PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071245

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071245

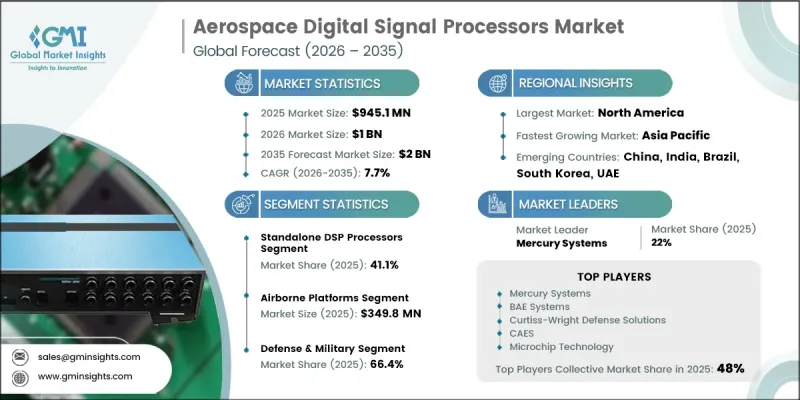

Aerospace Digital Signal Processors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Aerospace Digital Signal Processors Market was valued at USD 945.1 million in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 2 billion by 2035.

Growth across the aerospace digital signal processors market is fueled by the increasing deployment of sophisticated avionics technologies and the growing requirement for high-speed data processing within modern aerospace systems. As aerospace platforms become more advanced, demand continues to rise for processors capable of managing complex computing workloads with exceptional speed, accuracy, and reliability. The market is also benefiting from the expanding integration of advanced sensing technologies, mission-critical processing capabilities, and enhanced communication systems throughout aerospace and defense operations. Continuous investments in aerospace connectivity infrastructure are creating additional opportunities for digital signal processing solutions that support secure and efficient data transmission. Technological progress in miniaturized electronics and highly durable semiconductor components is further contributing to market expansion. In addition, the growing implementation of autonomous capabilities and artificial intelligence across aerospace applications is increasing the need for advanced processing architectures that can deliver real-time computational performance while maintaining operational reliability in demanding environments. These factors collectively continue to strengthen the long-term outlook for the global aerospace digital signal processors market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $945.1 Million |

| Forecast Value | $2 Billion |

| CAGR | 7.7% |

The aerospace digital signal processors market is experiencing substantial momentum due to the increasing adoption of advanced avionics platforms and high-performance data processing technologies. Modern aerospace systems require processors capable of handling significant volumes of information with minimal delay, supporting efficient operation across increasingly sophisticated environments. The expansion of aerospace communication networks and satellite-based connectivity systems is further accelerating demand for advanced digital signal processing technologies. Growing emphasis on secure data transmission and protection within mission-critical aerospace environments is encouraging the adoption of enhanced processing solutions that support robust encryption capabilities and secure communication frameworks. These developments are helping improve system reliability, operational continuity, and overall performance across aerospace and defense applications.

The standalone DSP processors segment accounted for 41.1% share in 2025, making it the largest segment within the industry. Its leadership position is attributed to widespread adoption across numerous aerospace processing applications where design flexibility, system compatibility, and supplier diversification remain important considerations. Strong compatibility with established aerospace architectures and existing avionics ecosystems continues to support demand for standalone DSP solutions. Market growth is further reinforced by ongoing modernization programs and continued investment in advanced aerospace platform development, which require dependable and adaptable signal processing technologies.

The airborne platforms segment generated USD 349.8 million in 2025. Segment growth is supported by the extensive global fleet of aerospace platforms that require continuous technology upgrades and system enhancements throughout their operational lifecycles. Digital signal processors integrated within airborne systems support a broad range of mission-critical processing requirements and play an essential role in maintaining operational effectiveness. Demand remains consistent due to ongoing equipment upgrades, modernization initiatives, and long-term maintenance activities across both original equipment manufacturing and aftermarket service channels.

North America Aerospace Digital Signal Processors Market accounted for 40.6% share in 2025. The region benefits from a highly developed aerospace and defense ecosystem supported by extensive manufacturing capabilities, advanced technology development, research institutions, and specialized component suppliers. Sustained investments in aerospace modernization initiatives and long-term procurement programs continue to generate strong demand for high-performance digital signal processing technologies. The presence of a mature aerospace infrastructure and ongoing development of advanced aerospace systems further strengthens the region's position within the global market. Continuous focus on innovation, security, and next-generation aerospace technologies is expected to support steady demand for aerospace digital signal processors across North America.

Key companies operating in the Global Aerospace Digital Signal Processors Market include AMD, Microchip Technology, BAE Systems, Intel, Texas Instruments, Analog Devices, VORAGO Technologies, NanoXplore, Teledyne e2v, CAES, NXP Semiconductors, onsemi, Renesas Electronics, STMicroelectronics, Infineon Technologies, Cobham Gaisler, Mercury Systems, and Curtiss-Wright Defense Solutions. Companies participating in the aerospace digital signal processors market are implementing a variety of strategic initiatives to strengthen their market presence and enhance competitive positioning. Product innovation remains a primary focus, with manufacturers investing heavily in the development of high-performance, radiation-tolerant, and power-efficient processing solutions designed for demanding aerospace environments. Strategic collaborations with aerospace manufacturers, defense contractors, and government organizations are helping companies secure long-term supply agreements and expand market opportunities. Businesses are also increasing investments in research and development to accelerate technological advancements in artificial intelligence, autonomous systems, and real-time signal processing capabilities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Environmental grade trends

- 2.2.3 Platform trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of advanced avionics and real-time data processing systems

- 3.2.1.2 Increasing integration of radar, electronic warfare, and ISR systems in defense aircraft

- 3.2.1.3 Expansion of satellite communication and aerospace connectivity infrastructure

- 3.2.1.4 Technological advancements in miniaturized and radiation hardened electronics

- 3.2.1.5 Growing demand for autonomous and AI enabled aerospace systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development complexity and cost of aerospace-grade DSPs

- 3.2.2.2 Stringent certification and long qualification cycles

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption of edge computing in aerospace systems

- 3.2.3.2 Increasing demand for space exploration and satellite constellations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Standalone DSP processors

- 5.2.1 Single-core DSP processors

- 5.2.2 Multi-core DSP processors

- 5.3 Integrated DSP systems

Chapter 6 Market Estimates and Forecast, By Environmental Grade, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Silicon (Si)

- 6.3 Silicon carbide (SiC)

- 6.4 Gallium nitride (GaN)

- 6.5 Commercial aerospace grade

- 6.6 Ruggedized grade

- 6.7 Radiation-tolerant grade

- 6.8 Radiation-hardened grade

Chapter 7 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Airborne platforms

- 7.3 Space platforms

- 7.4 Defense systems

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Defense & military

- 8.3 Commercial & civil aerospace

- 8.4 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Mercury Systems

- 10.1.2 BAE Systems

- 10.1.3 Curtiss-Wright Defense Solutions

- 10.1.4 CAES

- 10.1.5 Microchip Technology

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 AMD

- 10.2.1.2 Intel

- 10.2.1.3 Texas Instruments

- 10.2.1.4 Analog Devices

- 10.2.1.5 onsemi

- 10.2.2 Asia Pacific

- 10.2.2.1 Renesas Electronics

- 10.2.3 Europe

- 10.2.3.1 STMicroelectronics

- 10.2.3.2 Infineon Technologies

- 10.2.3.3 NXP Semiconductors

- 10.2.3.4 Cobham Gaisler

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 VORAGO Technologies

- 10.3.2 NanoXplore

- 10.3.3 Teledyne e2v