PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071279

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071279

Geographic Information System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

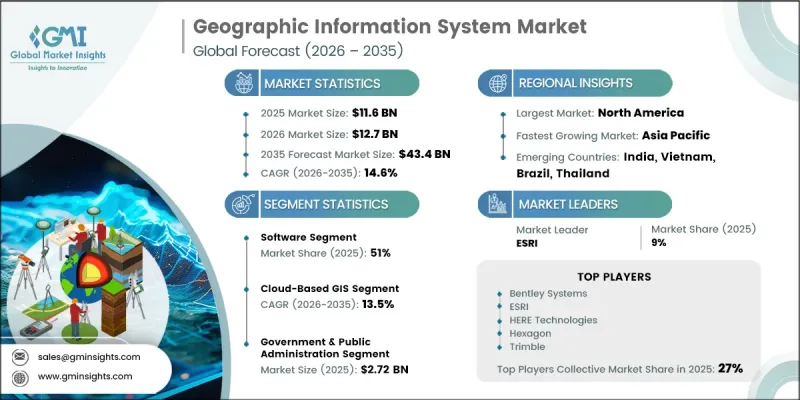

The Global Geographic Information System (GIS) Market was valued at USD 11.6 billion in 2025 and is estimated to grow at a CAGR of 14.6% to reach USD 43.4 billion by 2035.

Market growth is driven by a structural shift in how spatial technologies are deployed and consumed across industries. Geographic information system is increasingly evolving from standalone mapping tools into integrated spatial intelligence systems embedded within enterprise operations. These systems now support advanced use cases such as real-time analytics, infrastructure monitoring, risk assessment, and digital environment modeling across multiple sectors. The convergence of cloud-native GIS platforms, artificial intelligence-enabled geospatial processing, and expanding satellite and drone-based data sources is significantly enhancing analytical capabilities while reducing deployment time across industries. Organizations are increasingly integrating geographic information system with connected sensor networks and virtual infrastructure models to enable continuous monitoring and simulation of physical environments. Growing demand for scalable spatial intelligence solutions is further reinforced by the expansion of digital transformation initiatives across both public and private sectors. In addition, rising investments in smart infrastructure, urban planning modernization, and data-driven governance are creating sustained opportunities for GIS adoption. As enterprises prioritize location intelligence as a core component of decision-making, geographic information system technologies are becoming increasingly central to operational efficiency, strategic planning, and predictive analytics across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.6 Billion |

| Forecast Value | $43.4 Billion |

| CAGR | 14.6% |

The software segment accounted for 51% share in 2025 and is expected to grow at a CAGR of 13.3% through 2035. This segment includes integrated spatial platforms as well as specialized analytical tools designed for industry-specific applications. Software solutions remain the foundation of GIS adoption, enabling organizations to process, analyze, and visualize geospatial data efficiently. Demand continues to rise as enterprises increasingly rely on spatial analytics for operational planning, resource management, and decision support across multiple industries.

The cloud-based GIS solutions segment held a 48% share in 2025 and is projected to grow at a CAGR of 13.5% during 2026-2035. Growth in this segment is driven by increasing demand for scalable, flexible, and remotely accessible geospatial platforms. Cloud deployment allows organizations to manage large volumes of spatial data while supporting collaboration, real-time analysis, and integrated digital workflows. The integration of advanced technologies such as connected sensors, distributed computing, and advanced visualization tools is further strengthening adoption across industries including infrastructure management, transportation systems, utilities, and urban development.

United States Geographic Information System (GIS) Market generated USD 4 billion in 2025. Market expansion in the country is supported by strong institutional demand for geospatial solutions, increasing use of location-based analytics, and rising adoption of advanced digital infrastructure systems. Federal programs supporting standardized geospatial data management and interoperability continue to sustain consistent demand across government agencies. Additionally, growing reliance on GIS for environmental monitoring, emergency response planning, and infrastructure management is reinforcing long-term market stability and expansion across public and private sectors.

Key companies operating in the global geographic information system market include ESRI, Hexagon, HERE, Trimble, Microsoft, Bentley Systems, Mapbox, Autodesk, GE Vernova, and SuperMap. Companies operating in the geographic information system (GIS) market are adopting multiple strategic initiatives to strengthen their market presence and enhance competitive positioning. Continuous investment in research and development is enabling vendors to advance spatial analytics capabilities, improve platform scalability, and integrate artificial intelligence into geospatial workflows. Cloud migration strategies are being prioritized to enhance accessibility, reduce infrastructure dependency, and support real-time data processing. Firms are also focusing on expanding ecosystem partnerships with technology providers, infrastructure companies, and data suppliers to broaden solution offerings. In addition, product diversification across industry-specific applications is helping companies address evolving enterprise requirements. Geographic expansion into emerging markets, along with subscription-based pricing models and software-as-a-service delivery frameworks, is further supporting long-term customer acquisition and revenue stability across the global GIS industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Component

- 2.2.2 Deployment Model

- 2.2.3 Industry Sector

- 2.2.4 Organization Size

- 2.2.5 Region

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Technology & platform providers

- 3.1.1.2 Sensor & IIoT hardware vendors

- 3.1.1.3 System integrators & implementation partners

- 3.1.1.4 End-use industries & asset operators

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of location-based intelligence across industries

- 3.2.1.2 Rising smart city & urban infrastructure development

- 3.2.1.3 Growing demand for geospatial data in disaster & environmental management

- 3.2.1.4 Expansion of cloud-based gis & remote sensing technologies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of geospatial data acquisition & system integration

- 3.2.2.2 Data privacy, security & regulatory compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Shift toward AI-powered spatial analytics

- 3.2.3.2 Rising integration of GIS with IoT & digital twin platforms

- 3.2.3.3 Increasing adoption of mobile & web-based GIS solutions

- 3.2.3.4 Growing use of 3D mapping & indoor GIS technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 U.S. Geospatial Data Act (GDA)

- 3.5.1.2 Federal Geographic Data Committee (FGDC) Standards

- 3.5.1.3 Canadian Geospatial Data Infrastructure (CGDI) Policies

- 3.5.2 Europe

- 3.5.2.1 GDPR (General Data Protection Regulation)

- 3.5.2.2 INSPIRE Directive (Infrastructure for Spatial Information in Europe)

- 3.5.2.3 EU Data Governance Act

- 3.5.2.4 Copernicus Earth Observation Programme Regulations

- 3.5.3 Asia-Pacific

- 3.5.3.1 China Surveying and Mapping Law

- 3.5.3.2 Japan Data Security Law (DSL)

- 3.5.3.3 India National Geospatial Policy 2022

- 3.5.3.4 Singapore Geospatial Master Plan and Cybersecurity Act

- 3.5.4 Latin America

- 3.5.4.1 Brazil General Data Protection Law (LGPD)

- 3.5.4.2 Mexico National Geographic and Statistical Information System Regulations

- 3.5.5 MEA

- 3.5.5.1 Saudi National Geospatial Information Center (NGIC) Policies

- 3.5.5.2 UAE National Spatial Data Infrastructure (NSDI) Initiatives

- 3.5.1 North America

- 3.6 Technology and Innovation Landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Use cases

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 Automated design optimization

- 3.11.3 Supply chain AI for demand forecasting

- 3.11.4 GenAI use cases & adoption roadmap by segment

- 3.11.5 Risks, Limitations & Regulatory Considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case - key macro & industry variables driving CAGR

- 3.12.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Desktop GIS

- 5.2.2 Cloud GIS / Web GIS

- 5.2.3 Mobile GIS

- 5.2.4 Open-Source GIS Platforms

- 5.3 Services

- 5.3.1 Professional Services (implementation, consulting, training)

- 5.3.2 Managed Services

- 5.4 Data & Content

- 5.4.1 Geospatial Data and Basemaps

- 5.4.2 Imagery and Remote Sensing Data

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Cloud-Based GIS

- 6.3 On-Premises GIS

- 6.4 Hybrid Deployment

Chapter 7 Market Estimates & Forecast, By Industry Sector, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Government & Public Administration

- 7.3 Utilities

- 7.4 Insurance & Financial Services

- 7.5 Agriculture & Forestry

- 7.6 Transportation & Mobility

- 7.7 Logistics & Supply Chain

- 7.8 Construction & Real Estate

- 7.9 Environment & Natural Resources

- 7.10 Others

Chapter 8 Market Estimates & Forecast, By Organization Size, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Large Enterprise (500+ employees)

- 8.3 Small and Medium Enterprise (SME)

- 8.4 Government and Public Sector

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 North America

- 9.1.1 US

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Belgium

- 9.2.7 Netherlands

- 9.2.8 Sweden

- 9.2.9 Russia

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 Singapore

- 9.3.6 South Korea

- 9.3.7 Vietnam

- 9.3.8 Indonesia

- 9.3.9 Thailand

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

- 9.5.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 ESRI

- 10.1.2 Hexagon

- 10.1.3 HERE

- 10.1.4 Microsoft

- 10.1.5 Trimble

- 10.1.6 Bentley Systems

- 10.1.7 Mapbox

- 10.1.8 Autodesk

- 10.1.9 GE Vernova

- 10.1.10 Planet Labs

- 10.2 Regional players

- 10.2.1 Topcon Positioning Systems

- 10.2.2 SuperMap GIS

- 10.2.3 Caliper

- 10.2.4 Blue Marble Geographics

- 10.2.5 Safe Software

- 10.2.6 VertiGIS

- 10.3 Emerging players

- 10.3.1 Pix4D

- 10.3.2 Orbital Insight

- 10.3.3 Vantor

- 10.3.4 GIS Cloud