PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071324

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071324

United Kingdom Doors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

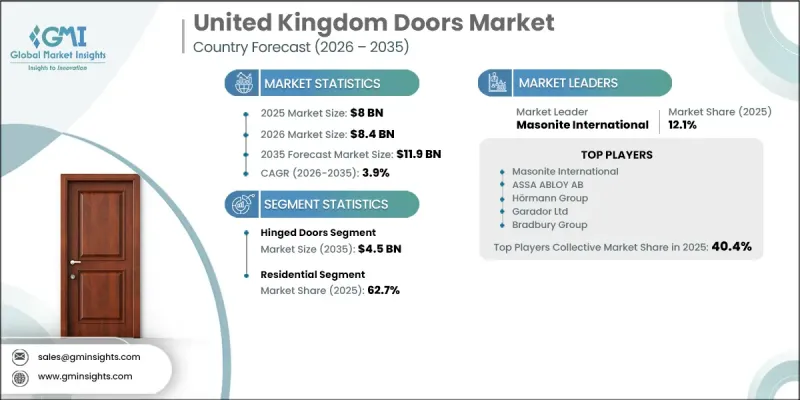

United Kingdom Doors Market was valued at USD 8 billion in 2025 and is estimated to grow at a CAGR of 3.9% to reach USD 11.9 billion by 2035.

Market growth is supported by sustained housing development activity driven by government-backed housing initiatives that improve access to financing for first-time buyers. These programs are encouraging higher volumes of new residential construction, which in turn is generating consistent demand for door installations across new-build properties. Developers benefit from policy support that maintains a steady construction pipeline, providing long-term visibility for manufacturers, fabricators, and installation contractors operating in the United Kingdom construction ecosystem. In addition, refurbishment and retrofit activity is becoming an increasingly important growth driver as existing housing stock undergoes upgrades to meet evolving energy efficiency, insulation, and safety standards. Homeowners are also investing in property improvements aimed at enhancing both aesthetics and market value, which supports ongoing replacement demand even during periods of economic uncertainty. This combination of new-build expansion and steady renovation activity ensures structural stability for the doors market across residential and commercial applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8 Billion |

| Forecast Value | $11.9 Billion |

| CAGR | 3.9% |

The hinged doors segment generated USD 3 billion in 2025 and is expected to reach USD 4.5 billion by 2035. This segment continues to lead the market due to its cost efficiency, mechanical simplicity, and widespread suitability for high-volume residential construction. Hinged doors remain the preferred choice for budget-conscious homeowners and large-scale developers because they require fewer components and are easier to install compared to alternative door systems such as sliding or folding designs. Their practicality and affordability make them a standard solution across both new construction and renovation projects, ensuring consistent demand across the United Kingdom market.

The residential segment accounted for 62.7% share in 2025, making it the dominant end-use category. This leadership is supported by strong housing development activity as well as a well-established replacement and refurbishment cycle across the country's housing stock. Residential properties typically require multiple door installations, including both internal and external applications, which significantly increases total unit demand compared to commercial buildings. Ongoing home improvement activity, combined with evolving consumer preferences for modern and customized door designs, continues to strengthen residential market dominance.

Major companies operating in the United Kingdom doors industry include ASSA ABLOY AB, JELD-WEN Holding Inc, Masonite International, Hormann Group, Endurance Doors, Garador Ltd, Deanta, LPD Doors, Urban Front, George Barnsdale & Sons, Booth Industries, Bradbury Group, CDC Garage Doors, Apeer Doors, Gowercroft Joinery, Hallmark Panels, Metador Ltd, Pendle Doors, Stronghold Security Doors, Todd Doors, and Vicaima SA. Companies in the United Kingdom doors market are focusing on strategic initiatives aimed at strengthening their competitive position and expanding market reach. Product innovation is a key strategy, with manufacturers developing energy-efficient, fire-rated, and security-enhanced door solutions to meet evolving building regulations and consumer expectations. Expansion of product portfolios across premium, mid-range, and budget categories is enabling companies to serve a wider customer base. Investments in advanced manufacturing technologies and automation are improving production efficiency and cost competitiveness. Firms are also strengthening distribution networks through partnerships with builders, contractors, and retail channels to ensure wider market penetration. Sustainability initiatives, including the use of responsibly sourced materials and eco-friendly production processes, are becoming increasingly important in brand positioning.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.2.1 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Material

- 2.2.3 Application

- 2.2.4 End Use

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising construction and real estate development

- 3.2.1.2 Increasing home renovation and remodeling

- 3.2.1.3 Focus on energy efficiency

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Raw material costs and price volatility

- 3.2.2.2 Supply chain disruptions

- 3.2.3 Opportunities

- 3.2.3.1 Retrofit & renovation market expansion

- 3.2.3.2 Smart & connected door systems growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.4.1 Building regulations (Part Q Security, Part L Energy Efficiency, Part B Fire Safety)

- 3.4.2 British standards (BS 476, BS EN 1634, BS 6375)

- 3.4.3 CE marking & UKCA requirements

- 3.4.4 Fire door certification & third-party accreditation schemes

- 3.4.5 Energy performance standards & thermal efficiency requirements

- 3.4.6 Planning & conservation area restrictions

- 3.5 Major market trends and disruptions

- 3.6 Technology/innovation landscape

- 3.6.1 Current trends in swimwear

- 3.6.2 Emerging trends

- 3.7 Pricing Analysis (driven by primary research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.8 Future market trends

- 3.9 Trade data analysis (driven by paid database) (HS Code-76101000)

- 3.9.1 Import/export volume & value trends (driven by primary research)

- 3.9.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 Gen-AI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Capacity & production landscape (driven by primary research)

- 3.13.1 Installed manufacturing capacity by region & key producer (driven by primary research)

- 3.13.2 Capacity utilization rates & expansion pipelines (driven by primary research)

- 3.14 Consumer behaviour analysis

- 3.14.1 Purchasing patterns

- 3.14.2 Preference analysis

- 3.14.3 Regional variations in consumer behaviour

- 3.14.4 Impact of e-commerce on buying decision

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product, 2022-2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Hinged Doors

- 5.3 Sliding Doors

- 5.4 Bi-Fold Doors

- 5.5 French Doors

- 5.6 Overhead/Sectional Doors

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Material, 2022-2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Wooden doors

- 6.2.1 Solid wood doors

- 6.2.2 Engineered wood doors

- 6.3 Metal doors

- 6.3.1 Steel doors

- 6.3.2 Aluminum doors

- 6.4 uPVC (unplasticized polyvinyl chloride) doors

- 6.5 Composite doors

- 6.6 Glass doors

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Interior Doors

- 7.3 Exterior Doors

Chapter 8 Market Estimates & Forecast, By End Use, 2022-2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Residential

- 8.2.1 New residential

- 8.2.2 Improvement & repair

- 8.3 Commercial

- 8.3.1 New commercial

- 8.3.2 Improvement & repair

Chapter 9 Company Profiles

- 9.1 Global Company

- 9.1.1 ASSA ABLOY AB

- 9.1.2 Bradbury Group

- 9.1.3 Garador Ltd

- 9.1.4 Hallmark Panels

- 9.1.5 Hormann Group

- 9.1.6 JELD-WEN Holding Inc

- 9.1.7 Masonite International

- 9.2 Regional Company

- 9.2.1 Apeer Doors

- 9.2.2 Deanta

- 9.2.3 Endurance Doors

- 9.2.4 George Barnsdale & Sons

- 9.2.5 Gowercroft Joinery

- 9.2.6 LPD Doors

- 9.2.7 Vicaima SA

- 9.3 Emerging Company

- 9.3.1 Booth Industries

- 9.3.2 CDC Garage Doors

- 9.3.3 Metador Ltd

- 9.3.4 Pendle Doors

- 9.3.5 Stronghold Security Doors

- 9.3.6 Todd Doors

- 9.3.7 Urban Front