PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061412

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061412

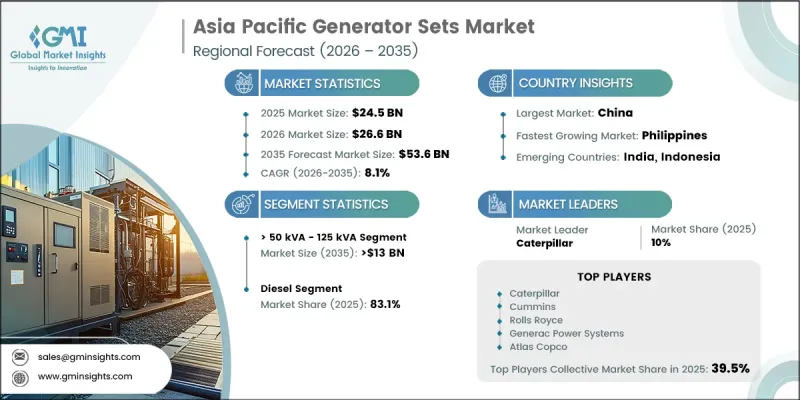

Asia Pacific Generator Sets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

Asia Pacific Generator Sets Market was valued at USD 24.5 billion in 2025 and is estimated to grow at a CAGR of 8.1% to reach USD 53.6 billion by 2035.

The market is experiencing strong growth as demand for uninterrupted and reliable power supply continues to increase across residential, commercial, and industrial sectors. Rising investments in transmission and distribution infrastructure are further strengthening genset adoption across the region. Supportive government initiatives focused on rural electrification, infrastructure development, and power reliability enhancement are also playing a major role in shaping market growth. In addition, increasing concerns regarding power outages and grid instability are driving end users toward backup and standby power solutions. Rapid industrialization, expansion of commercial facilities, and the growing importance of energy security are further accelerating demand for generator sets. The rise of data centers and digitization trends is also boosting reliance on backup power systems to avoid operational disruptions and data losses. Overall, the market is benefiting from strong infrastructure development, increasing electricity demand, and the need for continuous power availability across critical applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24.5 Billion |

| Forecast Value | $53.6 Billion |

| CAGR | 8.1% |

The diesel generator segment accounted for 83.1% share in 2025. Diesel-based gensets remain widely preferred due to their high reliability, operational flexibility, and ability to perform consistently under varied environmental conditions. These systems are extensively deployed across industrial facilities, commercial buildings, telecommunications infrastructure, and energy-intensive operations. Rising demand for dependable power solutions in both on-grid and off-grid regions is further reinforcing their adoption. Strong government focuses on improving electrification access and expanding high-capacity infrastructure, which continues to support segment growth across the region.

The >50 kVA-125 kVA segment is projected to reach USD 13 billion by 2035. This capacity range is widely used across residential complexes, telecom infrastructure, and small-scale commercial establishments due to its cost-effectiveness and reliable performance. Increasing frequency of extreme weather events and ongoing challenges in grid stability are contributing to higher demand for mid-range generator sets. These systems are increasingly preferred as an efficient backup power solution, ensuring uninterrupted electricity supply during outages and supporting essential operations across multiple end-use sectors.

China Generator Sets Market was valued at USD 10.3 billion in 2025. Market growth in the country is being driven by the rapid expansion of data centers, continuous upgrades in digital infrastructure, and rising dependence on uninterrupted power supply systems. Increasing digitization across industries and the growing frequency of power disruptions are further encouraging the adoption of backup power solutions. Demand is also rising across institutional sectors, where reliable electricity is essential for operational continuity in education, administration, and public services. Expanding industrial activity continues to reinforce the need for stable power infrastructure across the country.

Major companies operating in the Asia Pacific Generator Sets Market include Caterpillar, Cummins, Wartsila, Mitsubishi Heavy Industries, Atlas Copco, Generac Power Systems, FG Wilson, Rolls-Royce, Briggs & Stratton, Deere & Company, Yamaha Motor Co., Honda India Power Products, Kirloskar, MAHINDRA POWEROL, Ashok Leyland, Sudhir Power, HIMOINSA, Powerica, Sterling & Wilson, Supernova Genset, Rehlko, and Rapid Power Generation. Companies in the Asia Pacific generator sets market are focusing on strengthening their market presence through product innovation, strategic partnerships, and capacity expansion initiatives. Manufacturers are increasingly developing fuel-efficient and low-emission generator sets to comply with evolving environmental standards and reduce operational costs for end users. Investments in advanced control systems and digital monitoring technologies are enhancing equipment performance and enabling predictive maintenance capabilities. Companies are also expanding their distribution networks and service infrastructure to improve customer accessibility and after-sales support across emerging markets. Strategic collaborations with infrastructure developers and industrial clients are further helping firms secure long-term contracts.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Power rating trends

- 2.1.3 Fuel trends

- 2.1.4 End use trends

- 2.1.5 Application trends

- 2.1.6 Sales channel trends

- 2.1.7 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of generator sets

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.9.1 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

- 3.11 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.11.1 By power rating (Driven by Primary Research)

- 3.11.2 By fuel (Driven by Primary Research)

- 3.12 Trade data analysis (Driven by Primary Research)

- 3.12.1 Import/export value trends (Driven by Primary Research)

- 3.12.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Capacity by region & key producer (Driven by Primary Research)

- 3.13.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.14 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.14.1 AI-Driven production optimization (Driven by Primary Research)

- 3.14.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 China

- 4.2.2 Australia

- 4.2.3 India

- 4.2.4 Japan

- 4.2.5 South Korea

- 4.2.6 Indonesia

- 4.2.7 Malaysia

- 4.2.8 Thailand

- 4.2.9 Vietnam

- 4.2.10 Philippines

- 4.2.11 Myanmar

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 330 kVA

- 5.6 > 330 kVA - 750 kVA

- 5.7 > 750 kVA

Chapter 6 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Gas

- 6.4 Hybrid

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 Residential

- 7.2.1 Single family

- 7.2.2 Multi family

- 7.3 Commercial

- 7.3.1 Telecom

- 7.3.2 Healthcare

- 7.3.3 Data centers

- 7.3.4 Educational institutions

- 7.3.5 Government centers

- 7.3.6 Hospitality

- 7.3.7 Retail sales

- 7.3.8 Real estate

- 7.3.9 Commercial complex

- 7.3.10 Infrastructure

- 7.3.11 Others

- 7.4 Industrial

- 7.4.1 Oil & gas

- 7.4.2 Manufacturing

- 7.4.3 Construction

- 7.4.4 Electric utilities

- 7.4.5 Mining

- 7.4.6 Transportation & logistics

- 7.4.7 Others

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & ‘000 Units)

- 8.1 Key trends

- 8.2 Standby

- 8.3 Peak shaving

- 8.4 Prime/continuous

Chapter 9 Market Size and Forecast, By Sales Channel, 2022 - 2035 (USD Million & ‘000 Units)

- 9.1 Key trends

- 9.2 Online

- 9.3 Dealer

- 9.4 Retail

Chapter 10 Market Size and Forecast, By Country, 2022 - 2035 (USD Million & ‘000 Units)

- 10.1 Key trends

- 10.2 China

- 10.3 Australia

- 10.4 India

- 10.5 Japan

- 10.6 South Korea

- 10.7 Indonesia

- 10.8 Malaysia

- 10.9 Thailand

- 10.10 Vietnam

- 10.11 Philippines

- 10.12 Myanmar

Chapter 11 Company Profiles

- 11.1 Ashok Leyland

- 11.2 Atlas Copco

- 11.3 Briggs & Stratton

- 11.4 Caterpillar

- 11.5 Cummins

- 11.6 Deere & Company

- 11.7 FG Wilson

- 11.8 Generac Power Systems

- 11.9 HIMOINSA

- 11.10 Honda India Power Products

- 11.11 Kirloskar

- 11.12 MAHINDRA POWEROL

- 11.13 Mitsubishi Heavy Industries

- 11.14 Powerica

- 11.15 Rapid Power Generation

- 11.16 Rehlko

- 11.17 Rolls-Royce

- 11.18 Sterling & Wilson

- 11.19 Sudhir Power

- 11.20 Supernova Genset

- 11.21 Wartsila

- 11.22 Yamaha Motor Co.