Arabia SASO conformity certificate and electrical equipment technical regulations

- 3.6.5.4 South Africa NRCS compulsory specifications for electrical products

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Trade Data Analysis (Driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Cost breakdown analysis

- 3.12 Impact of AI and Generative AI on the Market

- 3.12.1 AI Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.12.3 Risks Limitations and Regulatory Considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.15.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Standby (Offline)

- 5.2.2 Line-interactive

- 5.2.3 Online UPS

- 5.3 Service

- 5.3.1 Professional

- 5.3.2 Managed

Chapter 6 Market Estimates & Forecast, By Organization Size, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 SME

- 6.3 Large enterprise

Chapter 7 Market Estimates & Forecast, By Capacity, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Below 1 kVA

- 7.3 1.1 - 5 kVA

- 7.4 5.1 - 20 kVA

- 7.5 20.1 - 50 kVA

- 7.6 50.1 - 200 kVA

- 7.7 Above 200 kVA

Chapter 8 Market Estimates & Forecast, By Phase, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Single phase

- 8.3 Three phase

Chapter 9 Market Estimates & Forecast, By Deployment Architecture, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Centralized

- 9.3 Decentralized

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

- 10.3.1 Distributors

- 10.3.2 Value-Added Resellers (VARs)

- 10.3.3 E-commerce platforms

Chapter 11 Market Estimates & Forecast, By End Use, 2022 - 2035 (USD Mn, Units)

- 11.1 Key trends

- 11.2 BFSI

- 11.3 Data center

- 11.3.1 Hyperscale data centers

- 11.3.2 Colocation facilities

- 11.3.3 Enterprise data centers

- 11.3.4 Edge computing facilities

- 11.4 Healthcare

- 11.5 Telecommunications

- 11.6 Industrial applications

- 11.7 Government & defense

- 11.8 Others

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Norway

- 12.3.8 Netherlands

- 12.3.9 Sweden

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Singapore

- 12.4.7 Thailand

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

- 12.6.4 Turkey

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 ABB

- 13.1.2 CyberPower

- 13.1.3 Delta Electronics

- 13.1.4 Eaton

- 13.1.5 Huawei

- 13.1.6 Legrand

- 13.1.7 Mitsubishi Electric

- 13.1.8 Schneider Electric

- 13.1.9 Socomec

- 13.1.10 Vertiv

- 13.2 Regional Players

- 13.2.1 AEG Power Solutions

- 13.2.2 Borri

- 13.2.3 Fuji Electric

- 13.2.4 Kehua Tech

- 13.2.5 Piller Power Systems

- 13.2.6 Riello UPS

- 13.2.7 Toshiba International Corporation

- 13.3 Emerging Players / Disruptors

- 13.3.1 Active Power

- 13.3.2 Natron Energy

- 13.3.3 ZincFive