PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061459

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061459

Smart Home Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

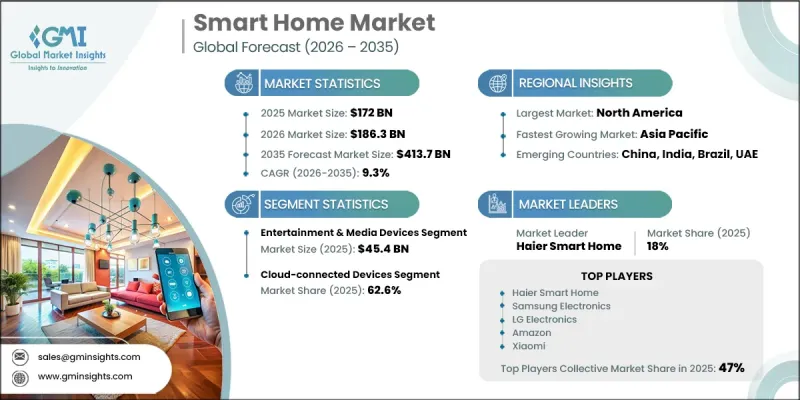

The Global Smart Home Market was valued at USD 172 billion in 2025 and is estimated to grow at a CAGR of 9.3% to reach USD 413.7 billion by 2035.

The smart home industry is rapidly transforming as consumers increasingly seek greater convenience, security, automation, and control across residential environments. Modern households are steadily shifting toward connected ecosystems where appliances, lighting systems, climate control, security solutions, and entertainment platforms operate together to simplify everyday living. Growing familiarity with smartphones, digital assistants, and connected technologies has significantly improved consumer confidence in adopting smart home products. What was once viewed as a luxury is now considered a practical investment for improving energy efficiency, strengthening home safety, and streamlining household management. The market is also evolving through continuous advancements in artificial intelligence, automation, and cloud computing technologies. Rising interoperability among devices from different manufacturers is encouraging the development of open ecosystems and standardized communication protocols, helping reduce compatibility concerns for users. As a result, technology providers, consumer electronics brands, and home automation companies are continuously expanding product portfolios to meet changing customer expectations and support broader adoption of connected living solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $172 Billion |

| Forecast Value | $413.7 Billion |

| CAGR | 9.3% |

In 2025, the entertainment and media devices segment generated USD 45.4 billion, making it the leading category within the smart home market. This segment continues to dominate due to its high consumer adoption, ease of installation, and immediate usability benefits. Connected entertainment products often serve as the first point of entry for consumers transitioning toward smart living environments. Their accessibility, convenience, and familiarity have helped establish them as one of the most widely adopted components of the broader smart home ecosystem.

The cloud-connected devices segment accounted for 62.6% share in 2025. Cloud-enabled infrastructure has become the foundation of modern smart home systems by allowing devices to communicate, synchronize, and operate as part of a unified ecosystem. These systems support real-time updates, centralized automation, remote monitoring, and seamless interoperability between multiple connected products. The increasing number of smart devices within households continues to accelerate reliance on cloud platforms for data processing, communication management, and automated functionality. This transition has transformed smart homes from collections of independent devices into integrated digital environments capable of delivering synchronized user experiences.

U.S. Smart Home Market held an 89% share and generated USD 50 billion in 2025. The region represents a highly developed and innovation-focused environment where connected technologies are already deeply integrated into daily routines. Consumers across North America increasingly view smart home products as practical tools that enhance convenience, improve home security, and support modern lifestyles. Strong smartphone penetration, widespread internet connectivity, and growing familiarity with voice-controlled assistants continue to encourage household adoption of connected technologies throughout the region.

Major companies operating in the Smart Home Market include Amazon, Apple, Google, Samsung, LG Electronics, Haier Smart Home, Panasonic, Xiaomi, Alibaba (Tmall Genie), Legrand, Schneider Electric, Robert Bosch, Crestron Electronics, Somfy, Signify (Philips Hue), Assa Abloy (Yale/August), Honeywell International, Lutron Electronics, TP-Link (Kasa Smart), and Aqara (Lumi United). Companies operating in the smart home market are focusing on multiple growth strategies to strengthen their market position and expand consumer reach. Leading players are investing heavily in artificial intelligence, cloud computing, and IoT integration to improve device interoperability and deliver seamless user experiences across connected ecosystems. Many manufacturers are introducing products compatible with open communication standards to reduce compatibility challenges and encourage wider adoption. Strategic collaborations with technology providers, telecom companies, and homebuilders are also helping brands increase product visibility and distribution channels. In addition, companies are prioritizing energy-efficient solutions, voice-enabled controls, and enhanced cybersecurity features to meet evolving consumer expectations.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360°synopsis

- 2.2 Key trends

- 2.3 Type

- 2.4 Connectivity

- 2.5 Price Range

- 2.6 End Use

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Value chain structure

- 3.1.2 Component manufacturers & suppliers

- 3.1.3 Device manufacturers/OEMs

- 3.1.4 Platform & software providers

- 3.1.5 Distribution & retail layer

- 3.1.6 Installation & integration services

- 3.1.7 End-user/consumer layer

- 3.1.8 Profit margin analysis by value chain stage

- 3.1.9 Value chain disruptions & disintermediation trends

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Supply chain analysis

- 3.4.1 Component supply chain structure

- 3.4.2 Semiconductor dependency & chip shortage impact

- 3.4.3 Manufacturing footprint

- 3.4.4 Logistics & distribution networks

- 3.4.5 Supply chain risks & mitigation strategies

- 3.4.6 Reshoring & nearshoring trends

- 3.5 Regulation Coverage

- 3.5.1 U.S. regulatory environment

- 3.5.1.1 FCC wireless device regulations

- 3.5.1.2 State-level privacy laws (CCPA, etc.)

- 3.5.1.3 Energy efficiency standards (Energy Star)

- 3.5.2 European regulatory environment

- 3.5.2.1 GDPR data protection requirements

- 3.5.2.2 CE marking & product safety directives

- 3.5.2.3 Energy efficiency regulations (EU Ecodesign)

- 3.5.2.4 Radio Equipment Directive (RED)

- 3.5.3 Cybersecurity regulations

- 3.5.3.1 U.S. IoT cybersecurity improvement act

- 3.5.3.2 EU cybersecurity act & ETSI standards

- 3.5.4 Asia Pacific regulatory environment

- 3.5.4.1 China regulatory framework

- 3.5.4.2 Japan regulatory framework

- 3.5.4.3 India regulatory framework

- 3.5.4.4 South Korea & Australia compliance requirements

- 3.5.5 Latin America regulatory environment

- 3.5.5.1 Brazil regulatory framework

- 3.5.5.2 Mexico regulatory framework

- 3.5.6 Middle East & Africa regulatory environment

- 3.5.6.1 GCC countries regulatory framework

- 3.5.6.2 South Africa & Israel compliance requirements

- 3.5.6.3 Data sovereignty & cross-border data transfer regulations

- 3.5.1 U.S. regulatory environment

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (2022-2024)

- 3.6.2 Pricing strategy by player type

- 3.6.3 Regional price variation

- 3.6.4 Channel-specific pricing dynamics

- 3.6.5 Bundle pricing vs a la carte models

- 3.6.6 Subscription service pricing trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Impact of AI and generative AI on the European doors market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.1.1 Voice assistants’ evolution (GPT integration)

- 3.9.1.2 Predictive automation & learning systems

- 3.9.1.3 Computer vision applications (security, monitoring)

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.2.1 Personalized home automation routines

- 3.9.2.2 Natural language control interfaces

- 3.9.2.3 Predictive maintenance & energy optimization

- 3.9.2.4 Content generation for smart displays

- 3.9.3 Risks, limitations & regulatory considerations

- 3.9.3.1 Data privacy & AI model training concerns

- 3.9.3.2 Algorithmic bias & fairness issues

- 3.9.3.3 EU AI Act compliance requirements

- 3.9.1 AI-driven disruption of existing business models

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plan

Chapter 5 Smart Home Market Estimates & Forecast, By Type (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Security & access control systems

- 5.2.1 Security cameras

- 5.2.1.1 Indoor cameras

- 5.2.1.2 Outdoor cameras

- 5.2.1.3 Doorbell cameras

- 5.2.2 Smart locks

- 5.2.2.1 Keypad locks

- 5.2.2.2 Biometric locks

- 5.2.2.3 Retrofit smart lock kits

- 5.2.3 Video door phones/intercoms

- 5.2.4 Remote monitoring software & services

- 5.2.5 Alarm systems & sensors

- 5.2.6 Other security devices

- 5.2.1 Security cameras

- 5.3 Lighting control systems

- 5.3.1 Smart lights/bulbs

- 5.3.1.1 LED smart bulbs

- 5.3.1.2 Smart light strips

- 5.3.2 Relays & switches

- 5.3.2.1 In-wall smart switches

- 5.3.2.2 Plug-in smart outlets

- 5.3.3 Occupancy sensors & motion detectors

- 5.3.4 Dimmers & controllers

- 5.3.5 Other lighting control products

- 5.3.1 Smart lights/bulbs

- 5.4 HVAC & energy management systems

- 5.4.1 Smart thermostats

- 5.4.2 Learning thermostats

- 5.4.2.1 Programmable thermostats

- 5.4.2.2 HVAC sensors (temperature, humidity, air quality)

- 5.4.3 Smart vents & dampers

- 5.4.4 Energy monitoring systems

- 5.4.5 Smart meters

- 5.4.6 Solar panel controllers & inverters

- 5.4.7 Battery storage systems

- 5.4.8 Other HVAC & energy products

- 5.5 Entertainment & media devices

- 5.5.1 Smart displays/TVs

- 5.5.2 Streaming devices (Roku, Fire TV, Apple TV)

- 5.5.3 Sound bars & speakers

- 5.5.4 Smart speakers (Alexa, Google Home, HomePod)

- 5.5.5 Multi-room audio systems

- 5.5.6 Other entertainment devices

- 5.6 Smart kitchen appliances

- 5.6.1 Smart refrigerators

- 5.6.2 Smart dishwashers

- 5.6.3 Smart cooktops & ranges

- 5.6.4 Smart microwaves & ovens

- 5.6.5 Smart coffee makers

- 5.6.6 Other kitchen appliances

- 5.7 Smart home appliances

- 5.7.1 Smart washing machines & dryers

- 5.7.2 Smart water heaters

- 5.7.3 Smart vacuum cleaners

- 5.7.4 Smart air purifiers & fans

- 5.7.5 Other home appliances

- 5.8 Home healthcare devices

- 5.8.1 Remote patient monitoring systems

- 5.8.2 Fall detection & alert systems

- 5.8.3 Ambient assisted living solutions

- 5.8.4 Smart beds with health sensors

- 5.8.5 Sleep monitoring systems

- 5.8.6 Medication management devices

- 5.8.7 Other healthcare devices

- 5.9 Other smart home devices

- 5.9.1 Smart furniture (non-health)

- 5.9.2 Smart mirrors

- 5.9.3 Smart pet care devices

- 5.9.4 Smart lawn & garden equipment

- 5.9.5 Other connected products

Chapter 6 Smart Home Market Estimates & Forecast, By Connectivity (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Cloud-connected devices

- 6.2.1 Wi-Fi-based devices

- 6.2.2 Cellular/LTE-based devices

- 6.2.3 Cloud platform dependencies & risks

- 6.3 Local mesh network devices

- 6.3.1 Zigbee protocol devices

- 6.3.2 Z-Wave protocol devices

- 6.3.3 Thread protocol devices

- 6.3.4 Hub requirements & architecture

- 6.4 Proximity-based devices

- 6.4.1 Bluetooth devices

- 6.4.2 Bluetooth Low Energy (BLE) devices

- 6.4.3 NFC-enabled devices

- 6.5 Wired protocol devices

- 6.5.1 Ethernet-connected devices

- 6.5.2 KNX systems

- 6.5.3 Power line communication (PLC)

- 6.6 Matter unified standard devices

Chapter 7 Smart Home Market Estimates & Forecast, By Price Range (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low (<$100 per device)

- 7.3 Medium (0-0 per device)

- 7.4 High (>$500 per device)

Chapter 8 Smart Home Market Estimates & Forecast, By End Use (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 New construction

- 8.3 Retrofit

Chapter 9 Smart Home Market Estimates & Forecast, By Region (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 U.K.

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Amazon

- 10.1.2 Apple

- 10.1.3 Google

- 10.1.4 Samsung

- 10.1.5 LG Electronics

- 10.1.6 Haier Smart Home

- 10.1.7 Panasonic

- 10.2 Regional Players

- 10.2.1 Xiaomi

- 10.2.2 Alibaba (Tmall Genie)

- 10.2.3 Legrand

- 10.2.4 Schneider Electric

- 10.2.5 Robert Bosch

- 10.2.6 Crestron Electronics

- 10.2.7 Somfy

- 10.3 Niche/Specialist Players

- 10.3.1 Signify (Philips Hue)

- 10.3.2 Assa Abloy (Yale/August)

- 10.3.3 Honeywell International

- 10.3.4 Lutron Electronics

- 10.3.5 TP-Link (Kasa Smart)

- 10.3.6 Aqara (Lumi United)