PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061446

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061446

Railway Maintenance Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

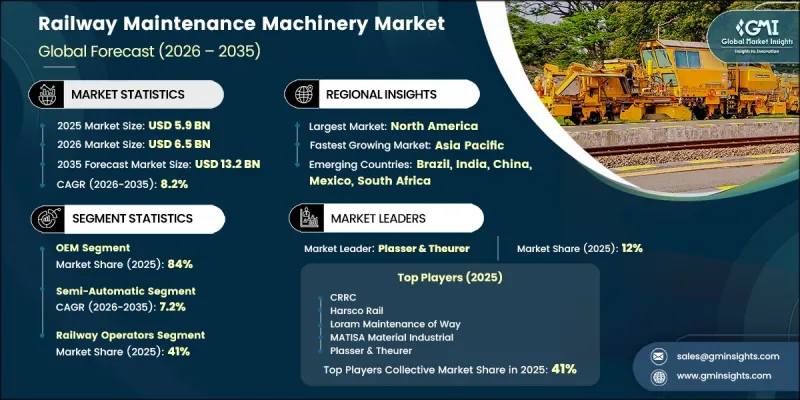

The Global Railway Maintenance Machinery Market was valued at USD 5.9 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 13.2 billion by 2035.

Growth across the railway maintenance machinery market is fueled by rising investments in rail infrastructure modernization, the expansion of passenger and freight rail networks, and the growing need to maintain aging railway assets efficiently. Railway maintenance equipment plays a critical role in ensuring network safety, operational performance, and long-term track reliability by supporting construction, inspection, repair, and maintenance activities. Demand for advanced machinery continues to increase as railway operators focus on improving track geometry, ballast stability, rail surface quality, and overall infrastructure performance. The industry is also benefiting from the growing adoption of technologically advanced maintenance solutions equipped with automation, digital monitoring capabilities, predictive maintenance software, GPS-enabled positioning systems, and energy-efficient powertrains. Manufacturers are developing highly accurate, durable, and cost-effective equipment to minimize downtime and improve maintenance productivity. The transition toward automated and semi-autonomous maintenance operations is enhancing safety standards while enabling faster and more efficient railway asset management, further strengthening market growth prospects over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.9 Billion |

| Forecast Value | $13.2 Billion |

| CAGR | 8.2% |

The railway maintenance machinery industry includes a broad portfolio of specialized equipment engineered to deliver precision, efficiency, and operational reliability. Modern maintenance systems increasingly incorporate intelligent monitoring technologies, automated diagnostics, predictive maintenance capabilities, and advanced positioning solutions to optimize maintenance activities. Equipment manufacturers are emphasizing automation, lightweight construction materials, and digital integration to improve performance while lowering operating and lifecycle costs. The shift away from conventional maintenance approaches toward technology-enabled systems continues to support higher levels of productivity, improved accuracy, and enhanced safety across railway operations worldwide.

The OEM segment accounted for 84% share in 2025 and is anticipated to grow at a CAGR of 7.8% between 2026 and 2035. This segment represents the sale of newly manufactured equipment supplied directly by manufacturers and authorized distribution networks, making it the primary revenue contributor within the industry. Railway operators and maintenance contractors continue to prioritize new equipment purchases due to the benefits of advanced technology integration, enhanced operational capabilities, and comprehensive warranty coverage. The strong preference for factory-new machinery reflects the industry's ongoing focus on reliability, efficiency, and long-term asset performance.

The semi-automatic segment captured 43.8% share in 2025 and is forecast to grow at a CAGR of 7.2% through 2035. Semi-automatic railway maintenance equipment combines automated work processes with operator supervision, making it one of the most widely adopted equipment categories across the industry. These systems automate key maintenance functions while allowing operators to maintain direct control over critical processes. Their widespread acceptance is supported by established operational practices, proven reliability, extensive workforce familiarity, and decades of deployment experience. As railway operators seek a balance between automation and operational flexibility, demand for semi-automatic machinery remains strong.

United States Railway Maintenance Machinery Market generated USD 1.8 billion in 2025 and is expected to grow at a CAGR of 7.2% from 2026 to 2035. Market expansion in the country is being supported by continued investments in railway infrastructure upgrades, modernization initiatives, and safety enhancement programs. Growing emphasis on improving rail network performance and maintaining infrastructure quality is driving increased deployment of advanced maintenance equipment. Railway operators are adopting sophisticated machinery to improve track conditions, strengthen operational reliability, and support long-term network sustainability. The country's extensive rail transportation network and ongoing infrastructure development efforts continue to create favorable opportunities for market growth.

Key companies operating in the Global Railway Maintenance Machinery Market include CRRC, Speno International, Plasser & Theurer, Harsco Rail, ROBEL Bahnbaumaschinen, Strukton Rail, MERMEC, MATISA Material Industrial, Loram Maintenance of Way, and Geatech. Companies operating in the railway maintenance machinery market are focusing on product innovation, automation, and digitalization to strengthen their market position and expand their customer base. Manufacturers are investing heavily in advanced maintenance technologies that improve operational efficiency, predictive maintenance capabilities, and equipment reliability. Strategic partnerships with railway operators, infrastructure developers, and maintenance contractors are helping companies secure long-term contracts and enhance service offerings. Businesses are also expanding their global footprint through acquisitions, regional expansion initiatives, and localized manufacturing capabilities. Integration of smart monitoring systems, data analytics, and remote diagnostics is becoming a key competitive strategy. In addition, companies are prioritizing sustainable and energy-efficient equipment development to align with evolving industry requirements while improving productivity, reducing maintenance costs, and enhancing overall customer value.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 Sales Channel

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aging railway infrastructure in developed economies

- 3.2.1.2 High-speed rail network expansion in emerging markets

- 3.2.1.3 Government investment in rail modernization programs

- 3.2.1.4 Shifts toward predictive & automated maintenance solutions

- 3.2.1.5 Growing freight rail traffic & infrastructure demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment requirements

- 3.2.2.2 Long equipment lifecycle & replacement intervals

- 3.2.2.3 Skilled operator shortage & training challenges

- 3.2.2.4 Regulatory compliance & safety certification complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Electrification of rail networks driving overhead line equipment demand

- 3.2.3.2 Integration of IoT & digital twins for predictive maintenance

- 3.2.3.3 Public-private partnerships in railway infrastructure development

- 3.2.3.4 Refurbishment & aftermarket services growth

- 3.2.3.5 Autonomous & remote-controlled maintenance equipment

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technological trends

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US- Federal Railroad Administration (FRA) Track Safety Standards

- 3.6.1.2 Canada - Transport Canada Railway Safety Act & Regulations

- 3.6.2 Europe

- 3.6.2.1 Germany- Eisenbahn-Bau- und Betriebsordnung (EBO) & EU Rail Directives

- 3.6.2.2 UK- Railways and Other Guided Transport Systems (Safety) Regulations & National Standards

- 3.6.2.3 France- Code des Transports & Decarbonization Rail Strategy

- 3.6.2.4 Italy- Rete Ferroviaria Italiana (RFI) Maintenance Standards

- 3.6.3 Asia Pacific

- 3.6.3.1 China- National Railway Administration Track Maintenance Standards

- 3.6.3.2 India- Indian Railways Track Maintenance Regulations & Electrification Standards

- 3.6.3.3 Japan- Ministry of Land, Infrastructure, Transport & Tourism (MLIT) Rail Safety Standards

- 3.6.3.4 Australia- National Rail Safety Law & Environmental Regulations

- 3.6.4 LATAM

- 3.6.4.1 Mexico- SCT Rail Safety & NOM-121-SCT Regulations

- 3.6.4.2 Argentina- National Rail Safety Law & Environmental Regulations

- 3.6.5 MEA

- 3.6.5.1 South Africa- Railway Safety Regulator Act & Track Safety Standards

- 3.6.5.2 Saudi Arabia- Railway Law & Vision 2030 Transport Modernization Initiatives

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Trade Data Analysis (Driven by Paid Database)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

- 3.11 Cost breakdown analysis

- 3.12 Patent analysis (Driven by Primary Research)

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable Practices

- 3.13.2 Waste Reduction Strategies

- 3.13.3 Energy Efficiency in Production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon Footprint Considerations

- 3.14 Impact of AI & generative AI on the market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.2 GenAI use cases & adoption roadmap by segment

- 3.14.3 Risks, limitations & regulatory considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.15.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

- 3.16 Maintenance contracting & outsourcing trends

- 3.16.1 In-house vs. outsourced maintenance models

- 3.16.2 Equipment leasing & performance-based contracting

- 3.16.3 Public-private partnership (PPP) structures in railway maintenance

- 3.16.4 Regional variations in outsourcing penetration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Track laying & renewal machines

- 5.3 Tamping machine

- 5.4 Stabilizing machinery

- 5.5 Ballast cleaning machinery

- 5.6 Rail grinding & milling machinery

- 5.7 Surfacing machinery

- 5.8 Overhead Line Maintenance Equipment

- 5.9 Others

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 New construction

- 6.3 Preventive maintenance

- 6.4 Corrective maintenance

- 6.5 Track renewal/rehabilitation

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Semi-automatic

- 7.4 Fully automatic

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Railway infrastructure companies

- 9.3 Contractors

- 9.4 Railway operators

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 CRCC

- 11.1.2 Harsco Rail

- 11.1.3 Loram Maintenance of Way

- 11.1.4 MATISA Material Industrial

- 11.1.5 Plasser and Theurer

- 11.1.6 Progress Rail

- 11.1.7 ROBEL Bahnbaumaschinen

- 11.1.8 Wabtec

- 11.2 Regional Players

- 11.2.1 Geatech

- 11.2.2 Holland

- 11.2.3 Knox Kershaw

- 11.2.4 MER MEC

- 11.2.5 Sinara Transport Machines

- 11.2.6 Speno International

- 11.2.7 Strukton

- 11.3 Emerging Players

- 11.3.1 American Equipment

- 11.3.2 Beijing Yan Hong Da Railway Equipment

- 11.3.3 Coril Holdings

- 11.3.4 Gemac Engineering Machinery

- 11.3.5 Knox Kershaw