PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071272

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071272

Network Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

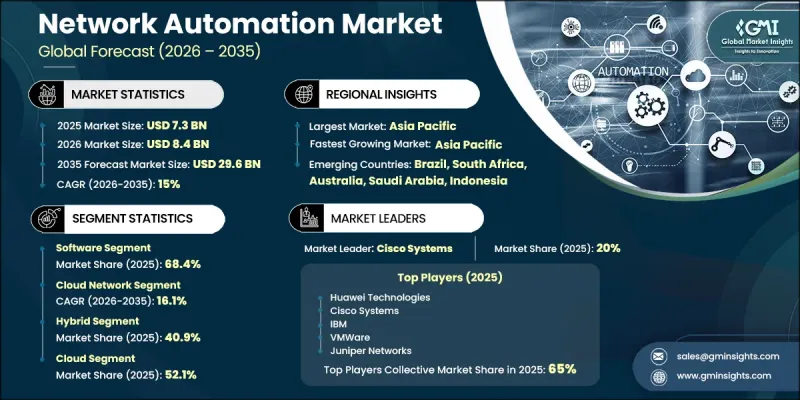

The Global Network Automation Market was valued at USD 7.3 billion in 2025 and is estimated to grow at a CAGR of 15% to reach USD 29.6 billion by 2035.

The market is witnessing rapid expansion as enterprises increasingly deploy AI, machine learning, and advanced analytics-enabled automation solutions to monitor and optimize network performance, security, and operational efficiency in real time. The rising demand for scalable, reliable, and self-healing network infrastructures, combined with the accelerating shift toward cloud computing and software-defined environments, is significantly boosting adoption across industries. The growth of the network automation market is further reinforced by evolving regulatory requirements and compliance standards that are compelling organizations to modernize legacy IT systems. Enterprises are placing greater emphasis on improving network reliability, reducing downtime, and strengthening cybersecurity resilience, which is accelerating the deployment of automated networking solutions across telecom, cloud, and enterprise ecosystems. As network environments become increasingly complex, automation plays a critical role in minimizing human intervention, preventing service disruptions, and ensuring consistent operational performance. Advanced technologies such as real-time telemetry, AI-driven analytics, and multi-layer automation frameworks are enabling continuous visibility into network traffic patterns, infrastructure health, and user activity. These capabilities are being integrated into intelligent network architectures that support proactive fault detection, automated remediation processes, dynamic workload balancing, and adaptive service delivery models. As a result, organizations are achieving improved operational efficiency while maintaining higher levels of network stability and performance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.3 Billion |

| Forecast Value | $29.6 Billion |

| CAGR | 15% |

The software segment accounted for a 68.4% share in 2025 and is projected to grow at a CAGR of 14.8% from 2026 to 2035. This segment forms the core of modern network automation ecosystems by enabling centralized orchestration, configuration management, and infrastructure control. Software platforms developed by key industry players such as Juniper Networks, VMware, and Cisco Systems are increasingly supporting intent-based networking models, where desired outcomes are defined and systems automatically configure network environments accordingly. The integration of AI-powered automation capabilities is further enhancing the efficiency, intelligence, and adaptability of network automation software solutions.

The cloud network segment held a 27.7% share in 2025 and is expected to grow at a CAGR of 16.1% from 2026 to 2035. Growth in this segment is driven by the widespread shift toward hybrid and multi-cloud infrastructures across enterprises. Organizations are increasingly deploying automation tools to manage workload distribution, enforce security policies, and maintain configuration consistency across distributed cloud environments. The rising adoption of containerized workloads, Kubernetes-based deployments, and API-centric architectures is further intensifying the need for automated orchestration in cloud-native networking environments.

China Network Automation Market held a 38.3% share and generated USD 556.8 million in 2025. The country's market expansion is supported by rapid advancements in cloud-native technologies, software-defined networking, and SD-WAN adoption across enterprises and telecom operators. Major domestic technology providers are heavily investing in AI-powered network automation solutions designed to support self-optimizing, self-healing, and intent-driven network management. These developments are particularly prominent in large-scale 5G networks and data center infrastructures, where efficiency, scalability, and real-time optimization are critical.

Key companies operating in the Global Network Automation Market include Cisco Systems, IBM, Juniper Networks, Hewlett Packard Enterprise (HPE), Huawei Technologies, VMware, Arista Networks, Fortinet, and Nokia. Companies in the network automation market are adopting a range of strategic initiatives to strengthen their competitive positioning and expand market presence. Continuous investment in artificial intelligence, machine learning, and predictive analytics is enabling the development of more intelligent and autonomous networking solutions. Vendors are increasingly focusing on intent-based networking platforms that simplify network management and enhance operational efficiency. Strategic partnerships with telecom operators, cloud providers, and enterprise customers are supporting large-scale deployment of automation solutions. Companies are also prioritizing cloud-native architecture development, API-driven integration capabilities, and multi-domain orchestration frameworks. Expansion into emerging digital economies, combined with strong focus on cybersecurity-enhanced automation tools, is further reinforcing market penetration.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Network Type

- 2.2.4 Network infrastructure

- 2.2.5 Deployment mode

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for network efficiency and cost optimization

- 3.2.1.2 Growth of cloud computing and virtualization

- 3.2.1.3 Expansion of 5G and edge computing

- 3.2.1.4 Increasing network complexity and scale

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment and integration complexity

- 3.2.2.2 Skill gaps and workforce readiness

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of AI-driven network automation (AIOps)

- 3.2.3.2 Growth in enterprise digital transformation initiatives

- 3.2.3.3 Expansion of intent-based networking (IBN)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 Federal Motor Vehicle Safety Standards

- 3.6.1.2 National Highway Traffic Safety Administration Driver Monitoring and Advanced Driver Assistance Guidelines

- 3.6.1.3 California Consumer Privacy Act

- 3.6.1.4 Illinois Biometric Information Privacy Act

- 3.6.2 Europe

- 3.6.2.1 EU General Safety Regulation

- 3.6.2.2 General Data Protection Regulation

- 3.6.2.3 UNECE cybersecurity and software update regulations (R155, R156)

- 3.6.2.4 National vehicle homologation requirements

- 3.6.3 Asia Pacific

- 3.6.3.1 Personal Information Protection Law

- 3.6.3.2 Cybersecurity Law

- 3.6.3.3 Data Security Law

- 3.6.3.4 Provisions on Automotive Data Security Management

- 3.6.3.5 Central Motor Vehicles Rules

- 3.6.4 Latin America

- 3.6.4.1 General Data Protection Law

- 3.6.4.2 National Traffic Council Resolutions

- 3.6.4.3 National Department of Traffic Regulations

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi Personal Data Protection Law

- 3.6.5.2 Saudi Standards, Metrology and Quality Organization Regulations

- 3.6.5.3 Gulf Standardization Organization Standards

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Cost breakdown analysis

- 3.11 Impact of AI and Generative AI on the Market

- 3.11.1 AI Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.11.3 Risks Limitations and Regulatory Considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.13.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 (USD Mn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Intent-based networking

- 5.2.2 SD-WAN

- 5.2.3 Network automation & orchestration

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Network Type, 2022 - 2035 (USD Mn)

- 6.1 Key trends

- 6.2 LAN

- 6.3 WAN

- 6.4 Data center networks

- 6.5 Cloud networks

Chapter 7 Market Estimates & Forecast, By Network Infrastructure, 2022 - 2035 (USD Mn)

- 7.1 Key trends

- 7.2 Physical

- 7.3 Virtual

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Deployment, 2022 - 2035 (USD Mn)

- 8.1 Key trends

- 8.2 On premises

- 8.3 Cloud

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn)

- 9.1 Key trends

- 9.2 IT & Telecom

- 9.3 BFSI

- 9.4 Healthcare

- 9.5 Manufacturing

- 9.6 Energy & Utilities

- 9.7 Retail

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Norway

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Cisco Systems

- 11.1.2 Juniper Networks

- 11.1.3 Huawei Technologies

- 11.1.4 Hewlett Packard Enterprise (HPE)

- 11.1.5 IBM

- 11.1.6 VMware

- 11.1.7 Nokia Corporation

- 11.1.8 Ericsson

- 11.1.9 Arista Networks

- 11.1.10 F5 Networks

- 11.2 Regional Players

- 11.2.1 NEC Corporation

- 11.2.2 Tata Consultancy Services (TCS)

- 11.2.3 Infosys

- 11.2.4 Wipro

- 11.2.5 HCL Technologies

- 11.2.6 Micro Focus

- 11.3 Emerging Players / Disruptors

- 11.3.1 NetBrain Technologies

- 11.3.2 Apstra

- 11.3.3 BlueCat Networks

- 11.3.4 SolarWinds

- 11.3.5 Red Hat

- 11.3.6 Forward Networks

- 11.3.7 Itential

- 11.3.8 Alkira