PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071264

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071264

Electric Vehicle Fleet Maintenance Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

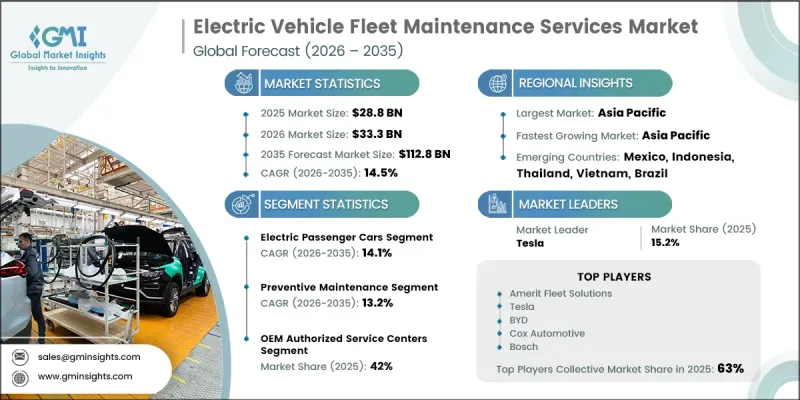

The Global Electric Vehicle Fleet Maintenance Services Market was valued at USD 28.8 billion in 2025 and is estimated to grow at a CAGR of 14.5% to reach USD 112.8 billion by 2035.

The rapid adoption of electric vehicle fleets across commercial transportation sectors is creating strong demand for specialized maintenance and servicing solutions. As organizations continue transitioning toward electrified transportation to improve operational efficiency and meet sustainability objectives, maintenance requirements for electric fleets are becoming increasingly sophisticated. Rising demand for battery health management, charging infrastructure servicing, software diagnostics, and advanced vehicle monitoring solutions is supporting market expansion worldwide. Favorable government policies promoting vehicle electrification and zero-emission transportation are further strengthening industry growth. At the same time, technological advancements in telematics, artificial intelligence (AI), the Internet of Things (IoT), and over-the-air (OTA) diagnostic capabilities are reshaping maintenance operations. Fleet operators are leveraging predictive maintenance platforms to maximize vehicle availability, streamline service schedules, and reduce maintenance costs. The growing integration of connected fleet technologies, remote monitoring platforms, and data-driven maintenance systems is enabling continuous assessment of vehicle performance and early fault detection, enhancing overall fleet productivity and reliability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $28.8 Billion |

| Forecast Value | $112.8 Billion |

| CAGR | 14.5% |

The electric passenger cars segment accounted for 62% share in 2025 and is anticipated to grow at a CAGR of 14.1% between 2026 and 2035. This segment maintains a leading position due to the extensive deployment of passenger electric vehicles within organized fleet operations. The increasing need for battery performance assessments, software management, tire maintenance, and proactive servicing programs continues to drive demand for specialized maintenance solutions. Fleet managers are increasingly utilizing connected maintenance platforms to improve vehicle availability, lower operating expenditures, and extend battery service life. The growing emphasis on efficient fleet utilization and long-term asset management is expected to further support segment growth throughout the forecast period.

By service type, the preventive maintenance segment held a 40% share in 2025 and is forecast to grow at a CAGR of 13.2% from 2026 to 2035. The segment remains dominant as fleet operators focus on scheduled maintenance programs to minimize operational disruptions, enhance vehicle reliability, and prolong the lifespan of critical EV components. Routine evaluation of key vehicle systems remains essential for maintaining optimal performance and ensuring uninterrupted fleet operations. Meanwhile, predictive maintenance is experiencing notable growth as the adoption of AI-powered analytics, IoT-enabled sensors, and telematics platforms accelerates across electric vehicle fleets. These advanced technologies provide continuous visibility into vehicle conditions, enabling operators to identify potential issues before they escalate and reducing costly downtime.

China Electric Vehicle Fleet Maintenance Services Market held a 65% share and generated USD 4.6 billion in 2025. The country's strong position is supported by its extensive electric vehicle population, well-established EV manufacturing infrastructure, and ongoing electrification of transportation networks. The increasing deployment of electric vehicles has created significant demand for maintenance services, including battery management, predictive diagnostics, and connected fleet monitoring solutions. Continued expansion of transportation infrastructure and mobility networks, combined with rising transportation activity, is contributing to greater utilization of electric vehicle fleets and driving the need for advanced maintenance services throughout the country.

Major companies operating in the Global Electric Vehicle Fleet Maintenance Services Market include Amerit Fleet Solutions, Tesla, BYD, Proterra, Cox Automotive, Bosch, and Merchants Fleet. Companies operating in the Electric Vehicle Fleet Maintenance Services Market are focusing on technology-driven service expansion to strengthen their market position and enhance customer retention. Key strategies include the integration of AI-powered predictive maintenance platforms, advanced telematics solutions, and remote diagnostic capabilities that enable real-time fleet monitoring and proactive servicing. Market participants are also investing in digital fleet management platforms to improve operational visibility and maintenance efficiency. Strategic partnerships with fleet operators, vehicle manufacturers, and charging infrastructure providers are helping companies expand their service networks and improve customer reach. In addition, businesses are enhancing technician training programs, expanding maintenance coverage areas, and developing specialized battery management services.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Service type

- 2.2.4 Service provider

- 2.2.5 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for Predictive Maintenance

- 3.2.1.2 Expansion of Logistics & Last-Mile Delivery

- 3.2.1.3 Stringent Emission & Safety Regulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Maintenance Infrastructure Cost

- 3.2.2.2 Battery Degradation & Lifecycle Uncertainty

- 3.2.2.3 Lack of Standardized EV Service Ecosystem

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of EV Commercial Fleets

- 3.2.3.2 Integration of AI-Based Fleet Diagnostics

- 3.2.3.3 Expansion in Emerging Markets

- 3.2.3.4 Development of Battery-as-a-Service (BaaS) Models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.1.1 Telematics & GPS Tracking Systems

- 3.4.1.2 Onboard Diagnostics (OBD) Systems

- 3.4.1.3 Fleet Management Software Platforms

- 3.4.1.4 Real-Time Vehicle Health Monitoring

- 3.4.2 Emerging technologies

- 3.4.2.1 AI-Driven Predictive Maintenance

- 3.4.2.2 5G-Enabled Connected Fleet Systems

- 3.4.2.3 Battery Swapping & Smart Charging Integration

- 3.4.2.4 Autonomous Fleet Maintenance Systems

- 3.4.1 Current technological trends

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US: Federal EV Safety, Battery Handling, and Fleet Maintenance Regulations for Electric Vehicle Fleet Maintenance Services

- 3.6.1.2 Canada: Canadian Zero-Emission Vehicle and EV Fleet Maintenance Regulatory Framework

- 3.6.2 Europe

- 3.6.2.1 UK: UK Electric Vehicle Infrastructure and Fleet Maintenance Regulations

- 3.6.2.2 Germany: Germany Electric Mobility Act and EV Fleet Service Regulations

- 3.6.2.3 France: France Energy Transition and Electric Vehicle Fleet Maintenance Regulations

- 3.6.3 Asia Pacific

- 3.6.3.1 China: China New Energy Vehicle (NEV) Service and Maintenance Regulations

- 3.6.3.2 India: India Electric Mobility and EV Service Ecosystem Regulations for Fleet Maintenance

- 3.6.3.3 Japan: Japan Next-Generation Vehicle and EV Maintenance Regulations

- 3.6.4 Latin America

- 3.6.4.1 Brazil: Brazil National Electric Mobility and EV Fleet Maintenance Regulations

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi Arabia: Saudi Arabia Electric Mobility Standards and EV Fleet Maintenance Regulations

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Cost breakdown analysis

- 3.11 Impact of AI and Generative AI on the Market

- 3.11.1 AI Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.11.3 Risks Limitations and Regulatory Considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.13.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn)

- 5.1 Key trends

- 5.2 Electric Passenger Cars

- 5.3 Electric Vans

- 5.4 Electric Trucks

- 5.5 Electric Buses

- 5.6 Two & Three-Wheelers

Chapter 6 Market Estimates & Forecast, By Service Type, 2022 - 2035 (USD Mn)

- 6.1 Key trends

- 6.2 Preventive Maintenance

- 6.3 Corrective Maintenance

- 6.4 Predictive Maintenance

- 6.5 Software & Diagnostics Services

- 6.6 Battery System Services

Chapter 7 Market Estimates & Forecast, By Service Provider, 2022 - 2035 (USD Mn)

- 7.1 Key trends

- 7.2 OEM Authorized Service Centers

- 7.3 Independent Service Providers

- 7.4 In-House Fleet Maintenance

- 7.5 Mobile/On-Site Service Providers

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 (USD Mn)

- 8.1 Key trends

- 8.2 Logistics & Freight Companies

- 8.3 Public Transit Authorities

- 8.4 Corporate & Private Fleets

- 8.5 Rental & Leasing Companies

- 8.6 Municipal & Government Agencies

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Norway

- 9.3.8 Netherlands

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Amerit Fleet Solutions

- 10.1.2 Tesla

- 10.1.3 BYD

- 10.1.4 Bosch

- 10.1.5 Cox Automotive

- 10.1.6 Volvo

- 10.1.7 Mercedes-Benz

- 10.1.8 General Motors

- 10.1.9 Daimler Buses

- 10.2 Regional Players

- 10.2.1 Merchants Fleet

- 10.2.2 Holman

- 10.2.3 ARVAL

- 10.2.4 ALD Automotive

- 10.2.5 LeasePlan

- 10.2.6 Wheels

- 10.2.7 Element Fleet Management

- 10.3 Emerging Players / Disruptors

- 10.3.1 Rivian

- 10.3.2 Proterra

- 10.3.3 Arrival

- 10.3.4 Fleetio

- 10.3.5 Standard Fleet

- 10.3.6 ChargePoint

- 10.3.7 SparkCharge

- 10.3.8 Fuuse

- 10.3.9 Nuvve