PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071251

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071251

Europe Cutting Tool Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

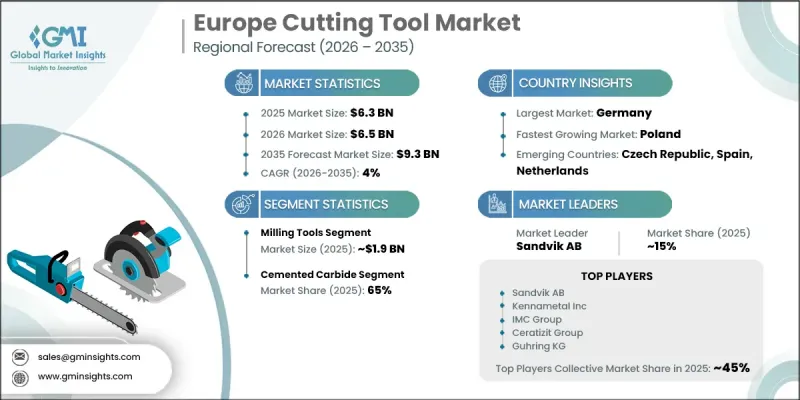

Europe Cutting Tool Market was estimated at USD 6.3 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 9.3 billion by 2035.

Growth across the Europe cutting tool industry is driven by evolving manufacturing requirements, advancements in industrial production technologies, and increasing demand for precision machining solutions. The market continues to benefit from the transition toward next-generation transportation technologies, expanding aerospace and defense manufacturing activities, and the modernization of production facilities across the region. Despite periods of softness in broader machine tool consumption, cutting tools have demonstrated strong resilience due to their essential role in ongoing manufacturing operations and recurring replacement cycles. Demand for high-performance tooling solutions is increasing as manufacturers seek greater productivity, tighter tolerances, and improved operational efficiency. In addition, industrial development across emerging manufacturing centers within Europe is accelerating the adoption of advanced cutting materials and premium tooling technologies. The growing emphasis on precision engineering, production efficiency, and high-quality component manufacturing is expected to support long-term market expansion. As industrial sectors continue to invest in modernization and advanced machining capabilities, demand for cutting tools is anticipated to remain strong throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.3 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 4% |

The milling tools segment generated USD 1.9 billion in 2025 and is projected to grow at a CAGR of 4.5% from 2026 to 2035. Milling tools represent the largest revenue-generating product category within the Europe cutting tool market due to their widespread use in precision machining applications across multiple industries. Demand is being supported by increasing requirements for complex component manufacturing, high-accuracy machining processes, and advanced material processing. The growing adoption of sophisticated machining technologies is further expanding the application scope of milling tools, particularly for operations requiring superior surface quality, dimensional accuracy, and production efficiency. Continued investments in advanced manufacturing capabilities are expected to reinforce the segment's leadership position over the coming years.

The cemented carbide segment accounted for 65% share in 2025 and is anticipated to grow at a CAGR of 4.5% through 2035. Cemented carbide remains the dominant material category due to its exceptional combination of durability, wear resistance, machining efficiency, and versatility across a broad range of cutting operations. The material is widely utilized in turning, drilling, milling, and other high-performance machining applications where productivity and tool life are critical considerations. Ongoing industrial expansion and increasing demand for advanced manufacturing processes continue to strengthen the position of cemented carbide as the preferred material choice across the European cutting tool industry.

Germany Cutting Tool Market generated USD 1.7 billion in 2025 and is forecast to grow at a CAGR of 2.9% from 2026 to 2035. The country's leading position is supported by its strong industrial foundation, advanced manufacturing capabilities, and continued investment in high-precision engineering sectors. Structural shifts across key manufacturing industries are creating new opportunities for cutting tool suppliers as production facilities increasingly adopt advanced machining technologies and automation solutions. Although certain industrial sectors previously faced operational challenges, growing investments in modern production systems and precision manufacturing are supporting market recovery and long-term growth. The increasing need for high-performance cutting solutions across technologically advanced industries is expected to sustain Germany's leadership within the regional market.

Major companies operating in the Europe cutting tool market include Sandvik AB, Kennametal Inc., Ceratizit Group, ISCAR Ltd., OSG Corporation, Mitsubishi Materials Tools Europe GmbH, Guhring KG, Mapal Dr. Kress KG, Paul Horn GmbH, LMT Tools, EMUGE-FRANKEN, Sumitomo Electric Hardmetal Corp., Nachi-Fujikoshi Corp., Kyocera Precision Tools, Vargus Ltd., YG-1 Co., Ltd., Fraisa SA, Mikron Tool SA, Carmex Precision Tools Ltd., Cerin S.p.A., and ARNO Werkzeuge. Companies operating in the Europe cutting tool industry are implementing a variety of strategic initiatives to strengthen their market position and enhance competitive advantage. Product innovation remains a central focus, with manufacturers investing in advanced tool geometries, premium coatings, high-performance materials, and extended tool-life technologies. Businesses are also increasing investments in research and development to improve machining efficiency, productivity, and precision across diverse industrial applications. Strategic collaborations with manufacturing companies, industrial distributors, and technology providers are helping expand market reach and strengthen customer relationships.

Table of Contents

Chapter 1 Research methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Business trends

- 2.3 Country

- 2.4 Product type

- 2.5 Material

- 2.6 End-use industry

- 2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Manufacturers

- 3.1.3 Distributors

- 3.1.4 Retailers

- 3.1.5 Profit margin analysis

- 3.1.6 Value addition at each stage

- 3.1.7 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand from EV transition

- 3.2.1.2 Aerospace production ramp-up driving precision tooling demand

- 3.2.1.3 CNC automation and lights-out manufacturing increasing tool cycle frequency

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Skilled machinist shortage across region

- 3.2.2.2 Volatility in tungsten and cobalt prices impacting carbide tool costs

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis (driven by primary research)

- 3.5.1 Historical price trend analysis by product category

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6 Trade data analysis (based on paid database)

- 3.6.1 Import/export volume & value trends

- 3.6.2 Key trade corridors & tariff impact

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Turning Tools

- 5.3 Milling Tools

- 5.4 Drilling Tools

- 5.5 Tapping & Threading Tools

- 5.6 Reaming & Broaching Tools

- 5.7 Grinding & Abrasive Tools

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Units)

- 6.1 Key trends

- 6.2 High-Speed Steel

- 6.3 Cemented Carbide

- 6.4 Cermet

- 6.5 Ceramics

- 6.6 Polycrystalline Diamond

- 6.7 Cubic Boron Nitride

Chapter 7 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Automotive

- 7.2.1 ICE Powertrain & Engine Components

- 7.2.2 Electric Vehicle (EV) & Hybrid Components

- 7.2.3 Transmission & Driveline Components

- 7.2.4 Body, Chassis & Structural Parts

- 7.2.5 Automotive Aftermarket & Component MRO

- 7.3 Aerospace & Defense

- 7.3.1 Commercial Aviation

- 7.3.2 Military Aviation & Defence Equipment

- 7.3.3 Space & New Space Components

- 7.3.4 Maintenance, Repair & Overhaul

- 7.4 Industrial Machinery & Equipment

- 7.5 Metal Products & General Metalworking

- 7.6 Medical Devices

- 7.7 Electronics & Semiconductors

- 7.8 Energy

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Units)

- 9.1 Key trends

- 9.2 Europe

- 9.2.1 Germany

- 9.2.2 UK

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Sweden

- 9.2.7 Netherlands

- 9.2.8 Poland

- 9.2.9 Czech Republic

- 9.2.10 Austria

- 9.2.11 Belgium

- 9.2.12 Switzerland

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Sandvik AB

- 10.1.2 Kennametal Inc.

- 10.1.3 ISCAR Ltd.

- 10.1.4 Ceratizit Group

- 10.1.5 Mitsubishi Materials Tools Europe GmbH

- 10.1.6 OSG Corporation

- 10.2 Regional Players

- 10.2.1 Mapal Dr. Kress KG

- 10.2.2 Guhring KG

- 10.2.3 LMT Tools

- 10.2.4 Paul Horn GmbH

- 10.2.5 EMUGE-FRANKEN

- 10.2.6 Sumitomo Electric Hardmetal Corp.

- 10.2.7 Nachi-Fujikoshi Corp.

- 10.2.8 Vargus Ltd.

- 10.2.9 Kyocera Precision Tools

- 10.2.10 YG-1 Co Ltd.

- 10.3 Emerging Players

- 10.3.1 Fraisa SA

- 10.3.2 Mikron Tool SA

- 10.3.3 Cerin S.p.A.

- 10.3.4 ARNO Werkzeuge

- 10.3.5 Carmex Precision Tools Ltd.